What happens if we try to optimize both a diagonal put spread and a diagonal call spread, and roll every position every day? We end up with a very high risk, high reward trade. But how much risk, how much reward? Are there ways to manage the risk enough to keep the reward? I’ll let you decide for yourself.

In a calm marketplace, this trade can often make 5-10% return on capital in a day. That’s right, in a day! For example, using SPX index options, a single double diagonal contract with a risk of approximately $10,000 will often make between $500 and $1000 profit from one day to the next. However, a bad day could mean a $3000-$4000 loss on that same capital. So, as trading volatility goes, like the guitar in the classic mockumentary movie “This is Spinal Tap,” on a scale of 1-10, this one goes to 11!

The idea is to make money off Theta decay of options sold with very short duration, while covering their risk with longer duration options that decay slower. And by using both calls and puts, the trade is less directional. This works great when the market moves small amounts day to day and decay/Theta is the main driver of option premium profit and loss. But on days with bigger price moves, Gamma kicks in and pushes the Delta values of one of short options up faster than the long option hedging it, and losses can get big as one of the short positions loses money much faster than the long position hedging it can gain.

I’ve hesitated to write about this trade because the risk is so high, even though the risk doesn’t seem to be that great at first glance and is deceptive. I’ve been trading this for a while, and my best month was 150% gain, but my worst month was a 140% loss. (You would think that after losing 100%, that would be enough, but I kept replacing lost capital.) April 2025 was the really bad month- you may recall that President Trump threatened to put up to 200% tariffs on China and 90% tariffs on most of the rest of the world, driving the market down 20% in a few weeks, and then reversing course and suddenly delaying implementation and severity of tariffs, which drove the market up over 10% in less than a day, the biggest one day move up ever. This trade lost big money both ways, and I vowed to adjust my mechanics to avoid that big of a loss in the future.

Over time, I’ve put together mechanics for normal days, plus mechanics to use for crazy days and normal adjustments to make and exceptions to normal adjustments. I’ve identified triggers to change strategy, or maybe even to get out, with a few different variations to pick from. I’ve tested different variations in back tests and in real trades, looking for the best approach.

Let’s back up and talk about what the setup of the double diagonal trade is along with basic management on a daily basis. My goal with this trade was to be able to make money from premium decay by selling short-dated options, and find the best longer dated options to hedge against big moves. In many ways this trade is related to the Very Long and Very Short Put Spread trade I’ve written about, as well as the Daily Diagonal Covered Put Spread trade, and Backtests for Rolling Diagonal Put Spread studies. All of those trades used only puts for diagonal trades, mostly with much longer duration on the long puts. My studies and experience pushed me to use 2 DTE short strikes and 10-12 DTE long strikes. I read about the experiences of many traders using double calendar strategies in generally longer duration trades, and decided that adding calls was the next logical addition to test and try.

Daily Double Diagonal Basics

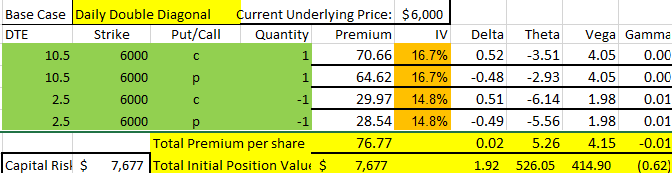

A double diagonal is four option positions, potentially with up to four different strike prices and up to four different durations. At it’s simplest, it can be an at-the-money double calendar with the same strike price for every option at two different durations. For example, if SPX is trading at 6000, we could sell a put and a call at 2DTE with a strike price of 6000, and buy a put and a call at 10 DTE each at a strike price of 6000. A simple adjustment would be to move all the strikes each day to the closest strike to the current price. This can be our base case strategy because it is easiest to comprehend. But, we can compare more diverse combinations to this as we go along.

To be clear, our short/sold options will be sold with two trading days until expiration, so on Friday, we would sell a Tuesday expiration because the market is closed on Sunday, and while Monday is 3DTE, it is only one trading day away. The long strikes are more like 8 trading days or 10-12 calendar days because sometimes 10 days hits on a weekend and we need to add a couple of days to stay consistent. That’s the assumption I’m working on for this base case.

The setup above and the profit chart show that with all strikes at the money, our optimal profit for a day for the market not to move. Notice that I’ve picked durations of half days, as I tend to open and close this trade early to mid-day. When the market moves more than the one day expected move, the trade loses money. Also notice that Theta is over $500 a day while using just over $7000 capital, which is the main reason why the trade has the potential to make 5-10% return in a day.

One key concept of the Daily Double Diagonal trade was to make the trade easily adjustable, no matter what the market does. I thought I could reset all the strikes every day for very little premium cost. This tends to work as rolling a losing strike for a debit is countered by rolling a winning strike for a credit. Each day the net debit or credit to roll is approximately what the profit or loss was from the day before.

Most days, two of the options are profitable and two lose money. The goal is for the winners to make more money than the losers lose. On a calm day, both shorts might make money while the longs both lose money- this is ideal. On up days, the short put and the long call make money, but the long put and short call lose money. On down days, the short call and long put make money while the long call and short put lose. Each day, different options have their day in the sun.

Most of the time, prices stay inside the expected move and we can make a profit. When moves are bigger than the expected move, they tend to not go that far beyond the expected move, so on average, we can make a nice profit. But, one bad day can really hurt. Typically, some sort of bad news or announcement moves the market down a few percentage points and the short put loses a lot. Then, if the trade is recentered back to all at the money strikes, there is often a snap back rally at some point that causes a big loss on the short call, often a loss going down and going up.

So, can we do anything to make our two winners average more than our two losers? Let’s consider some adjustments to the basic ATM calendar version of daily diagonal.

- Move the whole trade out in time to reduce daily volatility.

- Make intra-day adjustments to short strikes to make sure there is plenty of premium and that Delta of the losing side doesn’t get too high.

- Avoid over adjustment, particularly rolling short puts down to avoid being whip-sawed.

- Only trade double diagonals when volatility is low. Get out or skew to more long options when volatility is high. Consider back ratios or other exotic variations when the market is turbulent.

- Go further out in time for strikes that you want to have less influence.

- Add Delta to options that are more likely to profit, and reduce Delta for those more likely to lose.

- Consider adding positive position Delta when the market is on the move up, the most common scenario, or market regime.

- Change strategy setup for high volatility regimes vs low volatility regimes.

- Move longs out of the money for less premium costs and less Delta impact.

- Treat the longs as a profit generator.

- Keep this trade a small percentage of a portfolio, and water down with cash.

Some of these strategy adjustments conflict with each other, so a trader would need to pick and choose based on their general approach to trading and risk management. Some of these also are hard to back-test because of changing mechanics based on what happens in the market, and most back-tests are for doing the exact same thing every time. But let’s discuss each one and see if we can develop some elements that might be cobbled together to improve results.

Go Further Out In Time (1)

One way to make this Daily Double Diagonal Trade less volatile on a daily basis is to pick longer strikes than what I’ve chosen above. To a degree, I originally chose 2DTE short options to optimize the highest level returns from this type of trade, but it also brings a huge amount of volatility. By using short options with a week or two of time until expiration and buying long options 2-4 times as long duration, day to day movement can be greatly reduced. 10% daily returns are probably out the window, but probably so are 20-30% losses in a day.

One downside to longer duration is that the capital costs will likely be a bit more. On the other hand, there may be more underlyings that could be used than index options.

Longer duration on the short strikes also means you won’t have to roll every day, and probably can skip the need to ever make an intra-day adjustment. For many traders, this might be the change that makes this trade tolerable.

After a lot of trading and back-testing, I’ve found 7 DTE for shorts to be a nice compromise. One factor that isn’t obvious is that Delta doesn’t change as much on moves (Gamma is much lower). This plays out with overall position Delta being more consistent for most daily moves. The only time I like to use shorter duration is when volatility is low and the market isn’t moving much, but that is part of another strategy adjustment.

Intra-day Adjustments (2)

When the market makes a big move during the day or even overnight, we see one of our short options start to lose money by increasing its short value dramatically, while the other short options approaches zero value, limiting its profit from the move. For example, in our base case double diagonal, both short options sold for approximately $29 premium. Let’s say the market moves up 75 points and now our short call is priced at $80 and now has a Delta value of over 80, meaning that it will keep going losing over 80 cents for every addtional dollar the market goes up. Meanwhile, our put has dropped to $8 in premium and has a Delta of less than 20 meaning it will only contribute under 20 cents back for every dollar the market goes up. We started with short premium of $58, and now we are at $88, a $30 loss. Meanwhile, our long options have only kicked in $15 because their Deltas don’t change much and we’ve gone from Delta neutral when we opened the trade to quite Delta negative for the overall position, based mainly on the short call being deep in the money.

We could wait and see what happens, or we could adjust our strikes back to close to new at-the-money strikes, so that if the trend continues, we are starting over at a Delta-neutral position and won’t lose a lot until there is additional big moves. If prices stay where they are or within an expected move of our new strikes, we’ll make back some of our money by the time we are ready for our regular roll.

The idea of adjusting is to cut our losses before the accelerate out of control and put the past in the past. We somewhat assume that the market move will stick, based on the efficient market theorem premise that the market is always fairly priced for the information that is currently available. Keep in mind that moving the two shorts back to center after a move does lock in the loss.

However, as any trader that has watched the market for any time knows, the market often over-reacts and then reverses coarse for almost no apparent reason. Making an adjustment back to at the money strikes is painful if the market turns around right after you adjust. Which brings us to our next adjustment consideration.

Avoid Over-Adjusting, Particularly Puts (3)

One of the things that makes this type of trade particularly risky is the short duration of the short options. With only a few days left until expiration, there isn’t time to let things play out like there is on a 45 DTE trade. But we also know that market swings up and down are pretty common. We know that big down moves often precede big up moves, but not necessarily. Variation is normal, but not really predictable. So, what can we do with that?

My take-away is that on a trade like this, we need to make adjustments but only incremental so that we don’t chase the market’s every move up and down. There are strategies that are good for chasing moves, but since our positions lock in losses when we make a big adjustment, it may make sense to make partial adjustments each time in case the market reverses. In that way, we can take some risk off without completely exposing the trade to a whipsaw of the market.

Most of the time, I’m more willing to adjust strikes up more aggressively than down. That’s because the market has a long term drift to the upside, and I really don’t like losing money when the market goes up- one of my biases that probably isn’t the most data driven consideration, but a bias nonetheless.

I tend to be skeptical of chasing moves down, as it seems like it is just a matter of time before the bad news that drove the market down is negated by something positive. As I write this, we’ve had a lot of experiences in 2025 that have caused the market to have big down moves, some lasting only hours, some for a few days, and some for weeks, but in each case we’ve come back to where we were before the bad news. Many of these moves have been driven by comments and actions by President Trump, both up and down. There’s also Federal Reserve commentary, and economic data. There’s a lot of sentiment to “buy the dip” and trust in a “Trump put” or “Fed put,” a belief that neither the president or the Federal Reserve will let the economy completely fall apart and will intervene when things look particularly bad. The most recent stark example was in April 2025 when threats of tariffs reached a level that threatened the global economy as trade started to halt all over the world. When things looked very bleak and the market was down around 20% from a recent high, President Trump announced that he was delaying implementation in a series of announcements that re-assured markets around the world and the market had its biggest one day up move ever. Adjusting this trade down mechanically at the low made for a painful loss going back up. That’s an extreme example, but one that is still very fresh to me.

I think about over adjustment of this trade both in short-term and long-term time frames. We’ll talk about short-term adjustments here and save the long-term strategy adjustments for a different point.

Short term, on a day to day basis, I can choose to adjust strikes in my rolls by only part of the move, particularly if a move is much bigger than normal and I’m worried that it could soon be subject to a reversal. Perhaps I’ll adjust my strikes half-way to where the ideal strikes I target are to give the trade a day to settle out. This is especially true for intra-day adjustments, where I’m trying to prevent a loss from running away. I also tend to treat my short call and short put a little differently when I adjust.

I’m hesitant to roll down my short put much at all, waiting at least one day at a previous high strike before rolling down and then rolling down in small increments each day following if needed. This is because rolling down is fighting against the long term upward drift of the market. Sooner or later the market will come back to my short put, so I can be patient. If it happens sooner, I’m really happy to have stayed patient. If it is later, it becomes easy to second guess as the paper losses pile up. On the other hand, I tend to aggressively roll up my short puts to make sure they always have plenty of premium.

For my short calls, I’ll roll down fairly aggressively to make sure I have plenty of premium, but I’m also aware that this goes against the upward trend bias, so I may error a bit to staying above the current price a little more than normal. When rolling up, I’m generally locking in a loss, so this may be a place to go halfway since I’m in the money anyway on an up move. But I’m not waiting long for the market to come back down after a big up move because up moves are part of the long term upward bias and I don’t want to fall too far behind the trend and let the Delta of the short call become significantly more negative than the long call Delta is positive.

The long calls and puts have less Gamma- their Deltas change less on bigger moves so I can use their adjustments to help keep my overall position Delta from getting extreme. So, I don’t have to make dramatic moves with the longs beyond what I do with the short positions. However, my longs make money in the direction the market goes, so having close to neutral Delta on longs optimizes profit opportunities for the longs with a move. This causes a contradiction that we’ll need to sort out.

Eventually, as I get a sense for where the market is settling, I’ll continue to adjust closer to my ideal Delta values, especially on the call side. I take my time rolling down puts that are in the money, but if the market stays down for a long period of time, eventually I have to move that way.

Change strategy for different market regimes (4)

Longer term, it might be appropriate to consider a more drastic change of strategy if the market moves to a period of extended and deep downturns. The short options of the double diagonal strategy tend to do well when volatility is average or below average. Over time a good measure of market volatility is the VIX volatility index. The long-term average, or mean, for the VIX index is around 18, and it stays below average more than it is above average because the spikes above average can go very high, pulling up the mean a lot. So a possible long term approach might be to only trade double diagonals when the VIX index is below average. So, what would there be to do when VIX is above average?

Over time the market transitions through different price environments or regimes moving from low VIX to high VIX and back down in response to market downturns and recoveries. In periods of above average VIX, we can take a couple of approaches. We can simply exit the trade and wait for the market to settle down, or we can look for trades that might do well with increased volatility but have similar mechanics to double diagonal.

One metric I noticed in my trade logs of the double diagonal is that in low volatility months (most of the time), my short options made more money than my long options. However, in high volatility periods, my long options outperformed my short options. The problem was that the long options didn’t make as much as the short options lost. So, what if we bought more options than we sold during volatile periods?

Having more long options with longer duration tends to boost the Vega values of our positions. Vega is the options Greek value tied to Implied Volatility. When Vega is positive, the position benefits from increasing Implied Volatility. So, we get the benefit of the price move, plus the benefit of premium increasing from the volatility component of options.

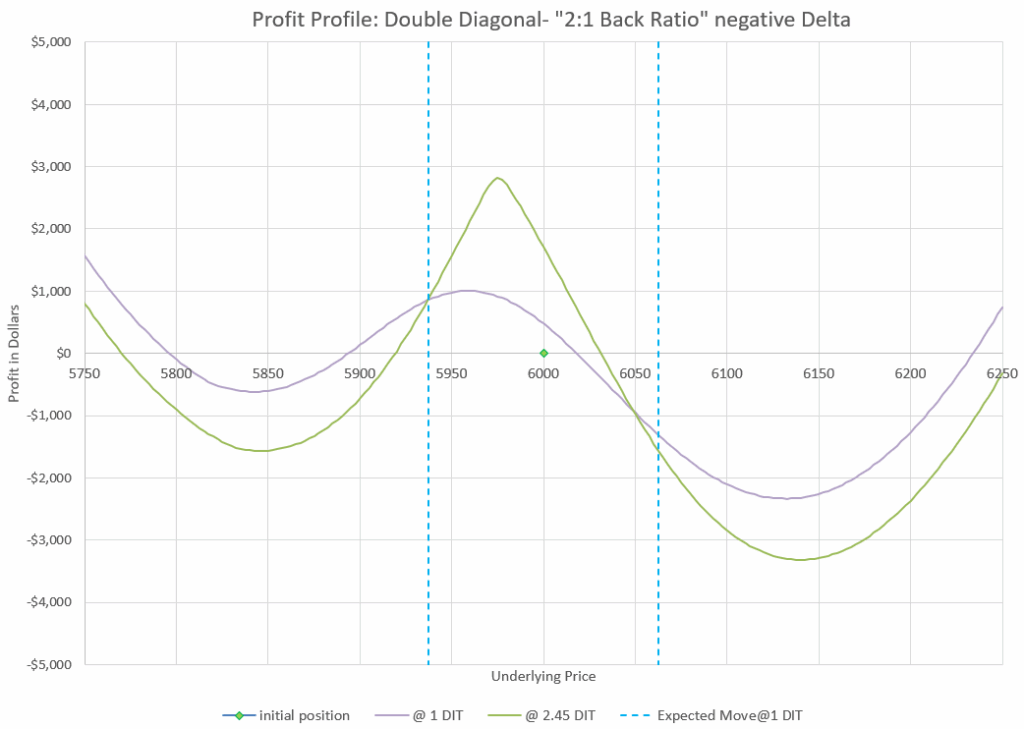

An adjustment to consider might be to buy two options for every option we sell when the market starts to become more volatile, essentially making the trade into a double back ratio diagonal spread. We can even balance Delta between calls and puts, keeping the position Delta neutral. Because we still have some short options, we have the opportunity to stay Theta positive, just not nearly as positive as in our double diagonal. So we can have a position that makes money from big moves, doesn’t have much time decay, and gains from increasing Implied Volatility. In fact, this set up does very well in a crashing market.

Here’s an example of what this type of trade might look like:

Setting up a back ratio for a double diagonal trade lets the trade make a big profit from very big moves. But moves that are between 1-3 times the daily expected move can still lose quite a bit with this set up as the short options go deep in the money faster than the two long options kick in. Since we still have positive Theta, a day with little price movement remains profitable.

We can even set up our strikes to skew our results to be more forgiving on the way down by adding some negative Delta:

By moving the short put out of the money, we can make it have less impact on the way down and make almost all down moves profitable. Overall, Delta is negative with this setup variation.

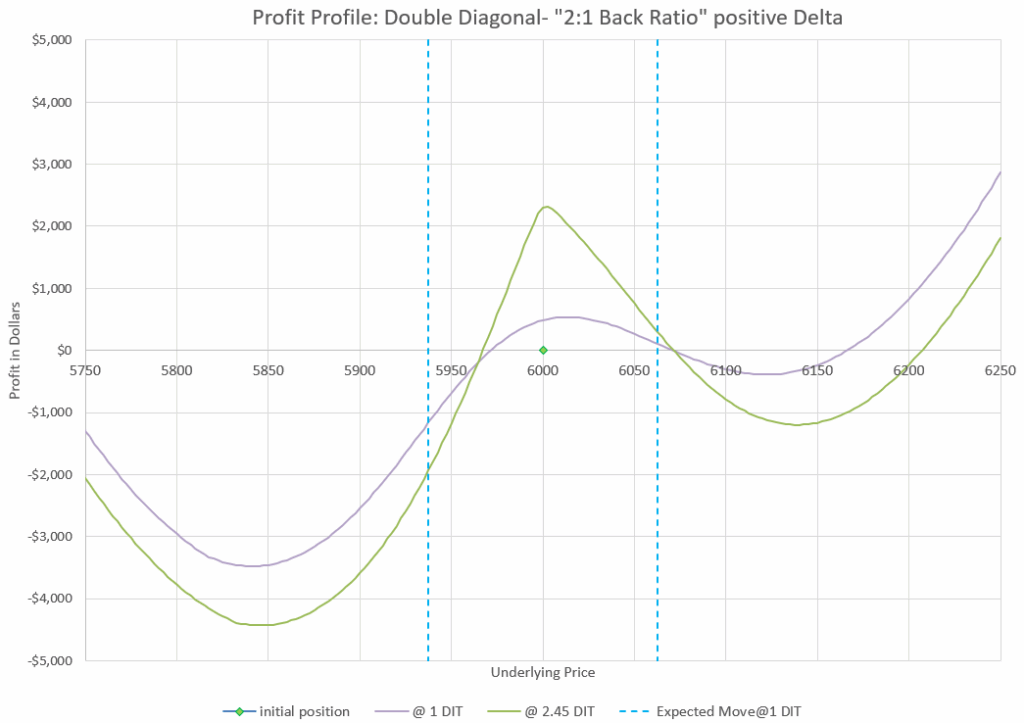

But what happens when the market turns around and starts going up and Implied Volatility starts going down? Usually there is some key turning point- an announcement that changes market sentiment. Typically, the initial move up out of a sharp downturn can be a sudden strong move. These moves are usually very hard to anticipate- often the market has started a big move up before traders realize the bottom is in. So it can be hard to switch to a double back ratio skewed with positive Delta in time to catch the initial rush up. But if you could, it might look something like this:

While hard to time, getting a positive Delta double diagonal back ratio spread can capture the up move. This setup variation has positive overall Delta value.

Another alternative would be to drop the call diagonal, especially the short call as the market gets severely negative, and just have a put back ratio with a long call. This setup has negative Theta, but if the market is really acting volatile, it is probably moving way more than the daily expected move each day so more longs each way give us more potential to win either way:

Simplifying to less short strikes makes a trade that benefits mostly from big moves, but doesn’t lose much if the market sits still, but we do have negative Theta.

One approach I’ve tried as it has evolved is to switch to a double diagonal back ratio when things start looking dicey and the market seems to be working toward a downturn. I give up a little income but have protection from a big loss on down moves. Once down moves are starting to seem never-ending, I switch to the put back ratio with a call so that I can make money either way the market goes and I stick with that version until we have recovered enough that Implied Volatility is either below average or has leveled off a level close to average VIX of 18. Once things are somewhat normal again, I can return to my favored version of Daily Double Diagonal again. Of course this assumes I don’t decide to pull the plug on the trade at some point.

The point of all these variations is to show that as the regime of the market changes, it can be beneficial to change approach to take advantage with appropriate adjustments to strategy. Every trader has a different tolerance for risk and loss. As explained before, this trade is about as risky as they come, so all of this adjustment may be too much for many traders for many reasons.

For the next three adjustments, we can apply them to any of the market environments or regimes, but I’ll focus in on the most common situation, below average VIX with a gradually increasing market.

Add More Time to Some Strikes (5)

One observation we’ve made in numerous examples is that the shorter the duration of an option is, the more volatile it becomes. On the other hand, longer duration options change value at slower rates the further out in time we go. So, for strikes that tend to be losers and are serving more as hedges, it makes sense to add time to those contracts.

There’s no real reason to keep our calls and puts at the same expiration with this trade because each short option is protected by the associated long, but not really from the opposing option type. The long call protects the short call, but it doesn’t protect the short put. So, the shorts can be different durations from each other and the longs can be different as well. We just have two diagonal trades that work somewhat in tandem to give us some sort of profit profile for different price moves and market sentiment changes.

If we know that during a typical up market, short calls and long puts tend to be losers, we can extend their duration a bit to make them have less influence on the total return of the four-legged double diagonal trade position. Maybe we add a day or two to the short call, and maybe add several days or a week to the long put. The trade still works in the same way, but the positions that tend to lose have less influence because they won’t change as much.

Of course, this means that when the market goes against the trade assumptions, losses will be bigger because those positions that were supposed to help in a downturn are now less potent. There’s pros and cons to every tweak you make, so understand how time adjustments will impact returns on a day to day basis.

Adjust Delta of Individual Strikes (6)

Initially we started with an example with all strikes at-the-money (ATM) at the exact same strikes. However, you may have noticed that some of the long-term variations of different strategies used different Delta values for different legs of the trades. Similarly, we can increase and decrease Delta to make certain legs have more or less influence on results. As we adjust individual legs, we also adjust the total Delta of the overall trade position, so we may want to consider whether we want to final version of the trade to be positive, negative, or neutral and adjust accordingly.

In reviewing my trade logs, I noticed that most months the legs with gains were the short put and the long call. This makes sense because most of the time the market is going up. So with an increased Delta of these strikes I should get a better return when the market is increasing. However, if I increase Delta of these strikes, I will make the whole trade more positive Delta, which will also make the position more volatile, winning more when the market is up and losing more when the market is down. So, this can only go so far until the trade becomes even more of a roller coaster ride. Maybe we can combine this idea with adjusting duration.

If we combine Delta adjustments with the time adjustments from the previous point, we can be more flexible to define combinations that work together to respond positively to the market changes that are most likely and still not be that far from neutral most of the time.

Add positive position Delta when the market is on the move up (7)

To build on the last idea, the most common market regime is an up market. Over history, the market tends to be in an uptrend around 80% of the time. This is due to the fact that the market represents growing companies that increase in value over time, so the average return of the market over time is positive. Also, when the market goes down significantly, it typically moves down quickly, so the down moves are shorter, but more pronounced than up moves generally.

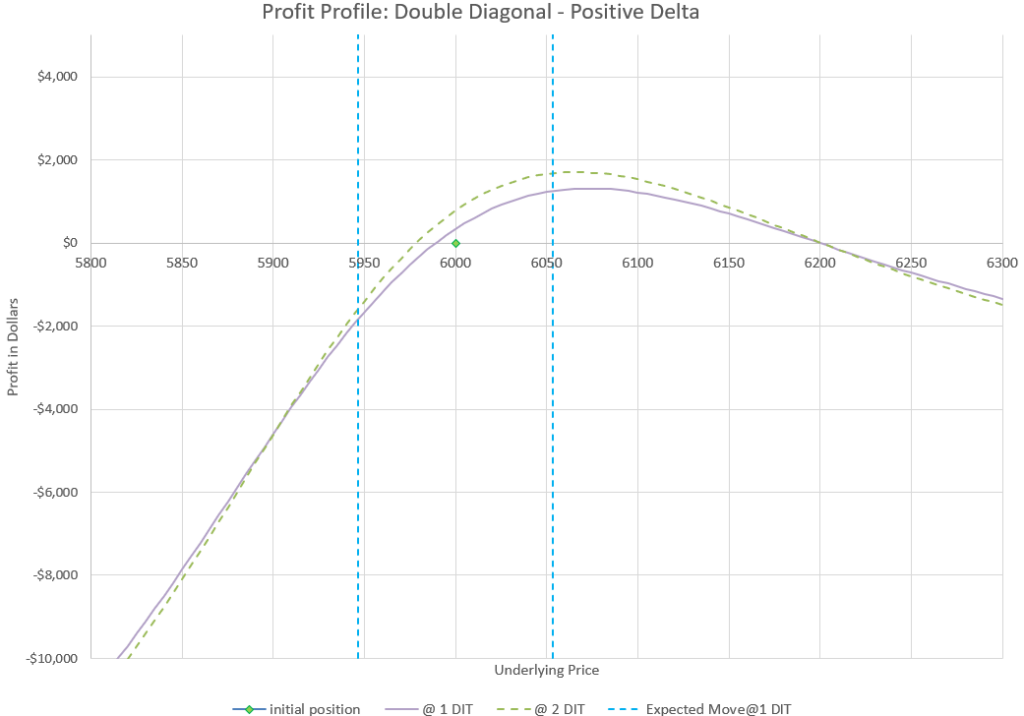

So, most of the time it would be good to set up this trade to have positive Delta built in. One of the strongest back test results I’ve come up with has the long call and short put essentially at-the-money, and the long put and short call out of the money. In up markets, the long call in this trade makes more money than any of the other positions over time.

Here’s an example of this kind of setup:

Note that this trade does well when the market goes up, but not when it goes down. For long bullish runs, this set up will do really well, but in bearish environments, a different setup is required, or big losses will occur quickly.

Change strategy setup for high vs low volatility regimes (8)

I’ve mentioned earlier that diagonals and double diagonals do well when the market doesn’t move much. And they can lose a lot when the market moves a large amount, generally beyond the expected move on a regular basis. This tends to happen when VIX, the volatility index is high. In all the back tests I’ve done on the double diagonal, the big drawdowns occur when VIX is high.

So, maybe we should trade differently when VIX crosses a threshold to avoid big losses? The simplest strategy would be to just stop trading when VIX crosses a threshold like 20 or 25. Or we could drop some or all of the short options and just trade a long strangle or double back ratio while VIX is high. Ideally, we’d pick one of these strategies that benefit from big moves and skew our strikes to have negative Delta on the way down, and switch to positive Delta when the market hits bottom. The challenge is that usually there isn’t any warning of when the market turns around. Often, when things look very bleak, there is some sort of policy change by the Federal Reserve, the President, or some other authority that re-assures the market and it quickly jumps from the bottom. In hindsight, it is obvious that this was the turning point, but in the moment, it might not be so clear. So, I try to not let my position Delta drift too far negative or positive to avoid a big loss from a reversal.

While it is hard to know ahead of time when the market will change from one volatility regime to another, VIX is a good indicator of which regime we are in at the moment.

If we have a VIX level below 16, that means volatility is low and there isn’t much fear in the market. Usually, this is a period of a smoothly rising market. This is ideal for a bullish version of double diagonal.

At some point the market tops out and VIX starts rising, perhaps with some price movement down, or maybe with a sudden move down. This is when we want to at least get neutral in our double diagonal approach.

If the market moves to a rapid decline, VIX may jump above 20 or even above 25. This would be a time to skew our approach to a bearish Delta, and perhaps reduce our short put position. We try to harvest gains in our long puts.

At some point the market bottoms out and usually has a rapid bounce back. During this period VIX starts declining, so we want to have less duration in our longs to reduce our Vega values. We may want to reduce our short call exposure, and shift to a more bullish overall Delta.

Eventually, the market settles into a more stable environment and VIX again drops below 16 and we are back to a smooth rising tide again. While a bit of an oversimplification, this is the pattern we often see repeating over and over. Sometimes these changes in regime are severe, and sometimes subtle. However, it does seem that they are becoming more frequent and shorter in duration. As much as a trader can identify changes and adjust accordingly, they have a chance to reduce some of the bigger potential losses from this very risky trade.

Move longs out of the money (9)

Our base set up was to have all of our strikes at the money. Keeping our long strike values close to our short strike values should give us good protection, at least in theory. We may even think that we should move longs into the money to be even more protective. I’ve thought that as I’ve considered ways to construct this double diagonal trade. But after a lot of testing and trial and error, I’ve seen that often moving the longs out of the money works better. Let’s see why that might be.

First off, moving the longs out of the money makes them less expensive. The premium is less to pay. However, you don’t get a free ride on buying power, because most brokers set your buying power requirements based on the difference in strike prices between the short and the long. So, if you sell a short put with a strike price of 6000 and buy a long put with a strike price of 5950, your broker will likely look at that as 50 points of risk, or $5000 for a 100x multiplier. But if the calls and puts don’t overlap, you will only get dinged for the largest gap because you can’t lose on both put and call spread widths at the same time.

By moving the long strikes out of the money, the Delta value of each strike is less. Price moves have less impact on the longs. On a move, the winning long gains Delta, while the losing long decreases Delta. With less premium and less Delta, the losing long will have less to lose.

More importantly, moving longs out of the money reduces Theta values, which is in our favor. Since long Theta is a drain on our profits, we want to minimize this value.

Treat the longs as a profit generator (10)

As mentioned above, when the market moves, the winning long gains Delta and profit, while the losing long loses Delta, and usually loses less than the winner. So, if we adjust and aggressively re-center to capture profits from price moves, we can make money on both up moves and down moves on the long side.

The opposite is true for the short strikes- aggressively adjusting to re-center will tend to lock in losses, so we need to consider different adjustment strategies for longs vs short strikes.

Stay small, and water down with cash (11)

Of all the considerations for reducing risk, the most important one for almost all option strategies is to stay small. What does that mean? Keep this trade a small percentage of a portfolio, so that a big loss is not catastrophic to your overall account. If a trader were to use all their buying power in an account on this trade, it is almost guaranteed that the account would go bust within a year or two, no matter how many of the other risk management techniques are used. This trade just has way too many large drawdowns over time that can’t be anticipated. On the other hand, if a trader had 5% of an account’s buying power using this trade, even a loss that takes more than all of the trade’s capital, say 7% of capital wouldn’t be that bad. And if the other 95% was in cash equivalents collecting interest of 4%, that will also buffer losses.

On the flip side, keeping this trade small does reduce the positive impact of outsized gains. If the trade triples its value- a 200% gain on 5% of an account, that would be a 10% increase from the trade, plus the cash return on the other 95% of the account.

Another related risk mitigation strategy is to resist the urge to compound returns by increasing the number of contracts when good returns pile up. Increasing contracts increases risk, so proceed with caution. Look at gains as an opportunity to take money off the table.

What’s the right percentage? Can some of the other parts of an account be other assets or other trading strategies? Each trader has to determine what is best for their situation and risk profile- the key consideration with this point is that making a risky trade a small portion of an account makes the total account less risky than a risky trade all by itself, and the smaller the portion of an account, the less that risk impacts total returns.

Pulling it all together

I’ve been trading variations of the Daily Double Diagonal for over a year now. I’ve tested all of the above adjustments in my trades, plus back-tested lots of other variations that I haven’t even mentioned. So, is there a trade here? I think so.

No matter what, anyone who trades something like this should be prepared for volatile returns, lots of good days, with some occasional very ugly days, sometimes a string of ugly days. Why put up with that kind of volatility? Because on average, this trade can average 20-40% return on capital per month. But that is an average, so some months are higher, some much lower, including losses of 100% possible. So, a trade like this can use a small part of a total portfolio to juice up returns over time if you can withstand the ups and downs. I keep 2-3 times the amount of capital that I use for this trade in cash or cash equivalent funds that I can easily access. So, for every $10,000 I trade in this strategy, I have $20,000 -30,000 in cash in case the trade goes badly for awhile. The reason I’m picking $10,000 is because one contract of SPX at the strikes I tend to use requires about $10,000 to get into, maybe a little more or less. But I think of my position as using $10,000 for the four different strikes of the Daily Double Diagonal position. This can also be done with SPY for 1/10 the cost, but you have to watch dividend risk and early assignment risk if one of the short options gets in the money. I use other trades and positions to further diversify beyond just having cash for this trade. In total, I keep this trade under 5% of my account.

Let’s try to simplify the approach down to something manageable. Here’s how I try to set up and manage this trade. Unlike most of my strategies, I don’t focus on Delta targets for individual strikes, but I do keep an eye on the overall Delta of all positions.

For a neutral set-up, I aim to sell my short put and call around 0.5% out of the money with 7 DTE. So, for SPX trading around 6500, I would look for a put 30-40 points below the current price, and a call about 30-40 points above the current price. This is my starting target and the ideal strikes. Once the market moves though, I’m rarely there because I roll up or down based on what the market does and I don’t want to overadjust, which will lock in losses from the losing side (from point number 3 above).

I like to roll my strikes each day between 30 and 60 minutes into the trading day, after the initial moves at the open have played out. There’s nothing magical about this time- I just like to get it done and move on. My personal way of adjusting my short strikes each day is to adjust toward my ideal in an amount that depends on where my strikes are when I roll. If my strike is out of the money, but no more than 1% out of the money, I’ll roll 10 points toward my ideal strike. I should be able to collect a credit by rolling out one trading day. If I’m more than 1% out of the money, I roll at least 20 points toward my target and enough to get within 1% of the current price. This way I don’t let my short get too cheap where it can not contribute if the market keeps moving it further out of the money. For any short strikes in the money, I roll at least 20 points toward my target, and if I’m more than 0.5% in the money, I roll to get within 0.5%. I’m more aggressive here because I don’t want to let my Delta get too high and cost me if the market keeps pushing my in the money strike further into the money. Keep in mind that my overall goal is to have both short strikes out of the money, but with this adjustment strategy, I probably have one short strike or the other in the money almost half the time.

Between my two short rolls, I should almost always collect a net credit. The point of this set of guidelines is to avoid over adjusting as the market bounces around from day to day. It is frustrating when you move your strikes a bunch and then the market moves right back to where you just had your strikes centered. With a rolling 7 day window, there isn’t an urgency to be centered every day. And it can be costly to center your short strikes every day. Moving in increments allows the trade to profit as the market bounces up and down from day to day.

For the long strikes, I have a different approach. I try to buy about 1% out of the money on both the put and the call side. Each day I roll to re-center my longs to be at my target strikes. When I do this with my longs, rolling to my target gives me the best chance to profit if the market makes a move.

Adjusting for low and high VIX

When VIX is low, generally under 17-18, I like to extend out my longs, to the 28-35 DTE range. I like this time frame because there are still plenty of strikes with decent volume, although I may not have choices to roll out a day at a time. I also move my long call strikes to the first strike above the current price, while keeping my puts well out of the money. This makes my long position a little bullish. With longer duration, I don’t have to roll the longs every day, I can roll more opportunistically, based on when the market moves.

For my short positions during low VIX, I bring my put strikes to just below the current price as a target, and keep my calls out of the money. I still follow my short adjustment strategy, but I don’t let the puts get far out of the money, and I don’t let my calls get as far into the money when the market is moving up consistently.

This combination allows me to harvest short premium and reduce the amount of Theta loss from the long side, while also gaining from an increasing market.

Eventually, all good things come to an end and I’ll take some losses when the market turns negative.

For high VIX, over 20, I switch my long strikes to shorter durations, 14-21 days, to reduce their cost and their Vega exposure. I generally don’t do this all at once, because Vega works for the longs as VIX goes up, so I just hold my expiration steady and adjust my strikes day by day when VIX is increasing, letting the duration decline day by day.

For my short options, I consider eliminating them or cutting my short exposure as VIX gets over 25. With sharp moves up or down, big losses on the short side can frequently occur and until the bottom is in, it is hard to tell which way the market will move going forward. Once we get some clear good news and we have a day or two of a bounce off the bottom, I add my short put back into the mix at full strength. When VIX gets down to 18, I add my short calls back into the mix.

All of the high VIX moves are intended to allow me to profit from big volatile moves, while avoiding losses on the short side. From experience and back-testing my biggest losses, both real and simulated were during periods of high volatility. Another choice would be to get out completely during high VIX periods, but I look for ways to keep trading.

In between, during medium VIX periods that aren’t high or low, I look to be more neutral overall and wait for the market to either get to a high or low VIX environment.

Most importantly, I keep this trade at a small portion of any account I trade it in and I keep a large cash buffer to be able to make adjustments day to day and have money needed if the trade has a series of losses. I do track the trade separately from the rest of the account to keep the performance front and center in my day to day management and tracking systems.

I can’t say that this approach works perfectly, or that it prevents losses. Each setup is making an assumption that the market will behave a certain way in the near future, and the market isn’t always cooperative in following historical patterns. So, big losses happen from time to time. With each big loss, I look at whether I followed my plan, and if I could have done something differently based on what I knew at the time. Monday morning quarterbacking is only useful if you consider what you knew at the time, not what you know after the fact. The market doesn’t care about your opinions about what it should do, or how you think it should react to news, it just does what it does. Spotting when the overall market environment has shifted isn’t easy, and doesn’t always make sense. My take-away is when in doubt, get as neutral as possible.

In the end, I’ll go back to my original thoughts on this trade. The Daily Double Diagaonal is clearly not for everyone, and probably not for very many people at all. It is extremely high risk and high reward. It is the best trade you can imagine at time, and it is the worst trade you can imagine at others.

As with all trades, I find keeping a trade log and reviewing results to be very helpful for this trade. Some periods seem extra profitable, while others don’t make nearly as much profit as I think I should. Going back to my logs help me see what happened and I can evaluate whether I could have traded better. I track each of the four legs independently and total them over time to see how each is contributing vs what I would expect. This helps me understand whether I’m optimizing each leg appropriately in different trading environments. This is probably the best way to learn the most about this trade.

I don’t recommend any trade in general, but I urge readers to be extremely cautious in their consideration of this trade. I can’t stress enough how quickly it can lose money in any trading environment. As I’ve mentioned in comments on other pages, I’ve hesitated to even finish writing this and to publish it because it is so risky, but I finally decided to go ahead with it, with as many cautions and warning as possible. And keeping the trade to only a small part of an account reduces the impact of worst-case scenarios.

Best wishes for trading the Daily Double Diagonal. I’ll follow up with a post on my personal results over time trading this.