Credit put spreads are one of the most versatile tools in an options trader’s playbook, offering the ability to generate income with defined risk and efficient use of capital. At their core, these spreads profit from time decay and the market’s tendency to drift upward or sideways more often than it crashes downward. But the real power of the strategy emerges when combined with a disciplined rolling process—systematically extending duration, re-centering strikes, and collecting additional credit over time. Rolling transforms a simple spread into a dynamic, repeatable system that can adapt to changing markets, reduce the probability of total loss, and steadily build premium income. This article explores not only the mechanics of credit put spreads, but also the art and discipline of rolling them, highlighting why this approach can be a cornerstone of a trader’s income strategy.

My favorite go-to option trading strategy is rolling credit put spreads. It encompasses several basic but important philosophies I use in much of my trading. Take this concept and build on it in many ways once you understand the details and choices involved. I’ve written other articles about put spreads, but I thought it would be good to write a fresh article about how I trade them, along with the mechanics I use for continuously rolling put spreads. For additional information, you can read earlier write ups on credit put spreads, optimal delta for put spreads, 7 DTE put spreads, Hold, Fold, or Roll, and Desperate Options Call for Desperate Measures.

We’ll take it in chunks, explaining what a credit put spread is, digging in the details of the setup, understanding the mechanics of a rolling put spread trade, and talk about risk and returns.

📌 What is a Credit Put Spread?

A credit put spread (also called a bull put spread) is an options strategy where a trader:

- Sells a put option at a higher strike price (closer to the current stock price).

- Buys a put option at a lower strike price (further out-of-the-money).

Both options share the same expiration date. The result is a net credit received upfront, which represents the maximum profit potential.

When a trader sells an option, they collect a credit. When a trader buys an option, they pay a debit. Because the put option being sold is closer to the current strike price, it is more expensive than the put option being bought further out-of-the-money is to buy, we collect a bigger credit than the debit, so we end up with a net credit.

The reason that this setup is often called a bull put spread is because it is considered a bullish trade. It does better when the market goes up and worse when the market goes down. Bullish traders look to make money from the market going up, while bearish traders try to make money from the market going down.

For this type of trade, I generally use specific Delta values for the put options I choose. Among other things, Delta represents the probability of an option expiring in the money. We want a high probability that the option will not end up in the money, and that instead it will quickly decay in value as time passes.

Basic setup with Delta 20/13

- Sell Put (Δ ≈ 0.20): This strike has about a 20% probability of finishing in-the-money.

- Buy Put (Δ ≈ 0.13): This strike is further out-of-the-money, with about a 13% probability of finishing in-the-money.

This creates a defined-risk bullish position: you’re betting the stock will stay above the short strike (the 20-delta put).

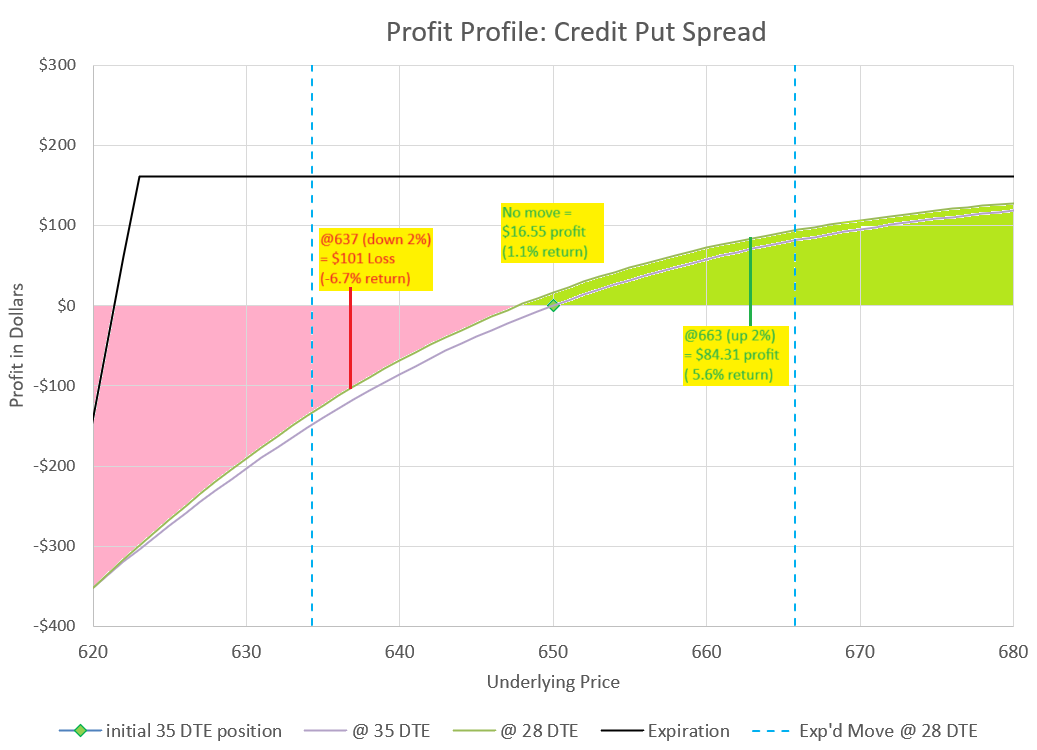

Here’s the set-up I like to shoot for to start with and as I adjust my positions over time. Consider trading options on the SPY ETF trading at $650 per share. In this example, we sell a 15 point wide spread and collect a premium of $1.61. We choose our strikes based on their Delta values of 20 and 13.

🎯 Goal of the Trade

The primary objective is to collect premium while taking on a high-probability, limited-risk position.

- If the stock stays above the short strike at expiration, both puts expire worthless, and the trader keeps the credit.

- If the stock falls, the long put limits losses, ensuring risk is capped.

This image illustrates the profit profile at different prices at different points in time. The light pink and green areas represent the profit and loss after one week in the trade, the dark red and green areas represent the profit and loss at expiration. Notice that the values just a little less than the starting price are a loss after a week, but if held to expiration become a profit. The dashed blue lines represent the expected move for one week in this trade, a range that we statistically expect the price to end up within. The line at the top of the green profit zone represents the profit that would be made if the options both expired with a value of zero. The line at the bottom of the red loss zone represents the maximum loss if both options were to expire in the money, making the difference in their premiums be $15, the width of the spread.

However, we are going to roll, or adjust, our position before expiration, so our goal is a little more subtle, we want the net premium to decay towards zero, since it will only be zero at expiration. Since we plan to roll after one week, the light pink and light green profit curves are what we expect to see after one week. We’ll get to an explanation of rolling, but first let’s continue to understand the set up, starting with why to choose a spread instead of a single naked put.

⚖️ Why Sell a Spread Instead of a Naked Put?

1. Defined Risk

- Naked Put: The risk is substantial—if the stock collapses, losses can be very large (down to zero price of the underlying asset).

- Credit Put Spread: The long put acts as insurance, capping the maximum loss to the width of the strikes minus the credit received.

- Simple example: Sell 100 put, buy 95 put, collect $1.00 credit → Max loss = $4.00 per share ($5 spread – $1 credit).

2. Capital Efficiency

- Naked Put: Brokers often require large margin reserves, since the downside risk is theoretically very high.

- Credit Put Spread: Margin requirement is only the strike width minus credit. This frees up capital for other trades.

3. Higher Return on Capital

- Because the margin requirement is smaller, the percentage return on capital can be significantly higher with spreads.

- Example:

- Naked Put: $1.00 premium collected, $2,000 margin → 5% return.

- Credit Spread: $1.00 premium collected, $400 margin → 25% return.

- Example:

4. Psychological Advantage

- Defined risk makes it easier to stick to a trading plan.

- Traders can size positions more confidently without fear of catastrophic loss.

🧮 Mechanics in Practice

Trade Setup Considerations

1. Choosing the Underlying: Index ETFs vs. Individual Stocks

- Index ETFs (e.g., SPY, QQQ, IWM) or Index Options (e.g., SPX, RUT):

- Tend to move more smoothly because they represent a basket of stocks, reducing the risk of sudden, outsized moves caused by single-company news (earnings, lawsuits, downgrades).

- Lower gap risk compared to individual equities.

- More liquid option chains, often with tighter bid/ask spreads—important for efficient fills and rolling.

- Individual Stocks:

- Higher volatility and idiosyncratic risk.

- A single event can blow through strikes, making spreads harder to manage.

- Conclusion: For systematic put spread trading, index-based underlyings are generally safer and more consistent for credit spread trades.

2. Why Delta 20/13 Strikes?

- Delta ≈ 20 (short put):

- Represents about an 80% probability of expiring out-of-the-money.

- Provides a balance between premium received and probability of profit.

- Delta ≈ 13 (long put):

- Positioned further out-of-the-money, providing defined risk protection.

- Theta Optimization:

- The 20/13 pairing maximizes Theta (time decay) as a percentage of the spread width.

- This means the spread decays in your favor at an efficient rate relative to the capital at risk.

- In practice: you’re collecting premium where decay is strongest, while still keeping risk capped.

- For in depth details on this, see the article on best Deltas for put spreads.

3. Duration: 4–6 Weeks to Expiration

- Why 4–6 Weeks?

- This window captures the “sweet spot” of time decay—Theta accelerates as expiration approaches, but you’re not so close that daily monitoring becomes mandatory.

- Provides flexibility to manage or roll without being forced into reactive decisions.

- Management Approach:

- After about 7 days, evaluate and roll the position back out in time:

- If profitable, take early gains (up to 50–70% of max profit) and re-position.

- If challenged, roll down/out to re-center the trade.

- This cadence allows for weekly check-ins rather than daily micromanagement.

- After about 7 days, evaluate and roll the position back out in time:

📝 Summary of Setup

- Underlying: Favor index ETFs/options for smoother, lower-risk exposure.

- Strikes: Sell ~20 delta, buy ~13 delta → optimal Theta capture with defined risk.

- Duration: 4–6 weeks → balance between time decay and manageable oversight.

- Management: Weekly rolls keep the system mechanical and stress-free.

🔄 Managing the Trade: Rolling Credit Put Spreads

1. What Does “Rolling” Mean?

- Definition: Rolling a spread means closing the existing position and simultaneously opening a new one in a single order ticket.

- Mechanics:

- The broker executes both legs together, so you’re never left exposed.

- Example: Close current short 100/95 put spread, open new 100/95 put spread one week later in expiration. You place an order with four legs to do this.

- Goal: Adjust the trade’s duration, strikes, or both—while collecting additional credit.

2. Why Roll Weekly?

- Time Decay Harvesting: By moving the spread out in time, you reset the clock and continue collecting Theta.

- Consistency: Weekly rolls keep the position aligned with your original setup (20/13 deltas, 4–6 weeks out).

- Credit Accumulation: Each roll should add net premium, steadily increasing total collected credit over the life of the trade.

- Avoid Drama of Expiration: By keeping the position weeks away from expiration and only staying in the trade for 1/4 or 1/5 of the duration, you avoid worrying about whether the position will expire at max profit or max loss based on a sudden move in the last few days of the trade. Instead, you have plenty of time to calmly decide how to roll each week unemotionally.

3. Rules for Rolling

- Always Roll for a Credit:

- Never pay to roll. The roll must bring in additional premium, even if small.

- When the Market Moves Up:

- Roll strikes up to re-center at your target deltas (20/13).

- This keeps the spread positioned optimally for Theta decay.

- When the Market Moves Down:

- Roll strikes down only as far as possible while still collecting a credit.

- This preserves defined risk while keeping the trade profitable over multiple rolls.

4. Example Workflow

- Initial Setup: Sell 623 put (Δ ≈ 20), buy 608 put (Δ ≈ 13), 5 weeks to expiration.

- One Week Later:

- If price is stable or higher → roll out one week, re-center strikes at new 20/13 deltas, collect credit.

- If price is lower → roll out one week, move strikes down as much as possible at same width while still netting a credit. Consider each roll down as part of a fight to extend trade time to give the market time to rebound and return to its long-term tendency to rise.

- Repeat Weekly: Each roll extends duration, maintains target deltas, and adds cumulative credit.

5. Benefits of Rolling

- Credit Stacking: Each roll builds additional premium, improving breakeven and return on capital.

- Risk Control: Defined risk remains constant (spread width), even as credits accumulate.

- Mechanical Discipline: Rolling weekly creates a repeatable, rules-based system—removing guesswork and emotion.

✅ Key Takeaways from Rolling

Rolling is not about “fixing” a losing trade—it’s about systematically extending time, optimizing deltas, and stacking credits. By always rolling for a credit, you ensure the position works in your favor over time, while maintaining defined risk and capital efficiency.

📊 The Role of Delta in Credit Put Spreads

Delta is one of the most important “Greeks” in options trading, and understanding it is essential for both entering and managing credit put spreads. While many traders think of Delta only as a directional measure, it actually provides multiple layers of insight when applied to spreads.

1. Delta as Sensitivity to Price Changes

- Definition: Delta measures how much an option’s premium will change for a $1 move in the underlying security.

- Application to Spreads: By looking at the net Delta of a spread, traders can estimate how much the spread’s value will change as the underlying moves.

- This helps anticipate how quickly profits or losses may accumulate.

- In our example of a 15 point wide spread with a net Delta of 7, a $1 increase in the $650 priced underlying would provide a $7 increase to the $1500 capital at risk. If you do the math, you’ll see that on a percentage basis, that’s almost 3x as much movement for the option position.

2. Delta as Probability of Expiring In-the-Money

- Rule of Thumb: Delta approximates the probability that a strike will finish in-the-money at expiration.

- Example: A 20-delta short put has about a 20% chance of being in-the-money at expiration.

- Nuance with Rolling: Since we don’t hold to expiration in a rolling strategy, this probability is more of a guideline than a certainty. Rolling reduces the chance of a total loss, but it never eliminates it.

3. Delta as Probability of Touching

- Touch Probability: A simple but powerful rule is that the probability of the underlying touching a strike before expiration is roughly 2 × Delta.

- Example: A 20-delta put has about a 40% chance of being touched before expiration.

- Why It Matters: Touches occur more frequently than final in-the-money outcomes, so traders must be prepared for strikes to be tested even if they ultimately expire worthless.

- Rolling Impact: Since we are rolling out after only a fraction of the time to expiration, we greatly reduce the probability of touching as well.

4. Delta as Share Equivalent

- Interpretation: Delta also represents the equivalent number of shares an option controls.

- Example: Selling a single 0.20 delta put is roughly equivalent to being long 20 shares of stock. Buying a single 0.13 delta put is roughly equivalent to being short 13 shares of stock.

- With Spreads: This is less obvious because the long and short legs offset each other, but it still provides perspective on the directional exposure of the position.

- In our example, with a net Delta of 7, our 15 point wide spread will have the price movement of the equivalent of 7 shares of the underlying ETF.

5. A Unique Observation: Premium Value Between Delta Values

- A credit spread’s premium as a percentage of its width will generally fall between the two Delta values of the strikes.

- Example:

- 10-point wide spread with short put Δ = 20 and long put Δ = 13.

- Premium will typically be between 13% and 20% of the width → $1.30 to $2.00.

- Why It Matters: This is a unique attribute of spreads and worth internalizing. It provides a quick way to sanity-check pricing and understand where the spread should trade. It also helps to understand how choices for rolling vary at different Delta values.

6. Delta and Rolling

- When Rolling for Credit: To collect additional premium, you often need to roll to longer-dated strikes with a higher average Delta.

- When Rolling Down: To avoid paying a debit, you must roll to new strikes with similar Delta as the old setup.

- Time Factor: Longer-dated options allow you to find lower strikes with the same Delta as shorter-dated options, since more time means more uncertainty.

✅ Key Takeaways for Delta

Delta is not just a directional measure—it’s a multi-purpose tool for spread traders. It helps estimate price sensitivity, probability of outcomes, likelihood of touches, and even provides a framework for understanding spread pricing. Ultimately, spread traders profit when Delta values decrease—whether from favorable price movement or from time decay reducing the probability of ending in-the-money.

🚨 When Things Go Wrong: Survival Mode Management

1. The Reality of a Big Move Down

- While the mechanical rolling process keeps most trades profitable and strikes out-of-the-money, markets can and do make sharp downside moves.

- In these cases, the short strike can move in-the-money, and the spread’s Theta flips negative:

- Instead of time decay working for you, it now works against you.

- Each passing day erodes your position’s value, making recovery harder.

- At this point, the strategy shifts from income generation to damage control.

- While we earlier said to always collect a credit to roll, sometimes that just isn’t possible- when strikes are in the money.

2. Why Rolling for Credit Stops Working

- Once the short strike is in-the-money, the premium structure changes:

- Rolling out in time no longer produces a net credit.

- Instead, you face debit rolls—paying to extend the trade.

- Time is working toward both options expiring in the money instead of expiring worthless.

- This is the signal that you’ve entered survival mode.

3. The “Least Bad” Choices

When in survival mode, there are no good options—only less bad ones. A disciplined trader must choose based on risk tolerance and market outlook:

- Roll for Debit at Same Strikes (Buy Time)

- Extend the trade to a later expiration, keeping strikes unchanged.

- This buys time for the market to recover, but costs a debit.

- Risk: You’re paying to wait, with no guarantee of improvement. The payment costs additional capital, which is more potential loss.

- Roll Down Strikes (Pay Larger Debit to Get OTM)

- Move strikes further down to re-establish out-of-the-money positioning.

- This reduces future risk but often requires a current large debit payment.

- Risk: Locks in a significant loss upfront. The payment is adding significant capital to a losing position.

- Close the Trade (Cut Losses)

- Exit the position entirely, realizing the loss.

- This avoids further uncertainty and prevents a total loss if the market continues lower.

- Risk: Loss is crystallized, but remaining spread capital is freed for new opportunities.

4. The Trader’s Decision

- There is no universally correct answer in survival mode.

- The choice depends on:

- Market conditions (is the move a short-term panic or a structural shift?).

- Trader’s capital reserves and willingness to pay debits.

- Psychological comfort with uncertainty.

- The key is to accept that survival mode is about minimizing damage, not maximizing profit.

5. Adopting a Contrarian Viewpoint

When volatility is high and markets are low, this is the best time historically to sell puts, as volatility tends to collapse and prices tend to quickly rise off the bottom. So, finding a way to stay in the market when everyone else is getting out most often leads to big gains in a short amount of time. Staying in forces a trader to add capital when there is historically the best future returns.

- Think of a drawdown where you must pay a debit as part of the buy low/sell high cycle.

- All the credits that are banked from the many rolls during good times are selling high.

- All the debits paid in tough times are buying low.

- Closing a position in this situation prevents a trader from benefitting from the large recovery gains after the market bottoms out.

✅ Takeaway for Survival in Down Markets

- Most of the time, the 20/13 delta credit put spread with weekly rolls is a high-probability, income-generating strategy.

- But when a large or extended downside move pushes strikes in-the-money, the system shifts into survival mode.

- At that point, the trader must choose the least bad option: roll for debit, roll down for a larger debit, or close the trade.

- Success comes from recognizing this shift quickly and acting decisively, rather than hoping Theta will turn back in your favor.

- A trader may even decide to consider down markets as an opportunity to be a contrarian thinker.

- In the end, the measure of success for a trader that rolls continuously like this over the long haul is whether the total credit collected over time exceeds the total debits paid.

⚠️ Understanding the Risks of Rolling Credit Put Spreads

1. The Illusion of Safety

- Credit put spreads can appear deceptively safe because of their defined risk and low capital requirements.

- While this structure allows for higher returns on capital, it also carries the real possibility of a total loss if the underlying makes a large move against the position.

- Defined risk doesn’t mean “no risk.” It just means that you know the total amount you can lose and not exceed. And in a defined risk trade, you can lose 100% of the capital at risk- it is a very real possibility.

- Starting at these Delta values, this is a high probability trade, and is expected to profit and also collect a credit when rolling most weeks. It can be easy to get complacent that there isn’t much risk with lots of weeks in a row with success.

2. The Compounding Risk of Rolling

- Rolling is a powerful tool for extending time and collecting additional credit.

- But when markets trend strongly downward, rolling losing positions can pile on losses beyond the initial capital at risk.

- Each debit roll or adjustment adds to the total exposure, creating the potential for losses larger than originally planned.

3. Worst-Case Scenario Planning

- Because this risk is always present, traders must plan for the worst case before entering any trade.

- Key considerations:

- Capital Allocation: Only commit a portion of trading capital to spreads.

- Reserves: Maintain significant additional funds to cover potential debits when markets drop.

- Stress Testing: Ask, “What if the market falls 10–20% quickly?” and size positions accordingly.

4. The Danger of Scaling Too Quickly

- In strong bull markets, spreads can feel like “easy money.”

- The temptation is to scale up aggressively—adding more contracts or larger positions.

- But without adequate reserves, a sudden downturn can wipe out gains and drain an account.

- Discipline is critical: growth in position size should be gradual, tied to account growth, and always leave room for survival in down markets.

5. Risk Management Principles

- Never risk capital you cannot afford to lose.

- Always keep reserves for unexpected market shocks.

- Size positions conservatively, assuming that multiple trades could go against you at once.

- Survival first, profits second. The ability to stay in the game matters more than maximizing returns in good times.

✅ Theoretical Risk Takeaway

Credit put spreads offer attractive returns on capital, but they are not without serious risks. The possibility of a total loss or compounding losses through rolling means traders must approach them with caution. Proper capital allocation, maintaining reserves, and resisting the urge to scale too quickly are essential to long-term survival.

⚖️ Practical Risk Considerations

Even with a disciplined rolling process, traders must recognize that credit put spreads are not immune to stress. A rolling credit put spread trader should expect to have their positions tested at least a few times each year. Most of these tests will resolve quickly, with the market bouncing back and the spreads returning to profitability. However, history shows that major market events can strain the strategy and consume significant debits to maintain positions.

1. Routine Tests vs. Major Events

- Routine Tests:

- Short-term pullbacks or volatility spikes.

- Typically resolved within days or weeks.

- Rolling through these events often adds credit and strengthens the position.

- Major Events:

- Large, sustained market declines can overwhelm the rolling process.

- In these cases, rolling requires substantial debit payments just to stay in the trade.

2. Recent Examples of Major Stress Events

- 2020 Covid Crash: A sudden, deep market collapse that forced traders to roll aggressively at heavy cost. You can read a post about how I chose to manage this at the time.

- 2022 Interest Rate Bear Market: A prolonged decline that steadily pressured spreads, requiring repeated debit rolls.

- April 2025 Tariff Scare: A sharp, sentiment-driven drop that tested positions quickly and consumed capital to maintain.

3. Implications for Traders

- Capital Reserves: Traders must maintain significant additional funds to finance debits during downturns.

- Expect the Unexpected: Even with a high-probability strategy, black swan events can and will occur.

- Survival Mindset: The goal in these scenarios is not maximizing profit, but minimizing damage and preserving capital for the recovery.

- Be prepared to take the heat: If the idea of sitting on a big loss that has the potential to get bigger is too much for you as a trader, this is probably not a good trade for you.

✅ Practical Risk Takeaway

Rolling credit put spreads work smoothly most of the time, but traders must be prepared for the occasional storm. Bear markets and sharp corrections will test the strategy, sometimes requiring large debits to stay in the game. The difference between long-term success and failure lies in planning for these events in advance—keeping reserves, sizing positions conservatively, and accepting that survival during downturns is the true measure of discipline.

📈 Expected Returns from Weekly Rolling of 5-Week Credit Put Spreads (Targeting 20/13 Delta with Leverage Amplification)

Rolling a 5-week credit put spread every week—anchored to a consistent delta profile (short leg near 20 delta, long leg near 13)—is a disciplined strategy designed to harvest time decay while staying exposed to directional drift. But the real engine of returns (good and bad) comes from the spread’s leverage, which amplifies modest index movement into meaningful position-level gains.

🔄 Weekly Return Mechanics

Each roll resets the clock and adjusts the strikes, allowing you to capture fresh premium and directional exposure. Returns stem from two primary sources:

- 🕒 Time Decay (Theta): ~1.0% per week

- With 5 weeks to expiration, the spread sits in the steepest part of the theta curve.

- Extrinsic value erodes faster on the short leg than the long leg, generating net profit.

- This decay is relatively stable and predictable—assuming the underlying stays above the short strike.

- 📊 Underlying Price Drift (Leveraged Impact): ~0.5–0.9% per week

- Indexes like SPX tend to return 8–15% annually, which averages to ~0.16–0.30% per week.

- With ~3x leverage from the spread structure, this translates to ~0.5–0.9% weekly gain in the position.

- This component is highly variable—some weeks may see sharp drawdowns, others strong rebounds. The leverage magnifies both. Many weeks may see profits or losses of 5-10% of the capital at risk.

📅 Long-Term Return Expectations

Assuming consistent weekly rolls and disciplined execution, the strategy can compound meaningfully as time passes and price movements average out:

| Component | Weekly Gain | Annualized (Approx.) |

|---|---|---|

| Time Decay (Theta) | ~1.0% | ~52% |

| Leveraged Price Drift | ~0.5–0.9% | ~26–47% |

| Total (Before Costs) | ~1.5–1.9% | ~78–99% |

⚠️ These figures assume ideal conditions averaged over time—no early assignment, consistent fills near mid-price, and disciplined roll logic. Real-world results will vary due to slippage, bid-ask spreads, and volatility events. Most importantly, results depend on the ability to withstand substantial drawdowns that can reach over 100% of initial capital used in this trade at times.

📉 Risk and Recovery Dynamics

- Initial Moves Often Down: Market shocks tend to hit quickly and hard. The spread’s leverage can amplify a 3% index drop into a ~9% position loss.

- Rolling Through the Dip: Weekly rolls reset exposure and allow participation in rebounds. A 2% index recovery can translate into a ~6% gain in the position.

- Volatility Spikes: Rising IV inflates put premiums, slowing decay and increasing unrealized losses. Rolling into lower delta strikes can help mitigate this, and when volatility ultimately collapses, credit put spreads will benefit substantially.

🧠 Mechanical Return Takeaways

This strategy is a short-volatility, time-decay engine with directional torque. Weekly rolls allow you to harvest theta while staying nimble enough to ride the bounce after market dips. The key is consistency: roll every week, maintain delta discipline, and treat each roll as a fresh trade. Over time, the compounding effect of small, leveraged gains can be substantial—especially when paired with robust risk management and capital buffers.

🔀 Variations on the Credit Put Spread Strategy

While the 20/13 delta, 4–6 week spread with weekly rolls is a strong baseline, individual traders may prefer to adjust certain parameters. These variations still follow the same core concept—defined risk, premium collection, and systematic management—but allow for customization based on risk tolerance, trading style, and market conditions.

1. Duration Choices

- Longer Duration (6–8 weeks or more):

- Slower time decay (Theta), smoother price movement.

- Requires less frequent rolling (e.g., every 1–2 weeks).

- Provides more time to react to adverse moves.

- Shorter Duration (7–14 days):

- Faster time decay, more rapid premium collection.

- Requires more frequent rolls—sometimes daily for 7 DTE spreads.

- Higher trading costs and more active management.

- Read more about 7 DTE trades here.

2. Delta Selection

- Lower Deltas (e.g., 10–15):

- Lower probability of finishing in-the-money.

- Less premium collected, slower decay.

- Often preferred for shorter durations to reduce probability of loss.

- Higher Deltas (e.g., 25–30):

- Higher premium collected, possibly more decay or profit from price moves up.

- Greater probability and risk of finishing in-the-money.

- Often works better with longer durations, where there’s more time to adjust.

- Key Watch-out: Regardless of delta, the possibility of total loss still exists.

3. Spread Width

- Wider Spreads (e.g., 10–20 Delta points):

- Behave more like naked puts, but with defined risk.

- Require more capital, reducing return on capital efficiency.

- Narrower Spreads (e.g., 1–2 Delta points):

- Lower capital requirement per spread, but less difference in Theta decay between strikes.

- Require more contracts to achieve the same return, which increases total exposure and transaction costs.

- Balance is Key: Too wide reduces efficiency, too narrow increases complexity.

4. Rolling Frequency

- Less Frequent Rolls:

- Lower trading costs, less active management.

- Risk of missing opportunities to collect additional premium.

- Market can move further against the position before adjustments are made.

- More Frequent Rolls:

- Keeps positions closer to ideal deltas.

- Allows for smaller, incremental adjustments.

- Increases trading costs and management effort.

- Guideline: Match roll frequency to duration.

- Roughly 1 roll per 4–5 trading days of duration.

- Example: 20 DTE → roll every 4–5 days; 6 weeks → roll weekly.

5. Rolling to Always Re-center

- An alternative to always collecting credit, is to always roll to target Delta

- Each roll, go out a week in time and choose 20/13 Delta, regardless of credit or debit

- Remains a mechanical process

- Keeps strikes near ideal decay parameters

- Avoid negative Theta

- Miss out on large rebounds after downturns

- Accept more debit rolls

6. The Importance of Understanding the Baseline

Before making adjustments, traders should fully understand why each part of the baseline trade is structured the way it is. Only then can variations be applied intelligently, with a clear understanding of the trade-offs involved.

✅ Variation Summary

Variations in duration, delta, spread width, and roll practices allow traders to tailor the rolling credit put spread strategy to their own style. But every adjustment comes with trade-offs—faster decay vs. more management, higher premium vs. higher risk, wider spreads vs. lower efficiency. The most important rule is to understand the implications of each change before implementing it, so the strategy remains mechanical, disciplined, and sustainable. As with all trades there is no “one perfect way” to execute a type of option strategy, but often there is a best way to optimize a strategy to an individual trader’s personality and risk profile.

🔄 Rolling Credit Put Spreads: A Wrap-Up

Rolling is the engine that powers a disciplined credit put spread strategy. By systematically extending time and re-centering strikes, traders can steadily collect additional credit while keeping risk defined. The key points to remember are:

- Mechanics: Rolling means closing the current spread and opening a new one in a single trade ticket. This keeps the position seamless and avoids exposure.

- Credit First: Try to always roll for a credit. When the market rises, roll strikes up to your target deltas. When the market falls, roll strikes down only as far as you can while still collecting a credit.

- Weekly Rhythm: A consistent cadence—rolling out one week at a time—keeps the trade aligned with your original setup and maximizes Theta harvest.

- Survival Mode: If a big move down pushes strikes in-the-money and Theta turns negative, rolling for credit is no longer possible. At that point, the trader must choose the least bad option: roll for debit, roll down for a larger debit, or close the trade to preserve capital.

- Capital Discipline: Rolling can compound gains, but it can also compound losses if not managed carefully. Always size positions with reserves in mind, and never scale too quickly in good times.

🌟 The Final Optimistic View

While survival mode scenarios are inevitable from time to time, the vast majority of trades will follow the smoother path: rolling week by week, collecting credits, and watching probabilities shift in your favor as time passes. With a mechanical process, disciplined capital management, and a clear set of rules, rolling credit put spreads can be a powerful, repeatable income strategy.

The real edge isn’t just in the spreads themselves—it’s in the trader’s ability to stay systematic, unemotional, and consistent. By mastering the roll, you transform a simple option spread into a durable, long-term strategy that thrives on structure and discipline.

Thank you, really appreciate your sharing! So each roll, need to keep the spread width the same, while collecting credits? Can enlarge the width when it’s hard to get the credit?

For simplicity, keeping the spread with constant works well. However, as IV changes, the Delta width also changes, so it may be tempting to widen or narrow to stay with target Delta. And as you suggest, widening the spread can make rolling down for a credit more likely.

A consideration is that widening the spread increases the capital required. But, when the market is down, IV usually increases, so the spread in Delta values may not increase that much. After widening a spread, look for opportunities in a future roll to narrow the spread back.

The key in deciding is to balance the trade-offs to determine which new position is the most comfortable for your risk/reward preference.

I see. This makes a lot of sense. Thank you!

So which option is better? Close at 21DTE or roll on weekly basis?

It sounds like you are asking whether continuous rolling is better than the “Tasty way.” There are a lot of commonalities between the approaches. Both work to avoid expiration drama. Both use timeframes in 3-6 weeks. Both are high probability of wins. The big difference that the Tasty version of enter at 45 DTE and exit at 21 DTE or 50% decay of premium is a single trade, while continuous rolling is well, continuous trading.

With the Tasty version, you have to decide when to enter the trade, but then the mechanics dictate exit at either 50% of initial premium, or when only 21 days are left. Once the trade ends, then what? Do you enter another one? When? Holding for the premium to decay by 50% can provide some big gains and exiting at 21 DTE prevents big losses. It’s a great strategy.

Rolling every week eliminates the decision of when to get in and out. Just roll every week. In a week, it is less likely to see really big wins or really big losses, as you might over 3-4 weeks in the Tasty version. But that is what appeals to me. Just stay mechanical.

Similar trades, with slightly different mechanical styles. Consider the trade-offs and choose the one that matches your trading personality better.

Agree! Staying mechanical definitely helps to control the greed and fear. Thanks a lot for replying. Big fan of your website.

Thanks for sharing your insights! On this comparison vs the Tasty approach: Understood, the weekly continuous approach leads to smaller gains and losses – but certainly also higher transaction fees?

Yes, transaction fees and commissions are a lot less than they used to be, but still add up to a significant amount, particularly if you are trading options on low priced underlyings, where the fees are a higher percentage of every trade.

Hey: Just discovered your website. Thanks so much for all you do. Learning a lot here. My bull put credit spreads are usually placed when stochastics are oversold and then closed when overbought, however rolling over seems to have a lot to offer. Question: here you write about rolling them over weekly. However here you are in a previous post: “The goal is to sell the options, have them decay for about three weeks and then buy them back for much less before they become volatile.” This seems to indicate a 21-day rollover.

Has your opinion and strategy changed? Or is this just another variation on the same strat? thanks again!

This is a variation of what I have written about earlier. I also tend to trade this later variation much more consistently than holding for several weeks, aka the Tasty Way. By mechanically rolling every week, I don’t have to worry about missing out on up moves that drop the premium to a point that there isn’t much decay left- I try to reset with each chunk that comes out. I can make smaller course adjustments and stay very mechanical and remain in the trade. Other versions take me out of the trade, and I then have to decide when to get back in. This appeals to me not trying to time the market, but instead taking what the market gives. It fits more with my trading personality.

Hello Carl, Thank you for a great website, sharing your strategies and writing highly educational articles! Re this strategy, what if you open a new trade once a week (same day every week) and follow the tasty mechanics (close at 50% or at 21DTE), so you may have 3 trades running simultaneously at a time. That way you are essentially recentering the deltas with each new trade. The risk exposure and capital is certainly higher with the 3 trades and you have already made the decision to close the trade regardless of the outcome at 21DTE. Have you considered this approach as well? If so, how would the results of this approach compare to your approach? Appreciate your insights. Thank you!

The beauty of option trading is that there are many ways to trade a given strategy. There are pros and cons to each way. I like rolling every week to keep it mechanical and not have to worry as much about big moves over time really changing my position a large amount between rolls. I used to like to trade closer to the “Tasty Way,” but I find rolling every week to be easier to manage with short amounts of time. But, that’s more of a personal preference than a statistically significant performance improvement.

Hi Carl, thank you for the insightful articles! I’m curious about your process—do you typically open your positions and perform your rolls on specific days of the week?

For positions I roll weekly like this rolling put spread strategy, I target to roll on Friday, but if the market is closed on Friday, or I have a conflict, I will move up and do my roll on Thursday. It is good to be mechanical, but timing isn’t super critical from my perspective for this kind of trade practice, which is one reason I like this strategy.

Hello! Just found your website and it is really informing! Thanks a lot for the effort you’ve put in!

Just a quick question, when the underlying breaches the short strike, would you say more often than not it is better to just close out the position instead of roll for a debit? Whether rolling down or rolling out?

Same goes for the “tasty method” if at any point before the “21 days” they have started, the underlying breaches the short strike, is it, in most cases, better to buy back the position or let it ride to expiration?

Oliver- thanks for the kind words. Great question.

Most people would say that when the market goes against you, it is best to get out at some point to save the capital you have left and pick someplace else to put your money. Once your strikes are in the money, the probabilities are that if you hold to expiration, you are more likely to have your position go to a full loss than to expire as a full profit. At any point in time, you have to consider that the market can go either way and it could get worse as easily as it could get better. For indexes, downturns eventually reverse, but do you have enough capital to wait to be right? For individual stocks, bad news can mean that a stock is down for months or years, or maybe forever. So, there are lots of reasons to set hard rules to get out at a certain amount of loss.

The contrarian view is that we are in an environment where we see rapid declines in the market based on odd news that panics the market, prices drop, and volatility spikes. These incidents for many have become buying opportunities. If you suspect that a situation is a short duration event, destined to reverse in short order, does it make sense to cash out with a big loss? Probably not. You may want to roll out, or roll out and down to get the strikes out of the money, taking a partial loss, and adding capital to the trade, essentially buying time to wait to be right. (Of course, others would term this chasing a loss, or digging a deeper hole.)

Part of this depends on what triggered the drop- did the president say something outrageous that could easily be reversed at any time? Or is it because of something systemic like inflation has caused the Fed to raise rates? Also, consider your timeframe- if you are trading 0 DTE, you don’t have time to wait. Even 7 DTE can be close when the market is tanking. But if the option expiration is weeks or months out, you have the flexibility to be thoughtful about the right move to make. It also matters how big the position is in your overall portfolio. A mistake with 1% of your account doesn’t hurt much, but messing up 50% of your account is extremely painful.

Finally, know yourself, and decide ahead of time what your plan is, and what the criteria will be for your decision. Then follow your plan. Evaluate and learn from your decisions- are you being impulsive, are you being lucky, are you being stubborn? Over time, adjust your plan when the market isn’t testing you. And realize, what to do when tested is only one of several factors to plan for in managing your portfolio and positions.