One of the most popular option strategies is selling covered calls. Another common strategy is to sell a bearish/credit call spread. If we combine the two, we can sell a covered call spread, collecting premium against stock, but not giving up all of our upside potential, and gaining some downside buffer.

Selling a covered call spread takes on one key downside to both credit call spreads and covered calls- upside risk. A regular covered call caps gains to the upside, while selling a credit call spread can lose a lot of money when the market goes up. It can be frustrating to have a position that was supposed to make money end up losing while the market is going up. To be fair, a regular covered call doesn’t lose money on an up move, because the gain in the stock offsets any loss from selling a call. However, compared to just having stock alone, the covered call can sometimes feel like a losing proposition. Let’s start by looking at each of these trades and then see how the combination gives us a different alternative.

Covered Call Issues

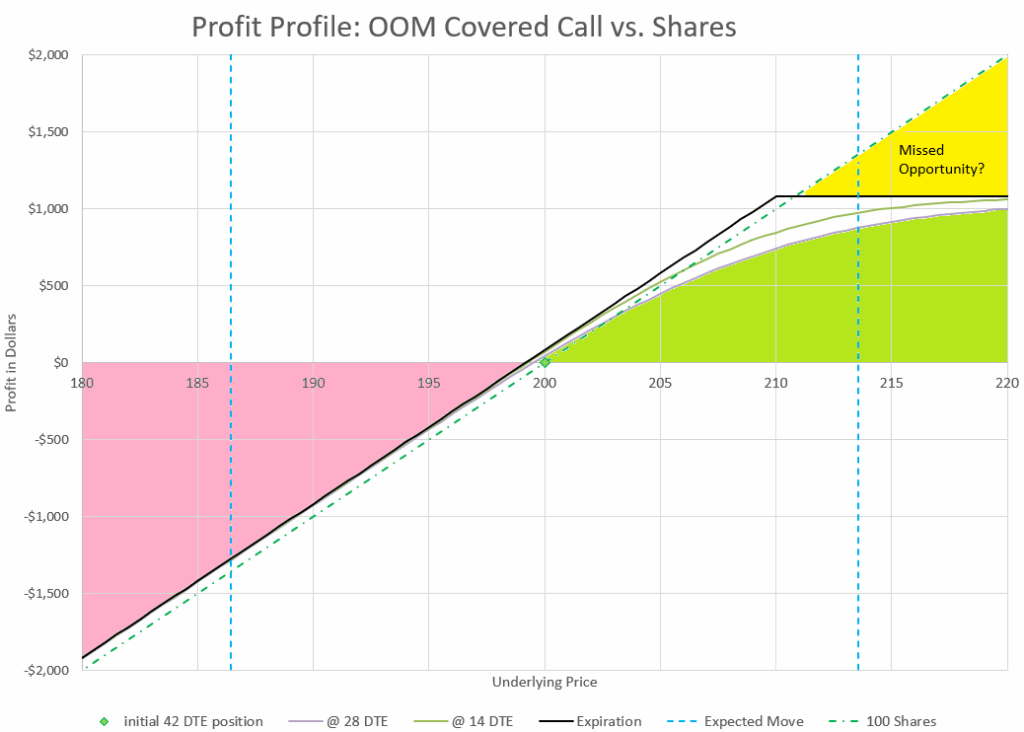

While the covered call provides many benefits, I’m often left with the sense that I’ve left money on the table when the underlying stock goes up significantly.

It has happened to me enough times that I’ve really found it irritating, even though by the time the stock is in the range where the call is in the money, I’ve made a tidy profit. The covered call is still a bullish trade and make money when the stock goes up. I just find myself thinking about what might have been.

Credit Call Spread Issues

I find credit call spreads even more troubling. Often meant to neutralize a credit put spread, more often than not, it seems like they end up losing money. Most back tests I’ve done bear this out, there just isn’t enough premium for the upside risk.

If you hold long enough, and the move up isn’t that big, you’ll make money, but even with a greater than 50% win rate, one big loss can wipe a bunch of smaller gains. The credit call spread is actually a bearish trade with negative Delta, so we shouldn’t be surprised that it loses money when the market goes up. One key point to remember is that the spread does define risk, so there is only so much that we can lose.

How a Covered Call Spread Can Help

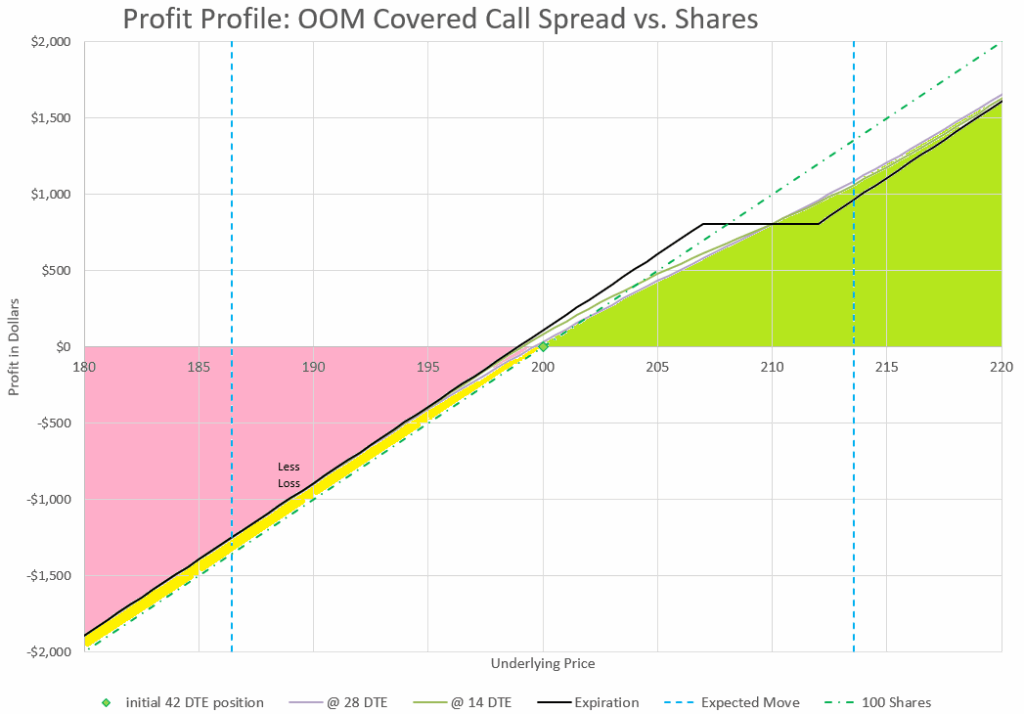

By pairing stock with a call spread, we can turn a bearish spread into a source of income with positive Theta, and a bullish overall position with positive Delta. We also get a bit of downside protection without giving up the ability to keep profiting when the market really breaks out to the upside.

At first glance, the profit curve for a covered call spread isn’t that different from stock alone, other than a little lower losses and a little lower profits. In fact, it does reduce volatility of returns compared to stock alone, like a covered call does. It also makes more money than stock alone at prices where the stock doesn’t move much.

The advantage compared to a regular covered call is that you don’t have to give up all the upside to get benefits at small moves up or when the stock goes down. The long call of the spread limits how much the short call can limit upward profits. The long call and the stock provide two positive Delta elements to the one negative Delta element of the short call. At the extreme, position Delta can approach 100 on the upside, compared to a Delta of zero for similar prices with a regular covered call. The disadvantage is that you pay for that remaining upside with less of an improvement at the money.

The Setup of a Covered Call Spread

Basically, the setup of a covered call spread is just a combination of a call spread and stock. Because we have stock to “cover” the spread, we can be a bit more aggressive with our Delta values than we would be with a credit call spread by itself, or perhaps even with a single short call in a covered call position.

The worst that can happen to the spread portion is that it ends up in the money, while the stock makes more than the spread loses. But the worst that can happen to the full covered call spread is that the stock can lose a lot of money in a downturn and the call spread can only contribute its premium to slightly reduce the loss.

I don’t have any magic Delta value for this trade- I just look at it as an opportunity to be aggressive with the short call of the spread and use the long call as a protective hedge. There isn’t a big penalty for the spread getting in the money, so collecting more premium with higher Delta can be beneficial.

Let your imagination run wild with this- our short call is essentially double covered. First, we have stock to ensure that the short call never can lose more than the stock can make, and then we have a long call to hedge the “loss” that the short can generate if considered separately. Both a covered call and credit spread protect a trader from the unlimited loss potential of selling a naked call. The covered call spread is double protection.

But is double protection worth it? You have to pay for the long call of the covered call spread, and no one forces you to add it. Your brokerage won’t even give you extra buying power for the addition and probably will show it as an extra call. Only you will recognize it as part of a covered call spread, a term that arguably isn’t even a real thing. But for a small price, you can still have essentially unlimited upside while making a bit more income, reducing volatility, and having a bit of downside protection. Only each individual trader can decide if it is worth it.

Managing the Covered Call Spread

When it comes to managing a covered call spread, it really works similar to a standard covered call. You have the standard methods of hold, fold, or roll like any other option trade. But there are a few nuances to consider.

In most cases a trader with this covered call spread will want to hold onto their stock, but manage the call spread. If a roll is warranted, rolling a spread can be a little more challenging than rolling a single short option. However, since the long call has no impact on buying power, we can change the width of the spread on a roll without requiring more capital, so we have more flexibility than we normally would with adjustments to a credit call spread. The stock is covering the short call, and the long call is just tagging along.

I typically like to manage the short call of a covered call spread similar to the way I would with a regular covered call. If the situation suggests rolling up, I’d roll up, and if I need to roll down, I roll down. When the spread is out of the money, the spread can be rolled to similar strikes for a credit at the same width.

When the short call gets into the money, it may make sense to widen the spread when rolling to keep collecting credit, looking for combinations to get later expirations that have more credit on the short call and less cost on the long call.

How long to hold the Covered Call Spread?

Because the covered call spread has a bit of a strange profit curve, it makes sense to have a little different plan for when to adjust or close the spread.

In the above diagram, I’ve highlighted the profit zones a bit differently to illustrate the difference between the best holding periods for different underlying prices. Let’s consider three different underlying price zones- lower prices, slightly higher prices, and much higher prices. One thing that is true for all zones is that the underlying price of the stock determines most of the gain or loss of the position. The call spread that has been added only “tweaks’ those results, but our goal is that those little tweaks add up to a nice positive benefit over time.

When prices go lower, the stock loses more value than the call option spread can gain except when the price decrease is very small. If you look at the profit curves for different time frames, after the price has dropped several dollars from its opening value all the curves- short duration to expiration- all converge. At this point, the call options have been zeroed or nearly zeroed out, so we can either close the spread, or roll to a new spread to collect some more premium to reduce losses. The call spread has contributed all it can, so we need to take it off one way or another. The only exception is that small section near our starting price where we need to wait for decay to occur.

When the price moves up slightly, but less than half-way through the spread, the spread will keep contributing profit due to decay. This is also true for the slight down move section where short duration moves are less than the expiration move. In this area of the profit curve, our goal is to hold onto the spread longer until we get close to expiration or the price moves to the point where we are equal to the expiration value. The only watchout is that if we get to the price where the short option is in the money, we can have the risk of assignment, especially if a dividend is approaching. So, as the short option gets into the money and we are short on time with the risk of assignment, it is good time to roll out in time to reduce assignment risk and find a way to collect more premium. If we are out of the money, we can hold the spread all the way to expiration or very close, and then roll out for more premium.

When we have a big move in price beyond the mid-point of the spread’s strikes, our profit curve is now above the expiration curve, so option Theta decay will be working against the position. We will see Theta turn negative for the combined options. At this point, it is a good time to roll our spread to a new set of options and get our Theta values positive and making money.

Another way to think about this is to focus our decision based on total position Theta value. In general, our goal is to get as much Theta decay out of the spread as we can without having our stock called away. You may want to consider monitoring Theta and making an adjustment when it falls below a value of perhaps half the starting value. For example, in our above example, we started with a Theta value of $1.86 per day. Theoretically, this should go up every day as we eat away at the $107 in premium that was initially collected to decay over 42 days. But, when our underlying price moves up or down our Theta will also change, either because there is little premium left to decay, or our spread has gone into the money and is growing against us. Either way, if Theta isn’t helping any more, we should adjust to a position where it can help us. If Theta is much less than where we started, we are close to switching over to negative, so it’s probably a good time to go ahead and adjust.

In the end, if we can keep our Theta positive and keep rolling our spreads out in time, collecting additional premium with each roll, our total profit from the covered call spread should beat the profit of holding stock alone. The exception would be when a stock just goes up non-stop and the rolls continue to be to the upside, increasingly harder to roll up for a credit as the spreads work against us. But that should be the exception.

Expectations for Covered Call Spreads

Let’s be clear, traders won’t get outsized returns from selling covered call spreads. The goal is to make a little extra income and reduce volatility a little. Depending on the width and duration of the spread, a profit goal of 3-10% above the return of the stock alone is about the best one can hope for. Still, I know a lot of people who would be very excited to make 3-10% returns.

Some would argue that a trader would be better off just doing a covered call and skipping the spread because the cost of the extra long call is just not worth it. But, the spread’s addition allows big moves up to still be very profitable overall and takes away the fear of capping gains.

Others would argue that a trader would be better off with just stock alone and getting a positive gain from an option sale isn’t a high enough probability. I used to feel that way. However, one thing I like about any version of covered call strategy is that it reduces the volatility of my returns up or down on a day to day basis, and there is value in that.

Finally, if you like this concept, consider applying it to the poor man’s covered call. How about a poor man’s covered call spread? Lower your capital use overall and keep your Theta positive while being bullish with long calls. A discussion for another time, but not that different overall.

Conclusion

For traders that like the idea of a covered call, but don’t like having their profits capped by selling a call against shares, selling a covered call spread provides an alternative to still collect call premium without giving up all upside potential.