The following is a listing of recent additions and changes to the site. For frequent users, this change log might be helpful to see what has been added new or changed.

July 30, 2026: Added an extensive post on How to Collect 10% Annual Income from Selling Covered Calls and Collecting Dividends on P&G Stock. This is written to a specific audience, but anyone interested in selling and rolling covered calls on blue chip stocks will hopefully find this an interesting read.

April 21, 2026: Added a post with results of trading the Daily Double Diagonal for 14 months, averaging 30% return per month or 400% total.

April 13, 2026: Added a new page on rolling Daily Double Diagonal trades. A four legged trade with calls and puts, long and short. A very high risk, high reward trade.

January 15, 2026: Added a new page on Uncomplicating Option Pricing and Greeks. Did we succeed?

January 13,2026: Added a new post on using a household balance sheet. Slightly off the topic of options, but something every trader should use in some form or another.

December 1, 2025: Added a new page on Best Option Order Entry Practices. Sometimes, it’s good to get into the nuts and bolts of trading a bit.

October 14, 2025: Added a new page on Rolling Credit Put Spreads. While I’ve written about this before, this is a more thorough version explaining how rolling works mechanically with put spreads.

September 17, 2025: Added a short post explaining that the site was back up after a week down. I appreciate the patience of all who had to wait, and the persistence of those who found ways to reach out to help get the site back up.

August 2, 2025: Added a page comparing the 111 and 112 put ratio trades. It’s been a year since the Implied Volatility blow-up that crashed so many naked traders, so it seemed like a good time to re-visit.

June 26,2025: Based on popular demand, I’ve added a page on selling covered call spreads. This strategy allows a trader to collect premium on existing shares without giving up all the upside potential if the stock goes up a lot.

June 17, 2025: Added a post featuring an interview about the Broken Wing Butterly that is featured on YouTube and ThetaProfits.com.

May 29,2005: Added a new post on the benefits of rolling a covered call.

March 13, 2025: Added an update to the Very Long and Very Short Diagonal Put Trade. This trade becomes truly unmanageable during extended down markets, making it an interesting concept to study and test, but not viable as an ongoing practical strategy.

February 9, 2025: Added a page with an updated write-up of the Delta Neutral Back Ratio Call Spread, as featured in the new YouTube video interview with John Einer Sandvand from ThetaProfits.com. This is an updated analysis from an earlier page on the same topic.

January 17, 2025: Added a new post on a Backtest for Optimizing Diagonal Put Spreads. This builds on the previous articles on diagonal puts spreads rolled daily.

January 14, 2025: Added a new page on the Daily Diagonal Covered Put trade. This is similar to the earlier Very Long Very Short Diagonal, but with much shorter duration and less capital required. I even included a backtest.

December 16,2024: Added a new page for the Very Long Very Short Put Diagonal Trade. This trade, also a version of a “Poor Man’s Covered Put” has much more to than what one would expect at first glance. However, this trade has elements of almost every aspect of options there is, so a lot to study for every option trader.

October 30,2024: Added a new post with a cautionary tale of trading the 112 trade on August 5, 2024, the fastest volatility spike ever.

October 2024: Lots of new comments from readers and responses on various pages of the site. Keep those questions and ideas coming!

August 24, 2014: Added an update to the page about 100% success in the 112 trade to highlight the issues with the August 5 volatility debacle that did wiped out many 112 traders.

July 23, 2024: Added a new post sharing results from the 112 trade in the first half of 2024. 100% success.

July 2,2024: I added a new page contrasting debit vs credit option trading strategies. It’s one of a few considerations traders should consider when picking strategies that work best for their style of trading.

May-June 2024: Lots of new comments and replies came in from readers. Always good to hear from folks with their questions and comments.

December 30, 2023: I added a couple more books to the Resources page. I also updated Tasty links for their new TastyLive.com URL.

December 20, 2023: Made a number of changes and additions to the home page of the site. With all the new content, it seemed like it was time to highlight some of the content that isn’t as obvious.

November 22, 2023: Added a duplicate post on the 1-1-2 Put Ratio Trade. I did this to capture the search engine traffic from the numbers of traders looking for information. So, whether it’s 112 or 1-1-2, there’s a write-up. Just read one or the other- they are the same.

November 14, 2023: Added a page on the 112 Put Ratio Trade. While I mentioned it a bit in the post on the 1112 Put Ratio Trade, I decided the naked option version deserved a write-up of its own.

September 19, 2023: Added a page on Covered Calls. Yes, I know I just wrote a post on the same subject. (Secret note: the write-ups are exactly the same. This is actually a test to see if pages do better than posts in getting search engine connections. Universally, my most read articles are always pages, but maybe that’s just a coincidence. Most readers would never recognize the difference between a page and a post, but posts are supposed to be part of an ongoing blog, while pages are more “permanent.” I’ve used them interchangeably, and I want to make a data-driven decision on what the impact of that choice is.)

September 18, 2023: Added a post on 5 Bullish Call Trades. This is the culmination of a series of trades that I felt like I had overlooked regarding data driven ways to utilize calls in a bull market without absorbing too much time decay. With the market in what appears to be a bull market, it was time to focus in on this topic. 4 of 5 of these trades have recent extensive write-ups that were completed in the past 3 months.

August 4, 2023: Added a post on Buying Out of the Money Call Spreads. This is a strategy that would appear to most option traders who mostly sell options to be a sure loser, but back-testing shows it to be quite profitable over time.

July 26, 2023: Added a post on the Poor Man’s Covered Call, a low cost variation of a Covered Call, based on selling a call against an in the money long call that acts as a replacement for stock. So, a bit of a cross combination of the two most recent previous write-ups.

July 25, 2023: Added a post on Covered Calls. Not sure why I never wrote one before, but given it is one of the most popular option trades around, I thought it was time to weigh in on it with a level of detail that isn’t available many places.

July 5, 2023: Added a post on Replacing Stock with a Call Option. When markets are going up and IV is low, buying calls can be a good way to get in at a low cost. This post goes into more detail.

June 19, 2023: Added a post on Underlying Security vs Risk Permission. There are a lot of factors to picking the type of security to buy or sell options for a specific type of trade. This post digs into what to consider and why some approaches may be better than others.

May 24, 2023: Added a post on Trading Options while working a Full Time Job. I went back to work this year and changed my trading routine. I know many readers can relate, even if they just want to make better use of their time.

May 20, 2023: Added a chart to the 1 DTE Straddle post to show profit and loss at various times of the day.

May 17, 2023: Added a post on Covered Strangles, a conservative options trade that reduces volatility with higher probability of profit than owning an equivalent amount of stock outright. It’s my first deep dive into Level 0 option trades, something I’ve had a number of requests to address.

February 27, 2023: Added a new Phone Stock Charts page with stock price charts formatted for a smart phone, and potentially screen-cast onto a monitor or TV. Not for everybody, but if this is something you are looking for, like I was, you’ve found it.

February 27, 2023: Updated the Current Prices page with more interactive charts, replacing those from a previous provider that had security flaws.

February 26, 2023: Added a post on the topic of 0 DTE trades.

January 16, 2023: Provided responses to a couple of great reader comments and questions regarding the 1-1-2-2 trade.

January 13, 2023: Added a new post on my 2022 learnings.

January 3, 2023: Added a new post on buying 1 DTE straddles on indexes.

December 28, 2022: Added a new page describing the 4 Different Types of Option Underlying Securities– stocks, ETFs, indexes, and futures.

December 23, 2022: Added a post regarding the best Delta for ROLLING put spreads. This is a new topic that I had curiosity about from years of observing that some rolls do better than others, and I couldn’t figure out why.

December 20, 2022: Added a post researching the best Delta values for selling put spreads. This is a follow up to page on credit put spreads written earlier.

December 6, 2022: Added a page on Options Portfolio Management.

November 28, 2022: Accepted an extended comment to the page Rolling Iron Condors and added a response. Comments are always welcome and appreciated. Note that comments from first time commenters must be reviewed and accepted to keep those crazy spammers from ruining the site.

November 9, 2022: Response added to a comment about how to roll a back ratio call spread up or down to get back to Delta neutral.

November 3, 2022: Added a new page on Options Margin Usage. In this page, I compare different types of margin available for option traders and the benefits and risk of each.

October 15, 2022: Worked with the ad provider to reduce the number of ads on the site and make them less obnoxious. Should be no more pop up adds when changing pages, and less ads per page.

September 30, 2020: Added a new page explaining how brokers permit different levels of risk in option trading.

September 7, 2022: Updated the Favorite Strategies Page and the Ratio Spread Page, adding more details to both.

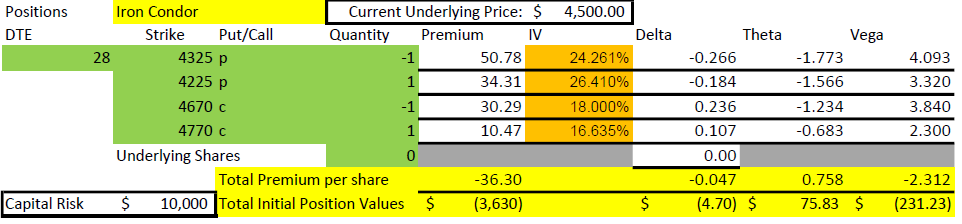

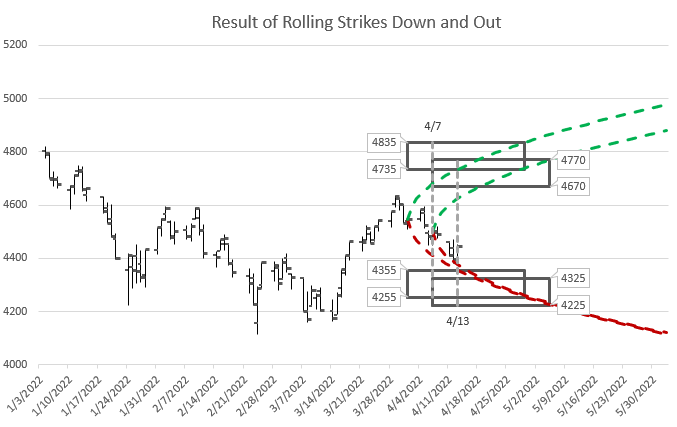

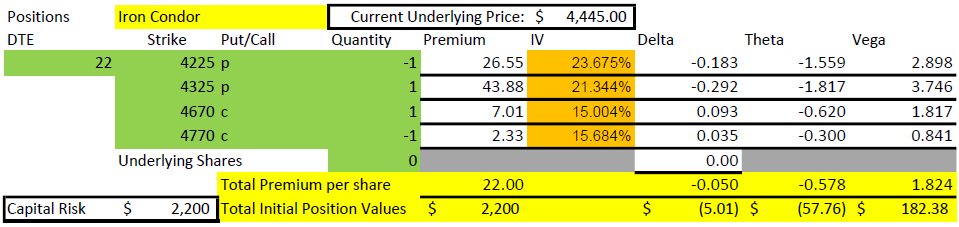

August 25, 2022: Added a new post with an example that illustrates the Goals for Rolling Iron Condors.

August 23, 2022: Replied to a new comment about my alternative 7 DTE trade posted a week ago.

August 18, 2022: Added an alternative strategy in a comment for the post on 7 DTE trades.

August 18, 2022: Added a post describing the 1-1-2-2 Ratio trade.

August 2,2022: Responded to a comment on rolling Iron Condors with perspective on defending call side in up moves.

June 5, 2022: Added this page- the change log

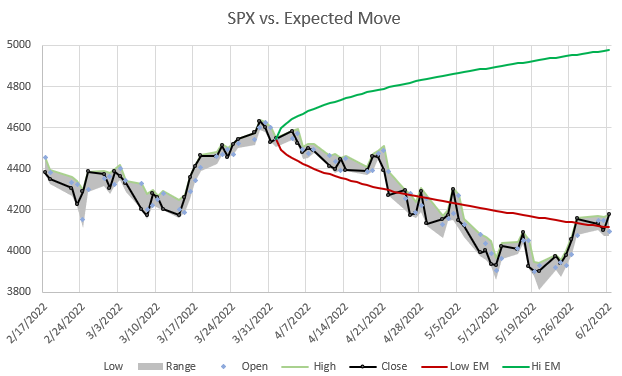

June 5, 2022: Added new post explaining the Expected Move and how to visualize it.

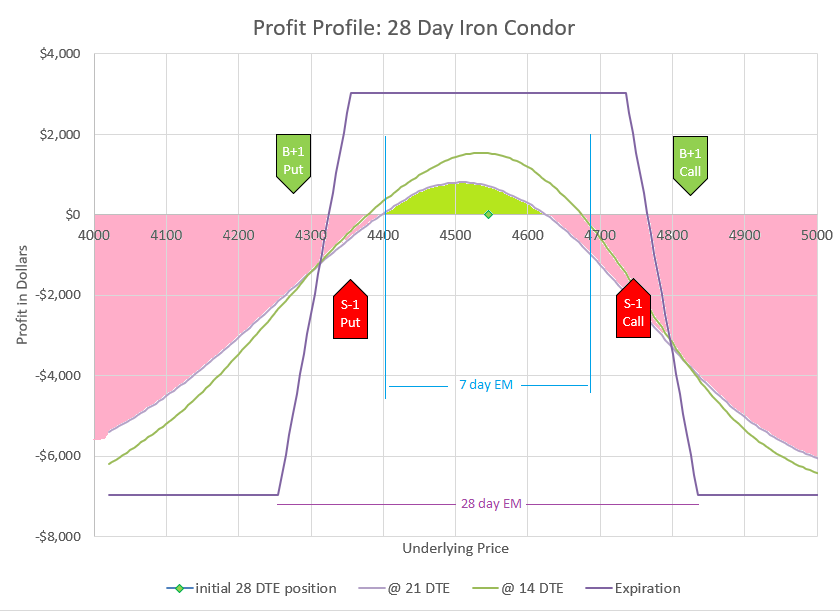

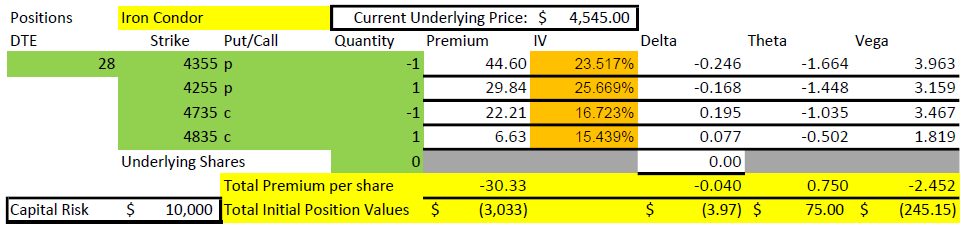

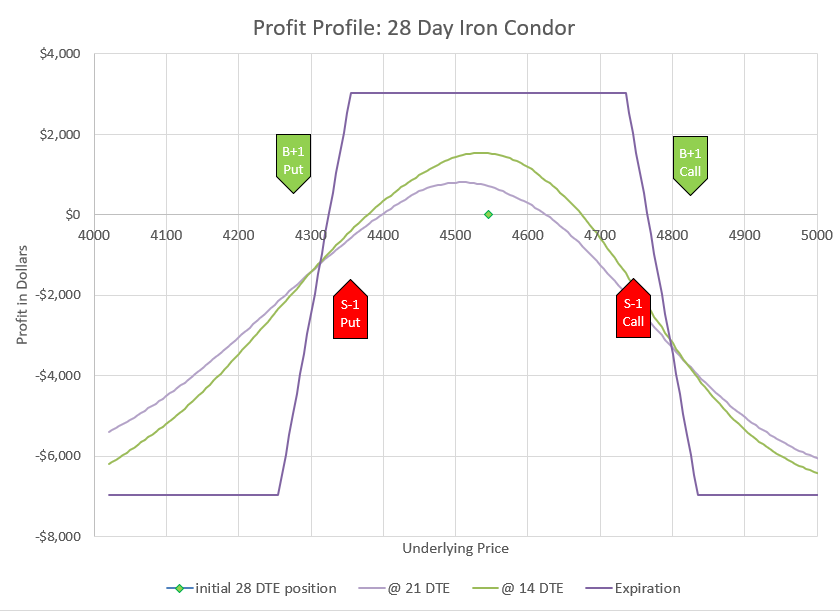

June 4, 2022: Added a new post explaining my approach to rolling Iron Condors in bear markets.

March 12, 2022: Added a post explaining different types of options on the S&P 500 index products.

January 14, 2022: Added a post about comparing risk of different option strategies.

If there are subjects you’d like me to address in future, leave a comment below.