After trading put spreads for several years, I’ve noticed that some rolls collect a lot of premium credit, and others are a struggle to collect any credit at all. I decided to study this to see if I could find if there is a “sweet spot” for rolling put spreads based on Delta values. I’m happy to report that there is.

It’s no secret that if a put spread gets fully in the money, it is impossible to roll to the same strikes in a later expiration for a credit. But when a spread is out of the money, I’ve seen a wide variation in credit when I roll, and I’ve often thought that there must be a best place to make a roll to get the most credit. If there is, I could devise a strategy to take advantage. So, I copied some option tables into Excel and pivoted the data a few different ways to figure out how premium from rolls vary.

Before jumping into the study, let’s discuss what rolling option spreads involves and why we might do it when a spread is out of the money. Rolling is one three ways to manage an exisitng trade- I covered the three ways in the page on managing by holding, folding, or rolling. One of my common management techniques is to continuously roll a position- I let the short spread decay in value, then roll it out in time to get more premium, and then let it decay all over again. Just repeat over and over. For those not familiar with the roll concept, rolling means executing a trade where an existing position is closed and a new position is opened all at once in one trade. The new options may be at the same strikes, which would be rolling “out,” or the strikes may be higher, which would be rolling “up and out,” or we could also roll “down and out.” Rolling a credit put spread that is out of the money out to the same strikes, will almost certainly generate a credit, which is the goal of this strategy. I’ve discussed this -approach in detail in other pages of this website, including roll for 6 percent a week, goals for rolling Iron Condors, the power of rolling Iron Condors, and rolling losing positions.

Rolling Spreads in the Study

I looked at a lot of different combinations of rolls, different durations, different times between durations, and I saw similar results. In the interest of keeping this write-up from getting lengthy, I’m choosing to just show a few examples.

7-10 DTE Roll

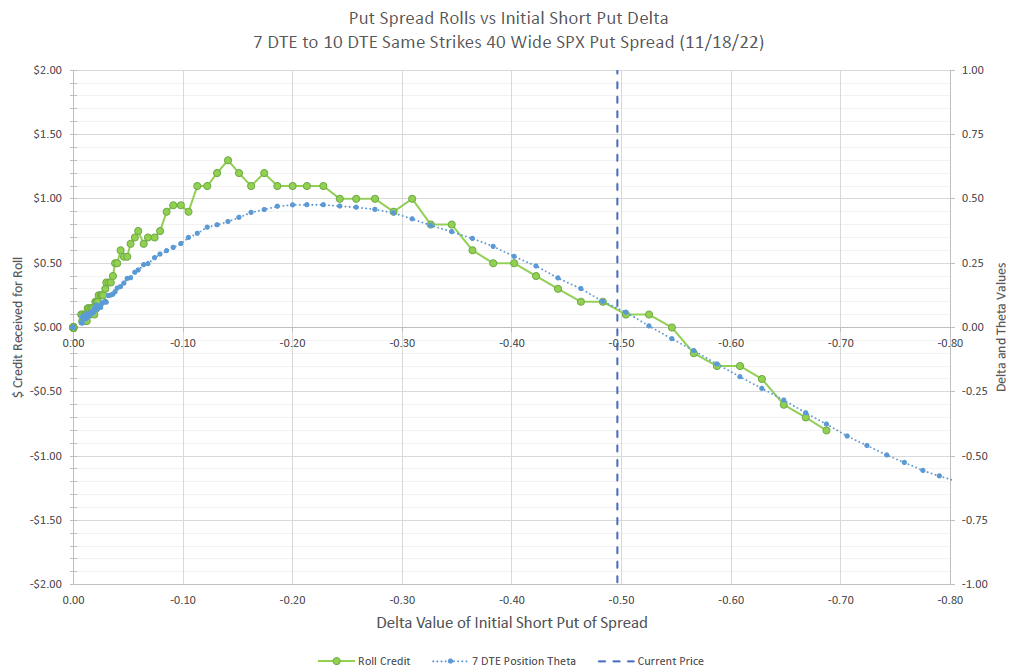

While I don’t trade a lot of options with durations of a week or less, I thought it would be good to look at this timeframe as the lower end of timeframes where we get outside of current week expirations. The following chart shows all the available combinations of 40 wide 7 days to expiration (DTE) SPX credit spreads rolling to the same strikes at 10 DTE.

I’ve shown the net credit for each roll combination, as well as the raw Theta difference for each existing 7 DTE 40 point wide spread. The x-axis is the Delta of each 7 DTE spread. The roll credit is shown on the left axis, and the net Theta is shown on the right axis. Looking at a peak value of approximately $1.20 per roll, we would collect 3% of the 40 wide spread. Meanwhile, the peak Theta of around $0.45 per day would equate to 1.1% of the width. So, holding might get a similar daily return, but with increasing risk as expiration approaches, but a roll would allow us to collect 3% and still collect additional Theta over again. Actually, that’s double counting. The Theta would just be the decay of the premium we are collecting. Just a few ways to think about the transaction. We can also look at actual strike prices and look at a few other values.

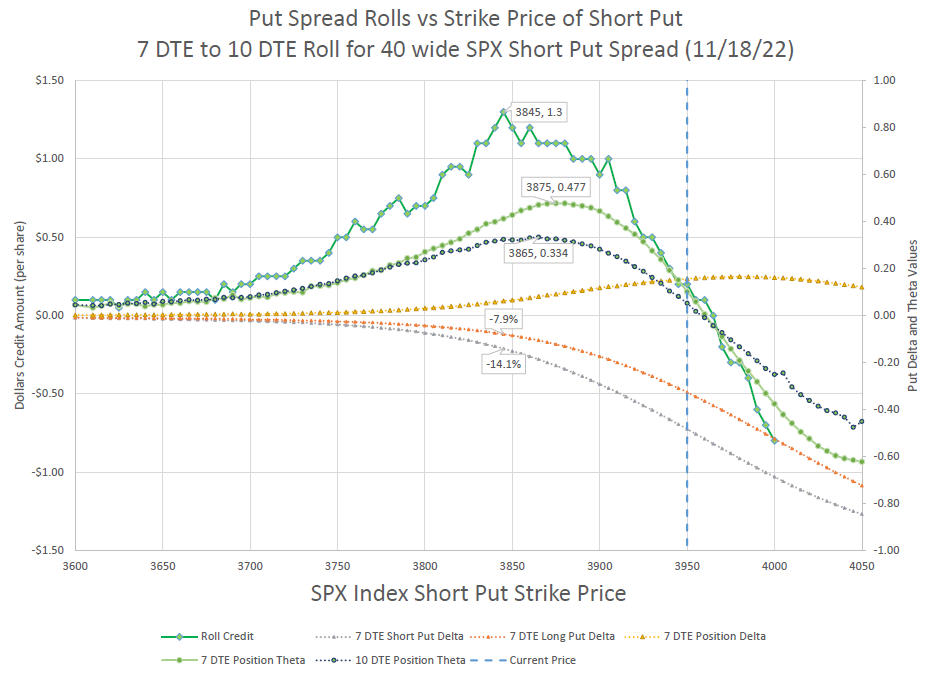

On this next chart, I’ve shown the x-axis as the strike price of the short put of the credit put spread. I’ve also added the Delta values of each of the puts for the 7 DTE spread as well as the Delta of spread position. In addition to the net Theta of the 7 DTE spread, I added the net Theta of the 10 DTE spread that we would roll to. So, each strike price on the x-axis is tied to six different pieces of data for a potential spread roll. While the roll premium and net Theta of the 7 DTE spread is the same information as the previous graph, the additional data can add more context.

Note that the Theta values of the longer duration spreads are generally lower than shorter. That should be expected. More time means slower decay. But the new spread will have a slightly higher Delta, which moves the peak of the Theta curve down in strike prices, because as we have seen in our study on maximizing Theta for a put spread, Theta tends to max out at short Deltas around 20, which will be further down after a roll. So, note from the chart that the maximum roll premium lines up for the most part with the maximum Theta of the spread we are rolling to.

The take-away from the Delta information on the chart is that as we get closer to the current price and have higher Deltas, the net Delta goes up, and the value of rolls goes down. Also, if Delta gets too low, there isn’t as much premium available in a roll to the same strike prices. I picked out the Delta values of the spread with the highest roll value, and it is approximately 14 Delta on the short strike and 8 Delta on the long strike.

So, the ideal scenario is to start with Deltas of around 20/13 and see the positions decay and Deltas to decline to 14/8, and then roll out to new strikes with Deltas of 20/13. If only the market would cooperate with our plan and let us do this all the time. Obviously, the market isn’t that consistent, so we have to manage in other ways.

Sometimes, we may want to roll down and out. Let’s look at the premium for 40 wide spreads and see what is possible if we want to collect a credit.

On the above chart, I have plotted the premium value of 40 wide put spreads at 7 and 10 DTE, along with the premium collected to roll out to the same strikes. I’ve also highlighted possible rolls down and out. The highest strike where it is possible to roll down a strike and collect a credit is to go from 3920/3880 at 7 DTE to 3915/3875 for a 10 cent credit. When a spread is being tested, every bit helps, but clearly this roll doesn’t give the position much more breathing room. On the other hand, if we had the 3800/3760 spread, we could roll down 25 points to 3775/3735 for no cost. So, again it pays to stay away from being tested. But at this short of timeframe, it doesn’t take much of a move to get a spread in trouble, so let’s look at how a little longer duration would fare.

21-42 DTE

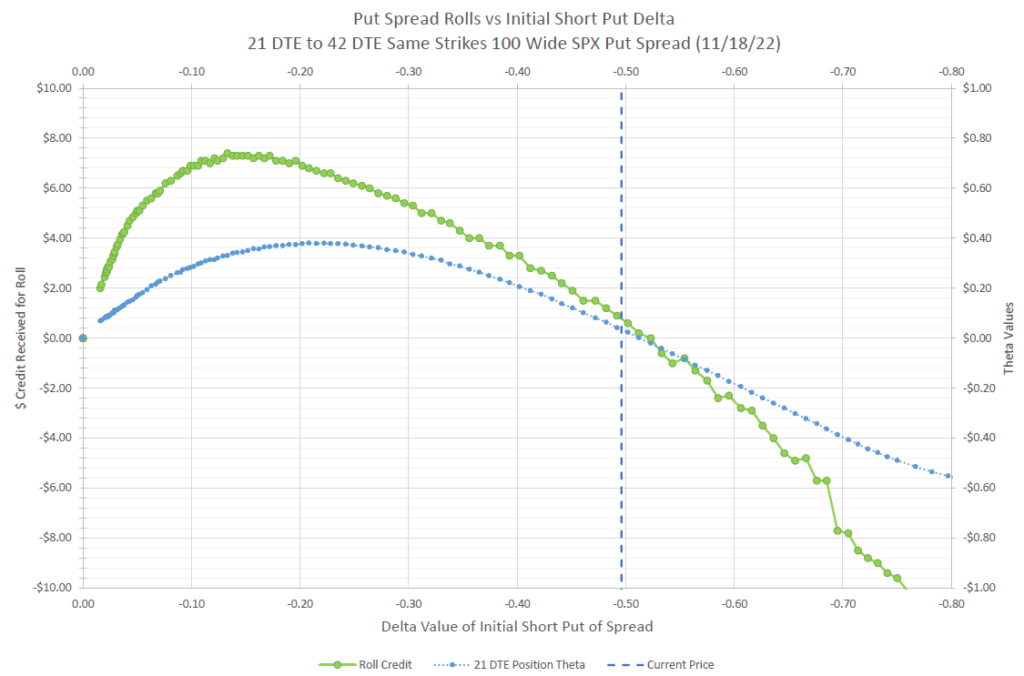

Let’s look at an example that generally matches up with the common strategy often associated with TastyLive.com. Interestingly, values peak out at about the same place based on Delta.

Again, the best premium for a roll is in the mid to low teen values of the Delta value of the short strike of the 21 DTE spread. Here we are collecting just over $6.00 to roll our 100-wide put spread out to 42 DTE. In that case, we would be collecting an additional 6% of the width of the spread. The 21 DTE spread would be decaying about $0.30 per day, so the roll allows us to collect around 21 days of decay in cash.

Notice that the observations we made on the 7-10 DTE roll hold almost exactly the same on the 21-42 DTE roll, even though we have much higher time to expiration, wider spreads, and proportionally longer rolls. One difference to note is that amount of premium and Theta are much less on a daily basis, but that should be expected as daily decay for similar Deltas gets higher as expiration approaches.

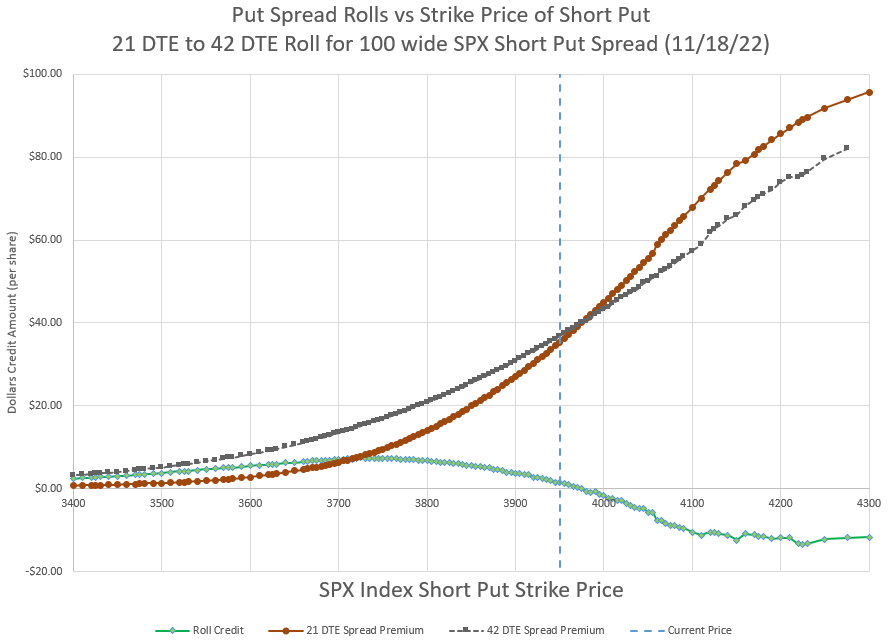

Another key difference is the distance that our strikes can be from the current price, giving the position more wiggle room for price changes. The above chart shows the premium of the various spreads available at 21 and 42 DTE. Notice that the lower strikes approach zero value while the spreads at higher strikes approach 100, which is the width of the spread and would be maximum loss for a credit spread at expiration. With spreads, the closer expiration gets the more of an S-shape we get when charting the premium. Since we are selling the spread, we’d like to see the value decay, either by staying out of the money as time goes by, or seeing the price go up, which would shift all the lines to the right on the chart.

What if we want to roll down to lower strikes when rolling out from 21 to 42 days? Let’s look at what would be available by zooming in a bit to the chart above to the area where there is credit available to roll out.

With plenty of time to expiration, we can roll out for nice credit or roll down quite a ways for some credit. For example, in the chart above, the 3700/3600 spread could be rolled down 150 points to 3550/3450 for 20 cents credit or rolled to the same strikes for $7.50 credit. The closer our strikes are to the money, the less credit we get to roll and the less we can roll down for a credit. And as we’ve seen, if our strikes are in the money, we would have to pay a debit to roll out. Having more time allows us to sell spreads that are much further away from the money and be able to roll out and away much easier than spreads that are closer to expiration.

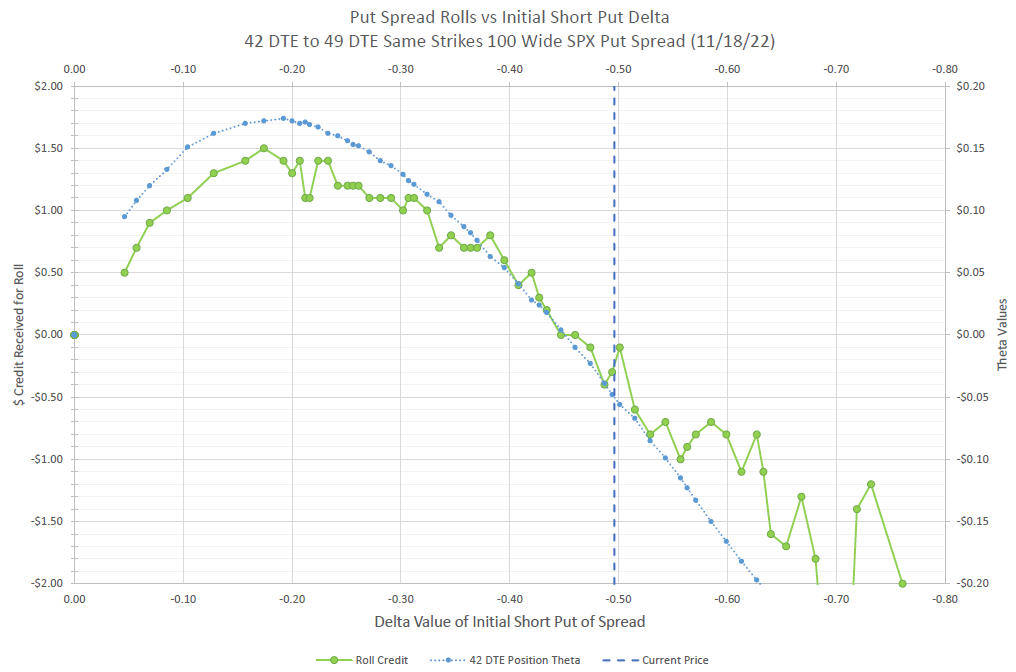

42-49 DTE

One last example for contrast, we will roll out a relatively short amount of time from a 42 DTE put spread.

So, this roll is from 6 weeks to 7 weeks until duration. However, our previous observations generally hold. The peak premium is at a bit higher Delta, in the high teens. This makes sense if we consider that we are only rolling out for about 16% more time, so our new spreads will have peak Theta much closer to our old spreads. This would point to the idea that the best roll is the roll that gets us to a new spread with a short strike Delta of around 20.

Again, our max roll amount equates roughly to the daily Theta multiplied by the number of days we are rolling out.

How to Use This Information

Readers may wonder, what good is this? A trader can’t really control where prices move to, so the Delta value is not really controllable by a trader. This is somewhat true, but prices do move up and down all the time, and so if I’m looking to roll out to get to a timeframe that has less volatility, I might be able to enter a limit order that seeks to collect close to the maximum roll credit possible. Often, I’m not in a big hurry to roll, so I can check out where the maximum should be and set up an order for 90% of that amount and go about my business. If it doesn’t execute after a day or maybe even a week depending on the timeframe of the position, I could change the order to something less lucrative.

Another way to look at this data is to realize that if my position has both strikes down in the single digits of Delta, I’ll likely want to roll up my strikes when I roll out to get to optimal Theta. On the other hand, if my position has strikes with Deltas in the twenties or thirties, I may want to try to roll down and out, and hopefully still collect a credit.

If my position has gotten even closer to the money or even into the money, I’m going to have trouble rolling for a credit, and I have some tough decisions to make. I need to consider all my choices: holding, folding, or rolling. If I’m deep in the money I might consider taking desperate measures. It all comes down to risk appetite and an overall plan of action. It’s best to have a plan for all possibilities ahead of time, and not try to figure it out when times get tough.

Final Take-aways on rolling put spreads

My thought process for looking into this was to find optimal credits for rolling spreads, so I could devise strategies to improve my results. After studying this, I was excited to find an answer that makes sense. Deltas in the teens for the short strike of the spread are ideal for rolling. The further out in time the roll is as a ratio of current DTE to future DTE, the lower the delta of the current spread for best credit from the roll.

A good starting point for estimating the best credit is to take current Theta of the spread and multiply by the number of days that are being rolled out. So, if Theta is 20 cents and the roll is going out 5 days beyond the existing spread, the best credit will be around $1.00.

Finally, realize that this study was for put spreads, not call spreads, iron condors, or naked options. Spreads have unique characteristics compared to naked positions, and their behavior does not translate over. So, I only apply this information to rolling put spreads.

I am studying how naked puts best roll as well and plan to do a write up in the future on the topic.

Hi Allen,

Thanks for the detailed research. It is hard to find such stuff now a days.

I have been trading PUT spreads om resistance and support for 25-35 DTE but never realized that .20 delta provides the best results if the market behaves normally. I always think there will be a down turn and so sell on support and buy 50-100 spread.

What is your most successful traded DTEs 7-10 or 21-42 ? I guess you always choose .20 delta.

Do you roll 10-15 days or wait for target premium to be received ?

Regards’

Arrora

Rakesh- Thanks for the kind words. There is a trade-off as you go to shorter durations. There is faster decay at shorter durations, so more potential quick profit, but the returns are much more volatile, meaning that positions are harder to defend when the market goes against the trade. Because of this, I tend to like the 42-21 DTE window more. I like to roll continuously within the window every week or two. It works well with my current trading schedule of less frequent trading, where I’m not watching the market constantly.

Thanks Allan for quick reply. I have the same opinion of 30d+ to manage the risks. I have 2 questions –

1. Do you still use .20 delta for 21-42 DTE PUT credit spread?

2. I guess we will be in bear market for a while and so PUT credit spread won’t work. Do you sell SPX bear CALL credit spread when market goes down ? You said return is very low for bear CALL spread.

OR

Probably buying 30d+ ITM Bear PUT debit spread is better in this case instead of selling .20 delta PUT bull spread? What do you say ?

I guess market will be volatile and down in next few months and selling PUT credit spread is risky and so I am thinking buying bear PUT debit spread when VIX30.

Regards’

RA

When I trade the the 21-42 DTE put spread, I try to stick to 20-13 Deltas. If I roll, I try to roll for credit and if my spread gets in the money, I will pay a debit to get out of the money generally. I often then pair the put spread with either a call spread, or a delta neutral back ration call spread.

I agree that selling put spreads when VIX is high has a lot of advantages, you get more premium and can sell strikes much further from the current price.

Hi. I stumbled across your site several months ago. The article “Roll for 6% per Week” has been a game changer for me. I roll every day to keep the 7DTE and always for a credit. I have been caught only once, April 7th 2025, and sometimes that happens. But the loss was made up in two months. LSS, it has been a very profitable strategy for me.

In a paper account, I also trade NDX, RUT & SPX for practice with excellent results.

Just wanted to thank you for publishing the paper. I also like the other information on your site. Very helpful.

Regards,

Dave

Hello, thank you very much for sharing this content, I have gained a lot from your website, I would like to ask if I choose the 45dte put spread and a delta neutral back ration call spread as a combination, do I also choose the delta neutral back ration call spread spread of 45dte? In addition, the theta of this combination looks negative, how should this be solved? When rolling the put spread, do I need to roll the delta neutral back ratio call spread together with it?

When pairing a put spread with a back ratio call spread, one goal I typically have is to make double use of the capital required. By choosing the same expiration for the two positions, the capital required is the width of the wider spread. As long as the spreads don’t overlap, the trade can’t lose on both sides, so the capital requirement and risk is shared by the two positions.

So, I prefer to have the two trades at the same expiration to open, and in the case of a roll, to roll both positions to the same new expiration.

You are correct that the Theta can be negative. The put spread will have a positive Theta, and the BRCS will have negative Theta. The negative Theta comes from buying two long options against the single short call. The Theta values of the calls and puts somewhat cancel each other out, and it depends somewhat on the strikes chosen on each side as to how much Theta is negative. As discussed in the writeup of the Back Ratio Call Spread, the trade loses money if the market stays in the same place and settles between the strikes, but can also make money if the market moves down letting the strikes move toward being worthless. The worst losses happen when holding until near expiration with price between the call strikes.