Many Procter & Gamble retirees hold legacy preferred shares with a unique tax advantage. This guide shows how to turn those shares into reliable income using a covered call strategy. If you worked at P&G, you probably hold PG stock in your retirement savings— not just as an investment, but as a reminder of the years you spent building brands people trust. This P&G covered call strategy lets you turn that legacy into a steady income stream without changing your long‑term relationship with the stock.

Using a combination of dividends and covered call premium, I’m collecting approximately 10% annual distributions from stock that I want to hold onto for the long term. This post is about a fairly specific situation that applies to current and former employees of Procter & Gamble, often retirees. Other option traders may be able to apply the same approach to parts of this approach, so I thought it would be valuable to share on this site.

Who This P&G Covered Call Strategy Helps

- P&G retirees with preferred shares

- Former employees who kept their Profit Sharing Trust

- Investors seeking income from blue‑chip dividend stocks

- Covered call traders who want low‑volatility underlyings

P&G has a bit of a unique retirement program that provides a special class of preferred stock to employees at a very low cost-basis. This opens up many opportunities for employees to handle their retirement in a lower tax scenario than most tax deferred retirement plans allow. There may be other companies with a similar plan, but not many. I’ll explain how I’ve chosen to manage this situation and why.

While every article on this site comes with a disclaimer that nothing here is to be construed as investment advice, I want to emphasize that with this posting. Not only is this not investment advice, it is also not tax advice. I’m sharing an approach that has worked for me. There are a lot of complexities to this specific approach, and readers should consult with their own advisors and accountants to see if this makes sense for each individual situation. I’ve read a lot about lump sum distributions of company stock from retirement accounts, but this is a bit of an additional nuance, so do your own research if you are considering this type of approach.

For those who don’t own P&G stock, you can ignore the gymnastics of getting preferred stock distributed out of retirement accounts, and focus on the call income and dividend part of the strategy, which applies to lots of stocks in virtually any kind of account.

The Procter & Gamble Profit Sharing Trust

Procter and Gamble has provided employees with company stock in their retirement accounts since 1944 as a way to share profits. The program is very generous. In the early 1990’s, the company transitioned a part of the retirement stock benefit to a new class of restricted preferred stock. These shares can only be held in employee retirement accounts, but can be converted to ordinary shares in certain circumstances. A large block of shares was set aside for this program and the shares are recycled in the program as retirees and ex-employees convert or cash out these shares, so the original cost basis of the shares remain intact within the P&G Profit Sharing Trust, which holds all employee retirement funds contributed to employees by P&G. When the shares are awarded to employees, they have a cost basis dating back over 30 years, which is now less than 5% of the stock price. Why is this important? Employees can take a distribution of shares from their retirement account for their preferred shares and only have to pay ordinary taxes on the cost basis of the shares, a small fraction of their now current value. Then, they have choices available to manage the shares in a taxable account and do many different things.

There are a bunch of rules about how and when to take total distributions of stock shares from a retirement account. In fact, there are long articles that you can read elsewhere on the topic, including in the Procter & Gamble retirement website, among other places. Suffice it to say that if done incorrectly, a person can end up with a very large tax bill. So, know the rules, or work with someone who does.

Here’s how I chose to manage the situation- this is not the only way to do it, but was my solution. I worked for many years at Procter & Gamble, until P&G made the decision to sell off the division of the company I worked for to another corporation. This divestiture happened well before I was retirement age, but I chose to keep my P&G retirement plan in place, mainly to hang onto the tax advantaged preferred shares in my account. In the years after leaving P&G, I decided to roll over the portions of my P&G retirement account that were not preferred shares, including my 401K contributions and the ordinary shares of P&G stock. All that remained were preferred shares. After turning 59 1/2, I took a full distribution of my preferred shares, and paid tax on the cost basis of the shares. The shares were converted to ordinary shares and were transferred to my taxable brokerage account at the low cost-basis that I had paid taxes on.

Doing this after age 59 1/2 was key due to IRS rules. A full lump sum distribution of this kind with this tax treatment can only be done one of three times- the first distribution transaction after retirement or separation, the first transaction after turning 59 1/2, or the first transaction by heirs after the death of the employee. Since I chose to roll over other parts of my retirement account early on, I had to wait until age 59 1/2 to take this lump distribution of stock.

After taking the stock distribution, I then had two accounts to manage from my days at P&G, my earlier rollover IRA with tax deferred holdings, and my P&G ordinary stock, now in a taxable account. My initial plan was to sell the stock as I needed cash and pay the tax on the long-term gain at lower long-term gain rates. I sold some shares early on and paid the low long-term tax rate, feeling good about saving taxes. Meanwhile, my roll-over IRA is all tax-deferred and will be taxed at ordinary rates when I withdraw from it. Eventually, I’ll be forced to take Required Minimum Distributions from my roll-over IRA and pay ordinary taxes on the distribution amount. I have much more flexibility with my P&G shares in my taxible account, now that they are no longer in a tax-deferred account.

But then I realized that I was giving up a low tax income source, the qualified dividends from the stock. P&G is considered a dividend aristocrat, increasing their dividend payments per share every year for something like 100 years. The current dividend yield is in the 2-3% range, depending on stock price, so dividend payments can be a nice source of income. Since the stock has been held for over a year, the dividends are considered qualified now that they are no longer in a retirement account, and the tax rate is the same as long-term capital gains.

Even though selling this stock would be taxed at a low rate, I’d have to pay tax on over 95% of the selling price due to the low cost basis. This goes against what many retirement planners assume with taxable stock that often hasn’t gained that much so selling is not a big income source. In my case, almost every dollar of the sale counts as income to be taxed and counted against things like Social Security tax limits and Medicare surcharges. If I hold it until I die, my heirs won’t pay any tax on the stock when they inherit it, so maybe that becomes the ultimate low tax choice.

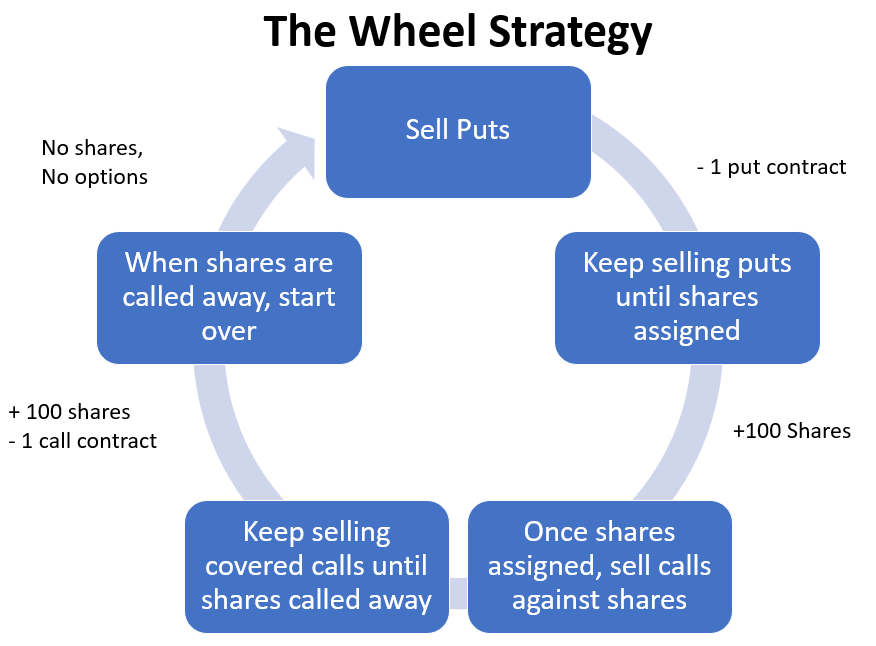

Use Covered Calls to Collect 10% Annually from P&G Stock

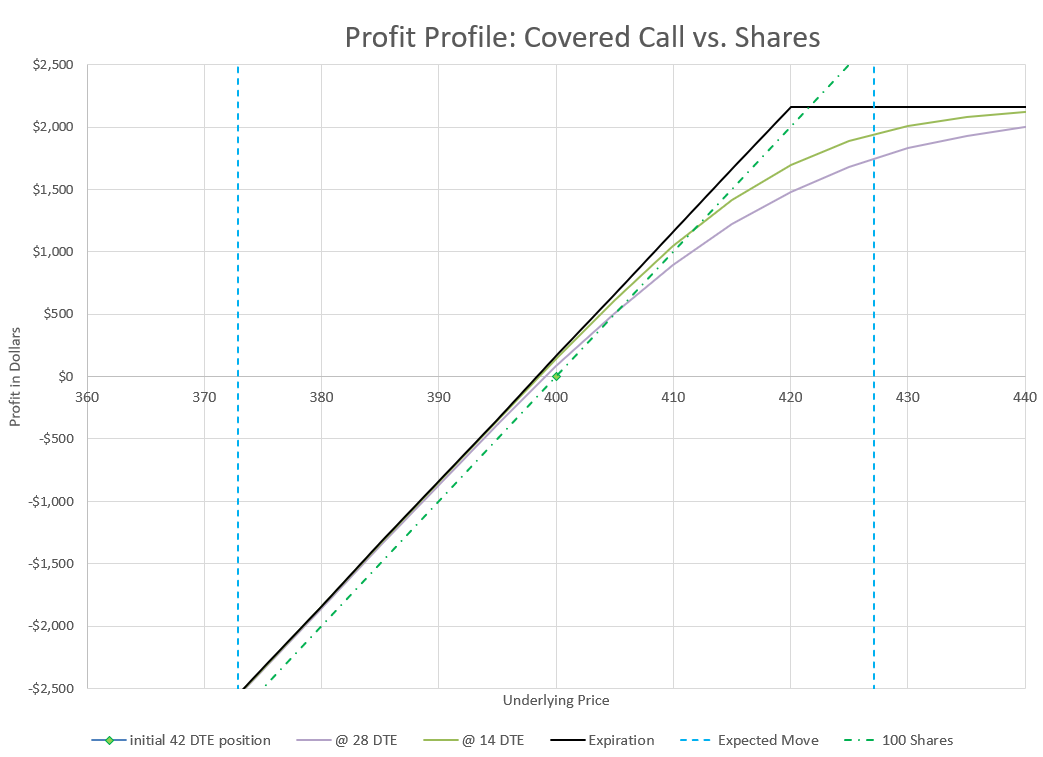

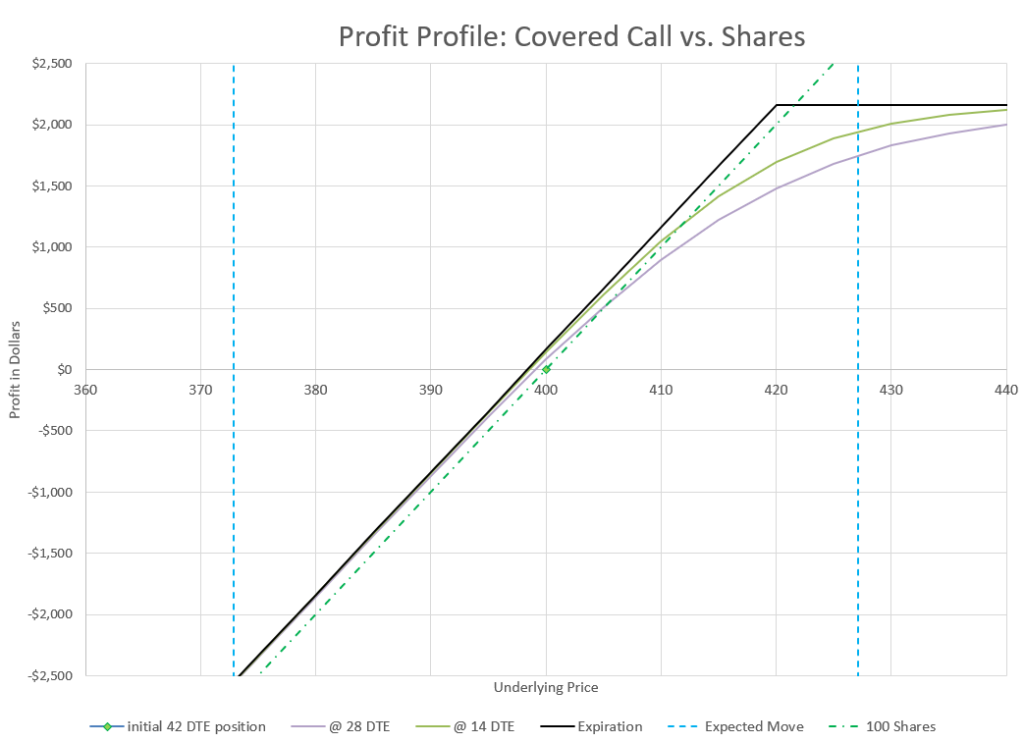

Now that I’ve chosen to keep this stock, I want to get the most I can out of it, so in addition to the qualified dividends the stock pays, I decided to start writing covered calls to collect additional cash. This is the part that applies to owning any stock. My goals with my covered call strategy is to collect call premium, never lose shares, never touch the principal value of the shares- letting them grow in value over time, and as much as possible never pay a debit to roll my positions.

I’ve written about selling covered calls elsewhere on this site, as well as on rolling covered calls. This is a specific and practical version of the strategy.

I started small at first with contracts on a few hundred shares, but realized that the combination of dividend and call premium profit was netting around 10% of the stock value for the shares I was selling calls against. My expectation is to net 6-10% from covered call premium per year, with some even better and some worse.

Keep in mind that this income stream works somewhat inverse to price action of the stock, making more money when the stock stays flat or goes down and potentially losing money (at least on paper) when the stock goes up. But this is the nature of covered calls, where the negative Delta of the short calls counters the positive Delta of the long stock. The net result is that the total position is less volatile than stock alone. Delta is the option Greek that represents how much an option changes in premium value for every dollar of stock price change, and also represents the probability of an option expiring in the money.

Another point to consider is that the short calls produce positive Theta, the decay in premium that happens day after day. Theta is maximized with at-the-money strikes, and minimized as the Delta values approach extreme values of zero or 1. No matter where the strikes are, decay will keep working in my favor. Theta is the option Greek that represents the daily value of option premium decay.

Choosing Delta and Expiration for PG Covered Calls

Selling calls is a balancing act. We want to collect a lot of option premium, but we don’t want to end up in the money if we can help it. Many call sellers sell fairly far out of the money calls, trying to avoid the risk of getting in the money. It is something of a personal preference and also depends on how a trader plans to manage the trade. If the plan is to hold to expiration most of the time, low Delta, far out of the money is definitely the way to go. If you’ve read very many of the other articles on this site, you’ll know that my preference is to roll out options well before expiration in all scenarios- win, lose, or draw.

For traders that want to hold until expiration, one fairly popular trader I know suggests that 0.12 Delta is ideal. This equates to a 12% probability of expiring in the money, which would mean having the stock called away. So, if a trader doesn’t want to lose the stock, there will have to be at least an occasional intervention before expiration to avoid losing the stock. We’ll discuss preventing option assignment more in a bit.

In this particular situation, I take a significantly more aggressive approach, selling calls with Deltas between 0.25 and 0.40. If I were starting a position, I would base my decision on how the stock price is performing compared to its long-term trend. Are we at all time highs, or perhaps at relative lows? If we are bumping up near the top of the long term trend, then I’m more comfortable selling the high end of my range, around 0.40 Delta. If we are bottomed out, I’ll be more cautious and shoot for a Delta that has more cushion like 0.25. You can find the Delta value of the option strikes in your trading platform.

Part of my reasoning is that with a blue chip stock like Procter & Gamble, I don’t expect to see crazy swings. It does go in and out of favor, often trading as a safe haven when trendy stocks are in trouble and trailing when new shiny things are all the rage. These seasons shift back and forth over time, and P&G also has times where results are challenging and other times when profits and volumes are outperforming. There are other stocks that fit this persona, but P&G is about as stable as they come. People always need soap, toilet paper, and grooming products. Anyone remember the Covid toilet paper shortage?

A good math check is to look at the target income of the calls. If I want to collect a target of 10% total income on a $150 stock (generally where P&G is trading in 2026), I’m looking for $15 per share over the year. Annual dividends are around $4.50, so I’m looking for $10.50 from call income. Let’s keep the math simple, so let’s look for $12.00, or $1.00 per month. With 30 days a month, we need to make $0.033 per day over time, $0.25 per week. So, I’d like to get my rolls to make $0.25 for every week I roll on average, and I’d like my Theta to be at least $0.033 per day. This gives me two targets to aim for in my call holdings and in my trades. I won’t hit these targets all the time, but each time I look at my account and see my Theta values, I can see if I’m on track, and every trade is either helping or hurting the average. As I write this, my P&G call Theta value is 0.045, so pretty close to where I want to be. You may find your Theta value multiplied out for 100 shares per contract, or in my case $4.50 per contract which gets back to $0.045 per share. These values will vary over time, so don’t get caught up if the rolls or Thetas are too low- the goal is for them to average out at our target over the long haul.

What expiration date is best?

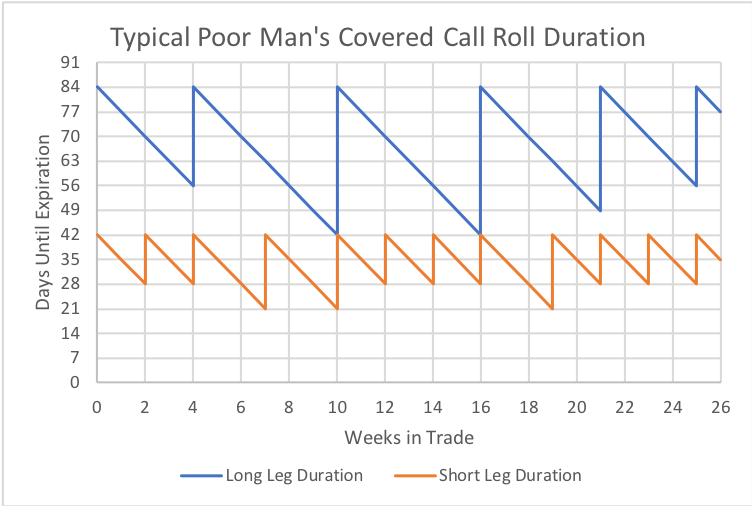

Options for Procter & Gamble stock are available for monthly and weekly expirations. Currently, weekly expirations are available to about 5 weeks out, monthly expirations are available to about 6 months out for every month, and every third month beyond that out for a few years. Knowing what expirations are available helps with being able to plan a management strategy.

Option traders know that the shorter the option duration, the greater is Theta, the decay of premium. But, the shorter the option duration, the more quickly Delta can change and an option can go from out of the money to in the money very easily. The option Greek for this phenomenon is Gamma, so short duration options tend to be loaded with Gamma risk.

Given the choices of expiration dates, I like to have my P&G options in the 3-5 week timeframe most of the time. I’ll open each option trade with 4-5 weeks left to expiration, and roll out a week or two when the option gets around 3 weeks from expiration. I know others like to go a bit longer and aim for the “TastyLive.com” timeframe of 45 to 21 DTE with less adjustment. Since 45 days is 6.5 weeks, and P&G weekly options go out only around 5 weeks, rolling to 45 days is not always an easy thing to do, which is why I like to stay in the 3-5 week timeframe as much as I can. Either way the concept is the same- avoid expiration and also minimize option assignment risk.

Always roll for credit?

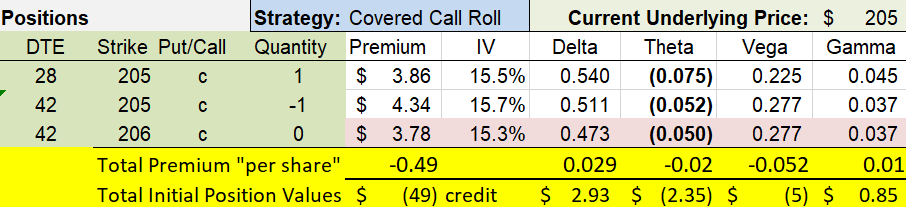

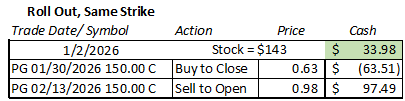

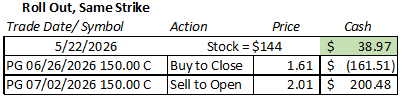

My plan is to always roll out my option expiration for credit, selling the longer dated option for more than I pay to buy back the shorter dated option. This is almost always possible at the same strike price. If my options contracts are in the 0.25 to 0.40 Delta range, I’ll likely roll to the same strike. For example:

In these real trades illustrating the cash flow of one contract, I rolled out a week or two, collecting a credit by increasing time until expiration.

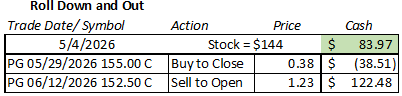

If the stock price has dropped to bring the Delta value below 0.25, far enough that my roll would be to a position with a Delta not above 0.25, I’ll look to roll down a strike and collect more premium. For example:

Rolling strikes down and out will create a bigger credit than the same strike.

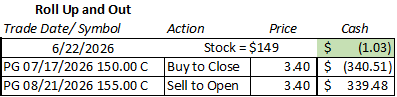

For a price move up that brings the Delta above 0.40, it becomes more challenging. In that situation, there are two objectives for a roll, collecting a credit and reducing Delta. This can become a challenge, as reducing Delta requires rolling up to higher strikes that have less premium value. To get a credit for a roll, it may require going out further in time, so instead of 5 weeks, it may take going out to the 2-3 month range to collect a credit. For example:

In this example, I rolled out a month to roll up and sell for the same price as I paid to close the nearer expiration. The only cost was my commission, but I was able to keep my strikes out of the money at least for the moment.

What’s the plan when the stock goes on a big run up, or a big run down? The strategy of adjusting strikes with each roll is fairly straightforward when stock price moves are 3-5%, but when moves are over 10%, it may not be possible to remain in the 0.25 to 0.40 Delta window and still collect a credit. So, which objective is more important? Let’s look at both types of extreme moves and consider appropriate strategy.

The easier situation would look to be a big down move. When the stock moves down a lot, we can just roll down our strikes, right? Yes, we can, but it warrants caution to not over roll down too much. Big moves down can be overdone, and if strikes are rolled down too far, the option position is susceptible to a price whipsaw, where stocks bounce off the bottom bringing the options in the money- the more difficult situation to manage. So, my approach is to roll down gradually, perhaps one strike down on each roll. In doing this, Delta will be less for a time, but most whip-saw events can be manageable. If Delta drops below 0.10, then I’m willing to roll down a bit more to get the Delta value up above 0.10, but that doesn’t happen very often.

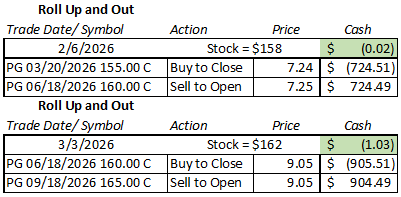

The more difficult situation is when the stock price jumps up unexpectedly. With a stock like P&G, this doesn’t tend to be dramatic like we might see in a tech stock or other economically sensitive stocks. But, it can happen. Going back to the earlier discussion, there continues to be two objectives, reducing Delta and collecting a credit to roll. Notice that I don’t include keeping the Delta under 0.40. While that is my target, I don’t have to get there with every roll. This strategy is a long-term, almost “forever” plan, so there’s no need to panic. I look to chip away at whatever gap there is between the strike price and stock price one roll at a time. Even if the strike prices are in the money, I’ll try to roll up a strike at a time in exchange for a month or two of expiration. I may allow my expirations to get 3-6 months out in extreme situations, but at that point, I’m generally satisfied to wait things out. For example:

Here, I rolled up and out twice, rolling from in the money to out of the money each time, for an even or nearly even trade. After the second trade, my expiration date was six months out.

While I haven’t seen it happen with P&G, other stocks that I’ve sold covered calls have moved up fast enough to get to Deltas of 0.80 or 0.90, which is where I start to consider paying a debit to roll up my strikes to a level where there is more decay and more manueverability. In those situations, I’ll look to roll to Delta values in the 0.70 to 0.75 range, chipping away but not making a dramatic move.

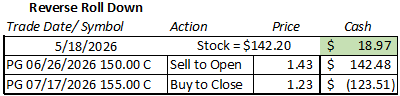

Reverse Rolls Back in Time?

A key reason not to over-adjust up is that big moves up are often not sustainable. Paying a debit to get out of the money may end up being a cost that ends up a regret a short time later when the price corrects back to the long-term trend line. Being patient with in the money short calls can occasionally offer a unique opportunity to roll backwards in time.

I’ve experienced a few situations where I’ve rolled out 4-6 months out to keep rolling up my calls and collect credit when stock has gone up a significant amount in a short time. Then, the stock drops as much as it went up after a time, and I’m left with option strikes way out of the money with a long time until expiration. In this situation, I could just sit and wait for time to catch up with my expirations, but there is no income to collect by doing that. Rolling even further out doesn’t make sense, and even rolling down in the same expiration doesn’t provide that much credit.

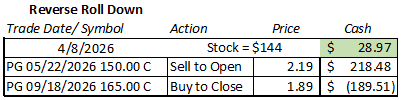

I’ve found that I may have the opportunity to roll backward in time to a nearer expiration at a strike closer to the current price and collect a credit. I may be able to buy back a 6 month to expiration call with a 0.15 Delta and sell a 5 week to expiration call with a 0.30 Delta for more, a net credit. This tends to be fairly easy when the market shifts down.

By rolling back in time, I was able to collect a credit here and also be able to get back on a regular schedule of rolling for credit every week or two. I also returned to target Delta values.

Even shaving three weeks off can be helpful to keep collecting regular premium.

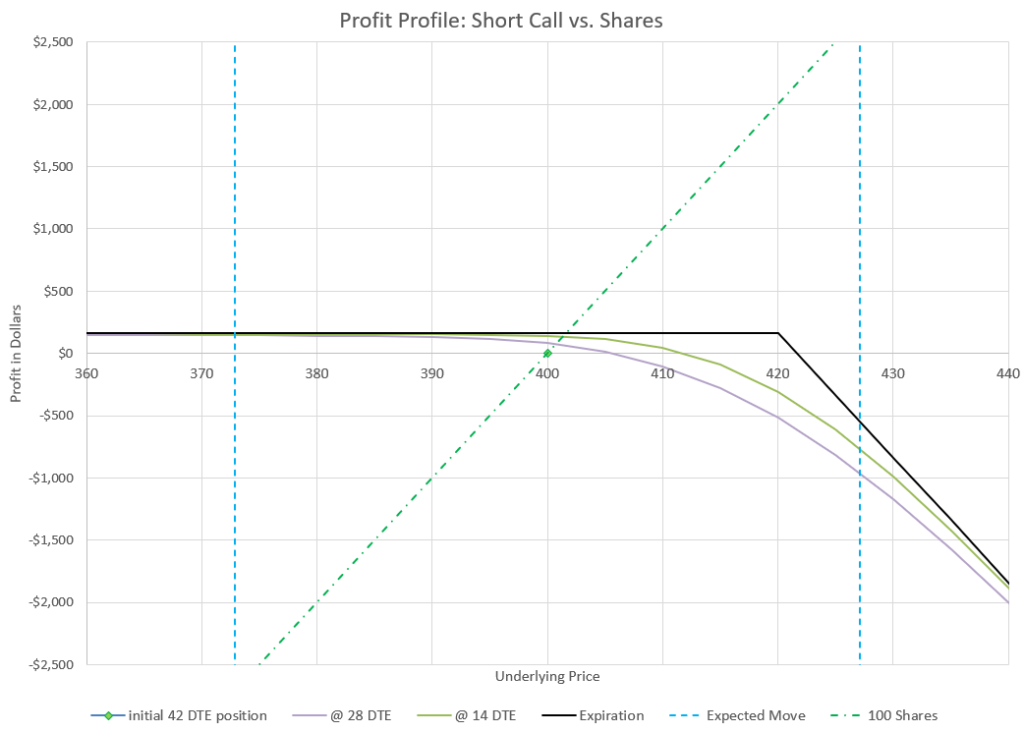

Avoiding Assignment When Selling Calls on Dividend Stocks

One possibility that a strategy like this has to stay vigilant for is avoiding option assignment. If you sell (write) call options on Procter & Gamble (P&G) stock, you are obligated to deliver the underlying shares if the buyer exercises the option before expiration. Since our plan is to hold the shares to avoid recognizing the large capital gain on the shares, we definitely want to avoid this.

So, when do call buyers exercise their option? Buyers almost never want to exercise a call option early — even on a slow‑moving, dividend‑paying stock like Procter & Gamble (PG) — unless a very specific set of conditions is met. Exercising destroys remaining time value, so it’s usually the least efficient way to use a call. But, there are a few situation where they will exercise the option, and as a seller that wants to hold onto shares, these are almost completely avoidable. Here are exercise scenarios to avoid:

- Call expires in the money. If the option contract expires and is in the money, the option will be exercised, and the shares will be sold and assigned to the call buyer. Even if something happens after the market closes that makes the stock worth more than the strike, the buyer can choose to exercise their option. Avoiding this is easy- don’t hold your options through expiration- either close or roll the contracts well before expiration. I try to keep my P&G options at least 21 days from expiration, so I never worry about this.

- The call is deep in the money AND has almost no extrinsic value. If the call is:

- Deep ITM (e.g., PG at $170 and buyer holds a $120 call)

- Near expiration

- Extrinsic value ≈ $0.05 or less

…then exercising is effectively the same as owning the shares, and the call buyer is not giving up meaningful time value. If the call has no time value left, the buyer is not “wasting” anything by exercising.

As a seller, we avoid this a couple of ways: - If the option is getting so deep enough in the money that Delta is up to 0.80 or above, we may consider rolling up for a debit. However, if there is still lots of extrinsic (time) value, this may not be necessary.

- If we’ve rolled way out, we won’t be close to expiration, and we’ll have plenty of extrinsic value- we used that time premium to roll up and out when the strikes went into the money. Our management strategy fixes this almost automatically if we follow it.

- If a call contract is deep in the money, check the extrinsic value periodically to make sure it doesn’t get low enough to be attractive for a call buyer to exercise.

With lots of time until expiration and a Delta that isn’t approaching 1.00, it is extremely rare that a buyer will exercise their option.

- Call buyer wants to capture the next dividend. P&G is a reliable dividend payer. This is the trickiest one to avoid when not paying attention. If:

- Your call is in the money,

- Extrinsic value < dividend amount, and

- Ex‑dividend date is tomorrow,

then early exercise can make sense to the call buyer and chances are high they will exercise.

For example: PG dividend: ~$0.94 per share and your call’s extrinsic value is $0.20, the call buyer would gain $0.94 but give up only $0.20 → net +$0.74. This is the classic early‑exercise scenario for dividend stocks.

To avoid this: - Know when the stock will turn ex-dividend. This is the date when shareholders of record will be allotted their dividend amount which will be paid to them a few weeks later. P&G currently pays a dividend of a little over $1.00 per share per quarter, so the stock price will drop by around $1.00 per share when the stock turns ex-dividend. These dates are usually around late January, April, July, and October.

- As the ex-dividend date approaches, if the covered call strike price is in the money or close to in the money, roll out the strikes to a date that has more extrinsic value than the anticipated dividend. Allow some margin here. If the dividend will be $1.10 and the extrinsic value of the call is $1.15, get more extrinsic value so that even with decay, there is no advantage for a call buyer to exercise to collect a dividend. If the call is close to being in the money, it could move in the money at the point when the dividend is assigned, so make sure there is enough extrinsic value just in case.

Like the other scenarios, keeping covered calls from nearing expiration helps prevent option exercise to capture dividends. Time alone is not sufficient here- a call seller needs to pay attention to the math.

There is no absolute guarantee that a seller of covered calls won’t ever be assigned to sell their shares by a call buyer exercising their option rights, but by knowing the scenarios that lead to exercise, we can steer clear of any situation that would give a call buyer a legitimate reason to exercise. Keep away from expiration and pay attention to dividend dates.

Long‑Term Income Strategy with P&G Covered Calls

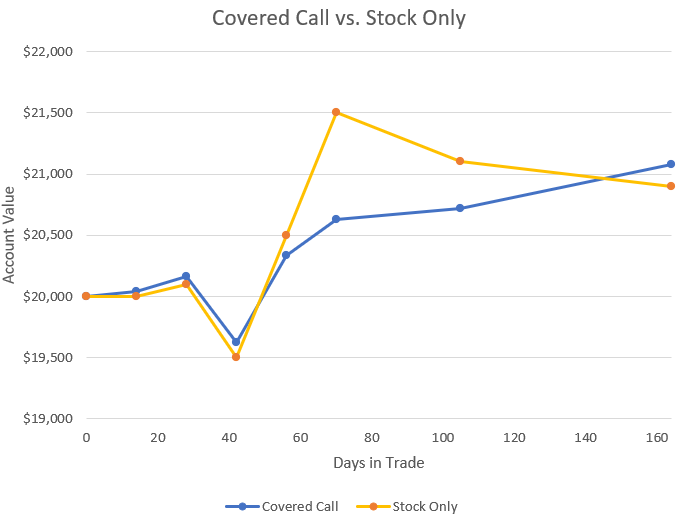

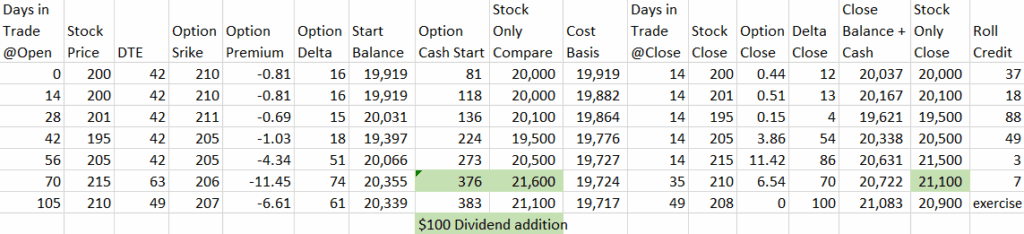

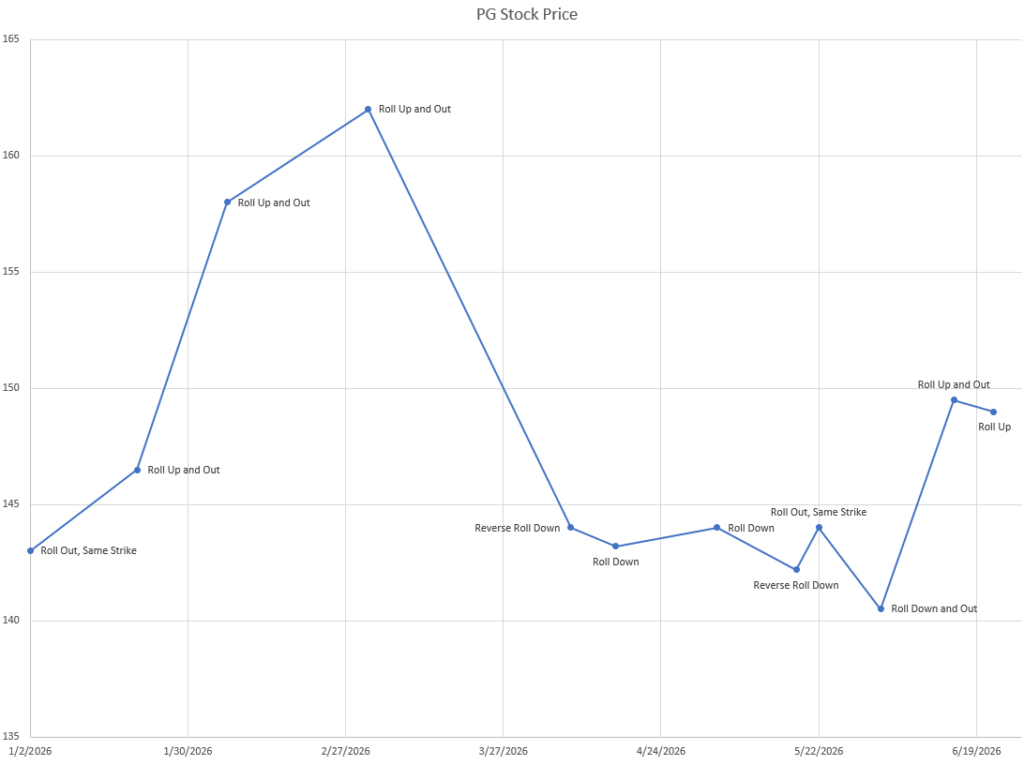

As we’ve reviewed different scenarios, I’ve shown trades that I did using each type of roll. If we look at a stock price chart with each point where I made a rolling trade, you can see how the price action of the stock drives option rolls.

The rolling covered call strategy is one of simply responding to price movement of the stock. Here we see a series of data points where rolls occurred. Every roll captured a net credit or was done break even. The comment by each point shows the type of roll done.

The key thing is that in each roll, I’ve

- Collected a credit, or rolled for an even trade while rolling up strikes.

- Kept my expirations out in time at least 3 weeks.

- Kept my extrinsic/time value greater than any anticipated dividend.

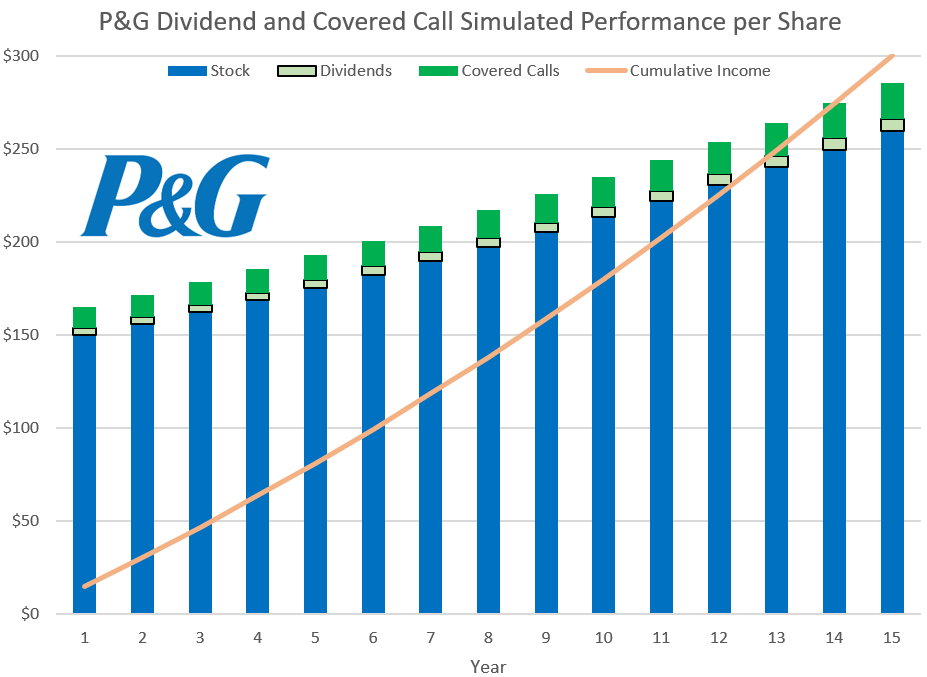

While I’ve tried to keep my Delta values in my target range, I didn’t let that objective over-ride the key items above. And as the market goes up and down, I collect call credits month after month, sometimes a little, sometimes more. The credits from rolling calls in this way isn’t predictable in the short term, but over time they average out to an income that exceeds the income from the dividends, which I also get each quarter.

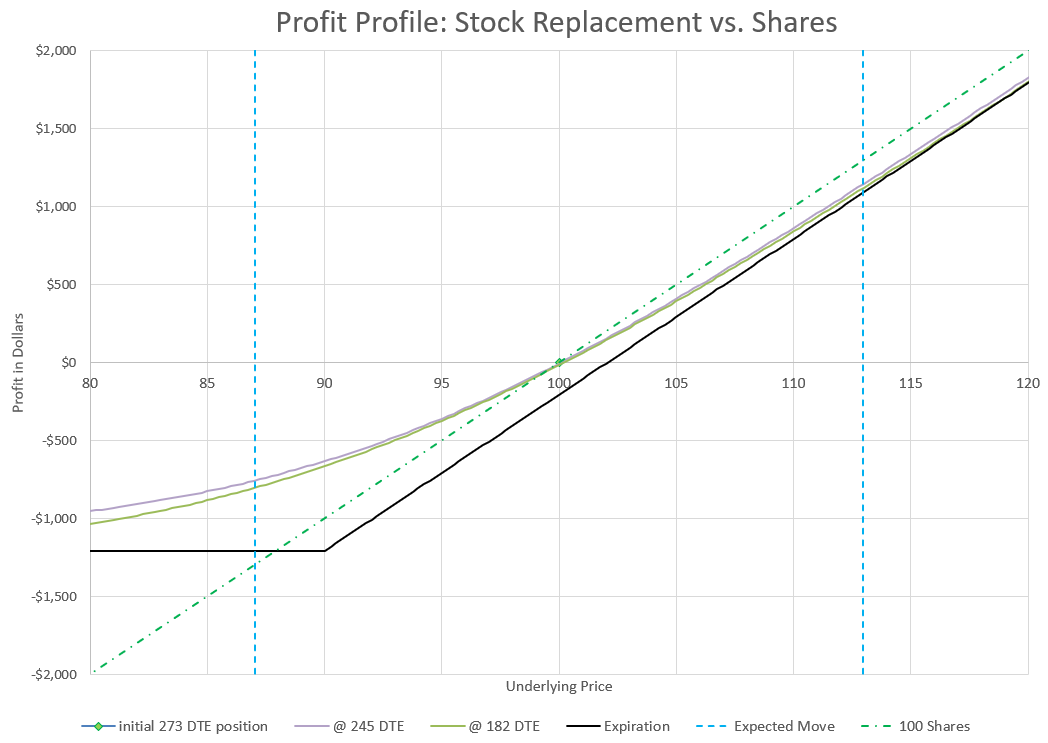

For some people this may seem like a lot of work for a relatively small return. Others may think it is too risky or maybe stressful to keep up with. I find it a relatively simple way to make a little extra income on stock that I want to keep for the rest of my life. For perspective, I’m aiming to make a 10% income return annually, while not touching principal- most people would be thrilled to pull that off. Let’s go back to the featured chart from the beginning:

If it isn’t clear from the write up so far, there are three ways this strategy is making money over time, beyond the long-term tax avoidance.

- Long term appreciation of the stock itself. This strategy isn’t really concerned with this, but if I didn’t think the stock would go up over time, it wouldn’t make much sense to hold onto it. But, because I am holding on, I can tolerate long periods of years of no growth or even down markets. I choose not to worry about it and trust that this blue chip stock will stay a blue chip as it has for over a century. My goal is for my heirs to inherit this stock with no tax to them on the value they inherit it.

- Dividends every quarter. P&G is a Dividend Aristocrat, raising its dividend every year for decades, longer than I’ve been alive. Currently, the yield is between 2-3% and since my shares are in a taxible account, they are taxed as qualified dividends. This is as close to a constant source of low-tax income as you can get from a stock.

- Income from selling calls. This is the subject of this whole write-up, but I’m listing it here to show that it is just part of the bigger picture. There will be substantial variation from month to month or even year to year, but my objective is to make 6-10% a year from selling calls that I plan to never let be assigned. It isn’t “free money” because I could get assigned at some point for a reason out of my control, but I’m happy to collect call premium and watch the calls’ value decay over and over for as long as I can. This is short-term ordinary income, so I pay my top tax rate on this income, but I’m okay with that- not every source of income has to be low tax or tax free.

So, I kind of look at this strategy as holding stock for my heirs, and it paying me rent for the privilege. It’s kind of like having a paid off rental property- collecting rent that slowly increases over time, while the property itself also gains in value. Even so, eventually the total income I get from this strategy could add up to more than the increasing value of the stock.

Why P&G Preferred Shares Create a Unique Covered Call Opportunity

I used to not be a big fan of selling covered calls because I ran into so many situations where calls went into the money, forcing a decision of whether to let the stock be called away, or to close or roll the calls for a loss. In high-flying stocks, this can be an issue, as well as in index ETFs. But, even when a covered call goes into the money, it is important to remember that the total position is making money because the stock is increasing more than the call is losing, plus there is always the gain from extrinsic value decay of the call. But I see blue chip stocks paying dividends as somewhat as an ideal case for covered calls. Let’s go through why.

Volatility: The “Goldilocks Zone” Compared to Other Underlyings: One of the biggest challenges with covered calls is dealing with stocks that move too much or too little. High‑flyers like Tesla or Nvidia offer enormous premiums, but they also have a habit of blowing straight through strikes. Selling calls on those names becomes a defensive exercise—you’re constantly rolling, adjusting, or deciding whether to let shares go. On the other end of the spectrum, broad index ETFs like SPY or DIA barely move at all, and their implied volatility is so low that the premium you collect often isn’t worth capping your upside. P&G sits right in the middle. It has enough implied volatility to make selling calls worthwhile, but not so much that you’re fighting runaway upside every month. It’s a “Goldilocks” underlying: not too hot, not too cold, and just volatile enough to pay you for your trouble.

Dividend Mechanics: Why Income‑Heavy Stocks Fit Covered Calls Better Than Growth Stocks. Covered calls work best when the underlying stock’s return profile leans toward income rather than explosive price appreciation. Growth stocks that pay no dividend rely entirely on price movement to reward shareholders. When you sell calls on those names, you’re capping the only engine of return they have. That’s why covered calls often feel counterproductive on high‑growth companies. Dividend stocks flip that equation. A large portion of the shareholder return comes from the dividend itself, not from rapid price appreciation. P&G is a textbook example. Its dividend is stable, predictable, and a core part of the company’s identity. Because so much of the total return is already delivered through cash payments, the stock doesn’t need to sprint higher to satisfy investors. That slower, steadier price behavior makes covered calls far more forgiving. You’re stacking option premium on top of a dividend that’s already doing most of the heavy lifting.

Assignment Risk: Why P&G’s Price Behavior Makes Covered Calls Less Stressful. Assignment risk is one of the main psychological hurdles for covered call sellers. In high‑beta stocks (ones that move much more than the overall market), even strikes that look safely out of the money can be breached in a single news cycle. Index ETFs don’t have that problem, but they also don’t pay enough premium to compensate you for the risk of losing your shares. Dividend stocks introduce another wrinkle: large dividends can trigger early assignment around ex‑dividend dates. P&G avoids most of these issues. Its dividend is meaningful but not so large that it routinely causes early exercise. Its price moves are orderly and rarely violent. You can sell calls closer to the money without constantly worrying about surprise upside explosions. The assignment risk is manageable, predictable, and easy to plan around—exactly what you want when running a systematic covered call strategy.

Price Behavior: Range‑Bound Stocks Are the Natural Habitat for Covered Calls. Covered calls thrive when the underlying stock spends long stretches moving sideways. Trend‑driven stocks—especially in tech or biotech—tend to grind higher for months at a time, and selling calls on them becomes a battle against the trend. You’re always rolling up and out, and you often give up more upside than you collect in premium. Cyclical stocks can be just as difficult, because their rallies and selloffs are sharp and unpredictable. P&G’s price behavior is different. It tends to move in a slow, mean‑reverting pattern. It has long periods where it trades in a well‑defined range, and even its earnings reactions are usually contained. This kind of price action is ideal for covered calls. You can sell calls weeks to months out and expect the stock to stay in a tradable zone most of the time. Slow and steady really does win this race.

Liquidity and Options Market Structure: Why P&G Is Easy to Trade and Easy to Manage. Liquidity is an underrated part of covered call performance. Small‑cap stocks may offer attractive premiums, but their options often have wide bid/ask spreads and thin open interest. Rolling or adjusting positions becomes expensive and frustrating. Mega‑cap tech stocks are extremely liquid, but their volatility makes rolling a constant chore. P&G offers the best of both worlds: tight spreads, deep liquidity, and plenty of open interest across strikes and expirations. When you need to roll, adjust, or reposition, you can do it cleanly and cheaply. P&G is one of the 30 stocks in the Dow Jones Industrial Average, and one of the longest continous ones to boot, one of the blue-est of the blue-chips. This makes the strategy more mechanical and less stressful, which is exactly what you want when building a repeatable income process.

Investor Base: Why the Type of Shareholder Matters More Than People Realize. The behavior of a stock is shaped by the people who own it. Speculative stocks attract traders, momentum chasers, and short‑term thinkers. That creates rapid price swings and unpredictable spikes—conditions that make covered calls difficult. P&G attracts a completely different crowd. Its shareholder base is dominated by long‑term dividend investors who value stability over excitement. That investor profile naturally dampens volatility and reduces the likelihood of sudden upside blowouts. When you sell calls on P&G, you’re operating in a calmer ecosystem. The stock behaves like a utility: steady, predictable, and slow to react. That stability is a hidden advantage for covered call sellers.

Total Return Profile: Covered Calls Fit Perfectly Into P&G’s Return Mix. When you look at P&G’s long‑term return profile, it’s built on three pillars: modest price appreciation, steady dividends, and low volatility. Covered calls slot neatly into that structure. You’re not capping a rocket ship; you’re enhancing a stock that already delivers most of its return through income. The premium you collect becomes a third income stream layered on top of the dividend. In many cases, the combined yield resembles a high‑yield equity strategy—but without the credit risk or business instability that usually comes with high‑yield stocks. This is one of the strongest arguments for using covered calls on P&G: the strategy complements the stock’s natural behavior instead of fighting against it.

Active management by rolling up and down before expiration protects shares. While P&G stock is not a fast moving stock for the most part, it does moves up and down based on company news and as part of the overall market. So, blindly selling calls could easily result in either having stocks called away, or collecting very small premium, or in a worst case scenario, both. That’s why actively managing call strikes by rolling strike prices and expirations is needed to keep collecting premium, and keep the shares out of call buyers’ hands as much as possible is so critical and is key to this strategy.

There are a lot of reasons to hold a stock long-term that are similar to this specific situation. This three-way profit strategy could be used in many different situations with many different stocks. The P&G covered call strategy is a powerful way for retirees to turn legacy preferred shares into steady income while preserving long‑term tax advantages. You don’t have to be a P&G retiree to use a strategy like this. Any steady, stable stock will do. So, if you happen to be in a similar situation, this approach might be for you.