Most people have full time jobs. Can someone manage an options portfolio and work full-time without watching the market all day? I say yes.

Most people have full time jobs that don’t involve the financial markets. Can someone manage an options portfolio and work full-time without watching the market all day? I say yes, and they may do even better than a full time trader. The reasons may surprise you.

For several years I was a full time options trader, watching positions in a bunch of accounts, adjusting every day as the markets moved. Many of my positions were short duration, which meant that I needed to stay on top of them. Much of my strategy involved rolling to avoid getting to expiration or to keep my strikes out of the money. There were lots of good reasons to spend the day reviewing every position in every account to determine if any adjustments were needed. And I enjoyed it. It was fun managing accounts that were growing and generating the income I needed.

But in 2022, I had a series of events that drained my accounts that provided my spending money. (Separately, I’ve written about my lessons learned in 2022.) I’m not yet to the age where I can take money out of my retirement accounts without penalty, and I didn’t want to get into Substantially Equal Payment Plans (SEPP) to commit to withdrawls- that’s a big topic for another day in itself. The bear market coincided with some unexpected expenses, so I liquidated most of the liquid accounts I had available at bad times. My accounts that had been providing nice streams of income lost a lot of value when I needed them most. So as the year came to a close, it was clear I needed to get a “real” job again.

Changing to a full time “real” job

In January of 2023 I started working full-time, a typical 9-to-5 job. But I still had a number of accounts to manage, a combination of retirement accounts and leftovers from my cash/margin accounts that I hadn’t completely used up. (I didn’t go broke, I just wasn’t flush enough to live off my accounts that I could draw from.) I had to have a different approach to account management- the days of full-time trading were over.

I still wanted much of my portfolio to be option-based. I’ve seen how options give me leverage and the ability to manage in any type of environment. But I knew that my approach to managing daily had to dramatically change. I couldn’t watch the market and do my job, so I needed to completely change my trading routine.

First, I decided to stop all 1 DTE and 0 DTE trades. Honestly, these had not been that profitable and were the most time-consuming positions I had been trading. It was almost like I had been trading them to keep my day completely filled with activity. If you read about my 1 DTE Straddle management approach, you’ll see that I try to take profit and adjust positions throughout the day, which is very time-consuming. 0 DTE trades are just as time-consuming for most strategies. I know some traders open a position and set up stop and profit limit orders and go about their day, but even that seemed like more than I wanted to do. So, no more expiring option trades.

Next, I moved all my shorter duration trades out in time. I was doing some 7 DTE put spreads, rolling almost every day. These were problematic in the 2022 bear market anyway, so it wasn’t a hard decision to get rid of them. I also decided to mostly stop doing 21-day broken butterfly trades. This was a harder decision, as I’ve had good success with defending these even in tough times, but I knew that I just didn’t want that responsibility to keep an eye on them.

So, I was left with positions mostly 4-7 weeks from expiration- put spreads, iron condors, covered calls, covered strangles, some 1-1-2 ratios, and some long duration futures strangles. All these trades are far enough out in time that a move during the day won’t be a huge loss or need an immediate adjustment.

Initially I thought I’d try to spend a half hour each morning when the market opened before I started my job. For a few weeks I did this, but I found that my work often required me to be available for an early call during that time, or there were urgent items that couldn’t be delayed, and that time wasn’t available. I’d miss a day, then it was two or three in a row, and I realized I needed to be able to have an approach that could go several days at a time without requiring action. But, I also noticed that missing several days wasn’t hurting my market results, especially in a choppy market.

Since almost all my trades are based on profiting from premium decay, time is my friend. I need time to pass and the market to remain somewhat stable. Getting away from the daily noise of the market up for some reason one day and down the next for another reason helped remind me that selling options is about being patient. It also reminded me that market movements are mostly noise that is statically insignificant. If I don’t react to every move, the market tends to chop up and down and not really move that much or that fast over time, which is exactly what a seller of options needs.

My new routine

With time, I’ve settled into a trading routine of doing a thorough review of all my positions about once a week. For positions in the 4-7 week to expiration window, I like to roll and adjust Delta about once a week, essentially kicking the can down the road, trying to pick up a percent or two of return on capital each time. Timing isn’t critical, but I want to keep my spreads in the sweet spot where they decay the most, with short strike’s Deltas in the high teens to low twenties. I’ve written about this in many posts that address best Deltas for put spreads.or for rolling put spreads. I’m leaving a bit of money on the table, missing the very best timing, but I’m making up for that by not over trading, which I clearly was in 2022.

Some of my longer duration trades, that are 2-4 months out, can go weeks or even a month or more without an adjustment roll. My weekly checks just make sure that they are not getting close to being tested or getting to a duration that I want to extend. My philosophy with those positions is an “if it ain’t broke, don’t fix it” approach. So, not much to do with these.

So, it takes me about an hour a week to make adjustments during market hours. I find a break in my day, or a day when I can get trades in early before my work day starts. I’ve been surprised at how manageable it all is. I’ve realized that when the day comes that I don’t need a job anymore, I will be able to manage my trades with a lot less time than I was using the last several years. I don’t plan to ever trade all day long again.

Results

The great news is that I’m very happy with my results. My most aggressive accounts have been pulling in about 10% returns each month so far in 2023, and all my accounts are handily beating the market. So, I’m very happy with my new approach. I know that the market isn’t always this calm, but I also know from 2022’s bear market that longer duration trades in high volatility have much better outcomes than short duration trades, so I’m confident that this approach would have done well in that environment, better than I did trading every day with short duration trades.

I’ve noticed some put spread rolls collect more credit than others. This study shows that there is an ideal Delta for rolling put spreads

After trading put spreads for several years, I’ve noticed that some rolls collect a lot of premium credit, and others are a struggle to collect any credit at all. I decided to study this to see if I could find if there is a “sweet spot” for rolling put spreads based on Delta values. I’m happy to report that there is.

It’s no secret that if a put spread gets fully in the money, it is impossible to roll to the same strikes in a later expiration for a credit. But when a spread is out of the money, I’ve seen a wide variation in credit when I roll, and I’ve often thought that there must be a best place to make a roll to get the most credit. If there is, I could devise a strategy to take advantage. So, I copied some option tables into Excel and pivoted the data a few different ways to figure out how premium from rolls vary.

Before jumping into the study, let’s discuss what rolling option spreads involves and why we might do it when a spread is out of the money. Rolling is one three ways to manage an exisitng trade- I covered the three ways in the page on managing by holding, folding, or rolling. One of my common management techniques is to continuously roll a position- I let the short spread decay in value, then roll it out in time to get more premium, and then let it decay all over again. Just repeat over and over. For those not familiar with the roll concept, rolling means executing a trade where an existing position is closed and a new position is opened all at once in one trade. The new options may be at the same strikes, which would be rolling “out,” or the strikes may be higher, which would be rolling “up and out,” or we could also roll “down and out.” Rolling a credit put spread that is out of the money out to the same strikes, will almost certainly generate a credit, which is the goal of this strategy. I’ve discussed this -approach in detail in other pages of this website, including roll for 6 percent a week, goals for rolling Iron Condors, the power of rolling Iron Condors, and rolling losing positions.

Rolling Spreads in the Study

I looked at a lot of different combinations of rolls, different durations, different times between durations, and I saw similar results. In the interest of keeping this write-up from getting lengthy, I’m choosing to just show a few examples.

7-10 DTE Roll

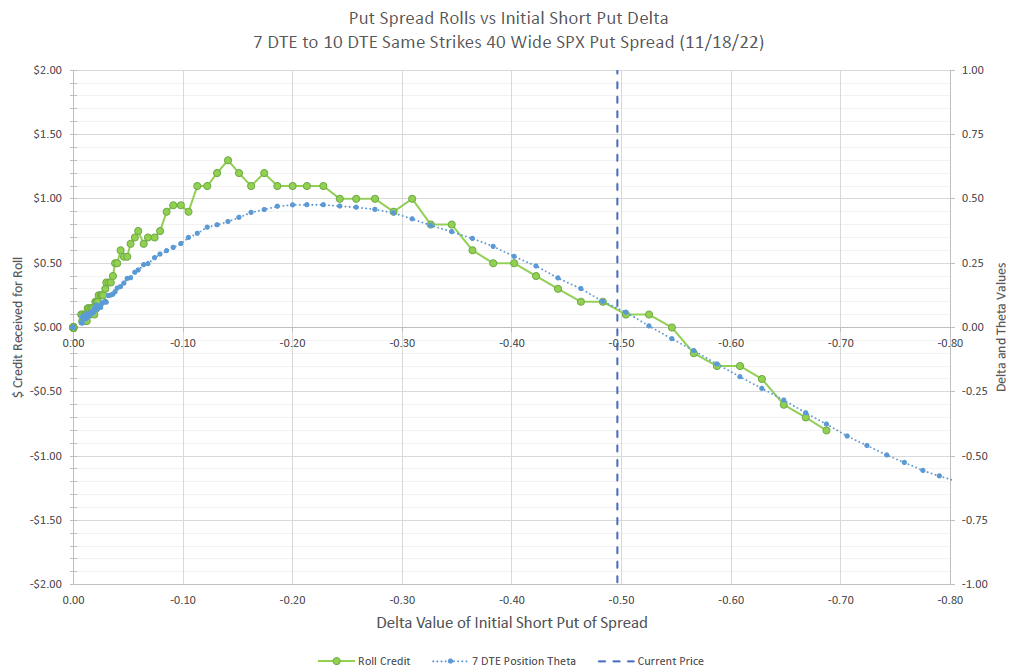

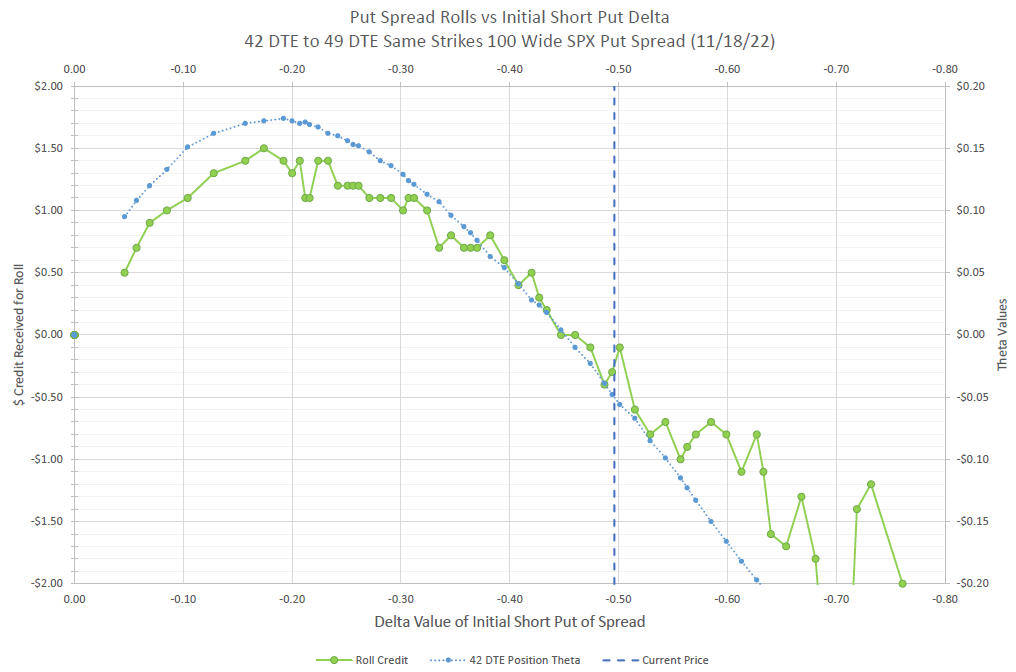

While I don’t trade a lot of options with durations of a week or less, I thought it would be good to look at this timeframe as the lower end of timeframes where we get outside of current week expirations. The following chart shows all the available combinations of 40 wide 7 days to expiration (DTE) SPX credit spreads rolling to the same strikes at 10 DTE.

Rolling out from 7 DTE to 10 DTE has the best credit when the 7 DTE short strike is between 10 and 20 Delta. Note that the Theta peaks at a slightly higher Delta.

I’ve shown the net credit for each roll combination, as well as the raw Theta difference for each existing 7 DTE 40 point wide spread. The x-axis is the Delta of each 7 DTE spread. The roll credit is shown on the left axis, and the net Theta is shown on the right axis. Looking at a peak value of approximately $1.20 per roll, we would collect 3% of the 40 wide spread. Meanwhile, the peak Theta of around $0.45 per day would equate to 1.1% of the width. So, holding might get a similar daily return, but with increasing risk as expiration approaches, but a roll would allow us to collect 3% and still collect additional Theta over again. Actually, that’s double counting. The Theta would just be the decay of the premium we are collecting. Just a few ways to think about the transaction. We can also look at actual strike prices and look at a few other values.

This graph shows roll credit plus Delta and Theta values for the positions

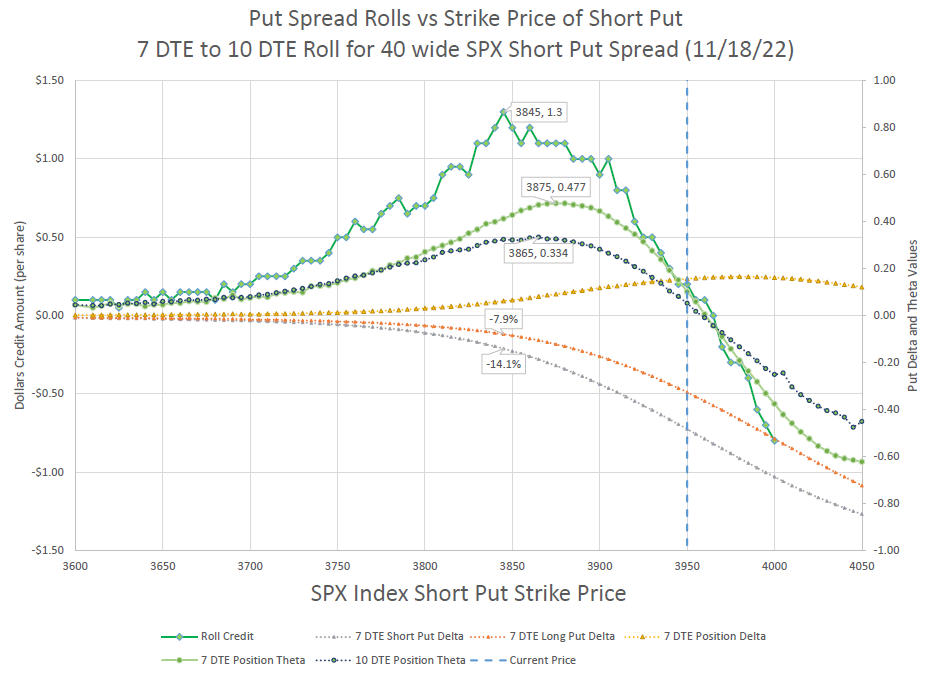

On this next chart, I’ve shown the x-axis as the strike price of the short put of the credit put spread. I’ve also added the Delta values of each of the puts for the 7 DTE spread as well as the Delta of spread position. In addition to the net Theta of the 7 DTE spread, I added the net Theta of the 10 DTE spread that we would roll to. So, each strike price on the x-axis is tied to six different pieces of data for a potential spread roll. While the roll premium and net Theta of the 7 DTE spread is the same information as the previous graph, the additional data can add more context.

Note that the Theta values of the longer duration spreads are generally lower than shorter. That should be expected. More time means slower decay. But the new spread will have a slightly higher Delta, which moves the peak of the Theta curve down in strike prices, because as we have seen in our study on maximizing Theta for a put spread, Theta tends to max out at short Deltas around 20, which will be further down after a roll. So, note from the chart that the maximum roll premium lines up for the most part with the maximum Theta of the spread we are rolling to.

The take-away from the Delta information on the chart is that as we get closer to the current price and have higher Deltas, the net Delta goes up, and the value of rolls goes down. Also, if Delta gets too low, there isn’t as much premium available in a roll to the same strike prices. I picked out the Delta values of the spread with the highest roll value, and it is approximately 14 Delta on the short strike and 8 Delta on the long strike.

So, the ideal scenario is to start with Deltas of around 20/13 and see the positions decay and Deltas to decline to 14/8, and then roll out to new strikes with Deltas of 20/13. If only the market would cooperate with our plan and let us do this all the time. Obviously, the market isn’t that consistent, so we have to manage in other ways.

Sometimes, we may want to roll down and out. Let’s look at the premium for 40 wide spreads and see what is possible if we want to collect a credit.

Looking at the premium differences, we can see opportunity to roll down at some strikes more than others.

On the above chart, I have plotted the premium value of 40 wide put spreads at 7 and 10 DTE, along with the premium collected to roll out to the same strikes. I’ve also highlighted possible rolls down and out. The highest strike where it is possible to roll down a strike and collect a credit is to go from 3920/3880 at 7 DTE to 3915/3875 for a 10 cent credit. When a spread is being tested, every bit helps, but clearly this roll doesn’t give the position much more breathing room. On the other hand, if we had the 3800/3760 spread, we could roll down 25 points to 3775/3735 for no cost. So, again it pays to stay away from being tested. But at this short of timeframe, it doesn’t take much of a move to get a spread in trouble, so let’s look at how a little longer duration would fare.

21-42 DTE

Let’s look at an example that generally matches up with the common strategy often associated with TastyLive.com. Interestingly, values peak out at about the same place based on Delta.

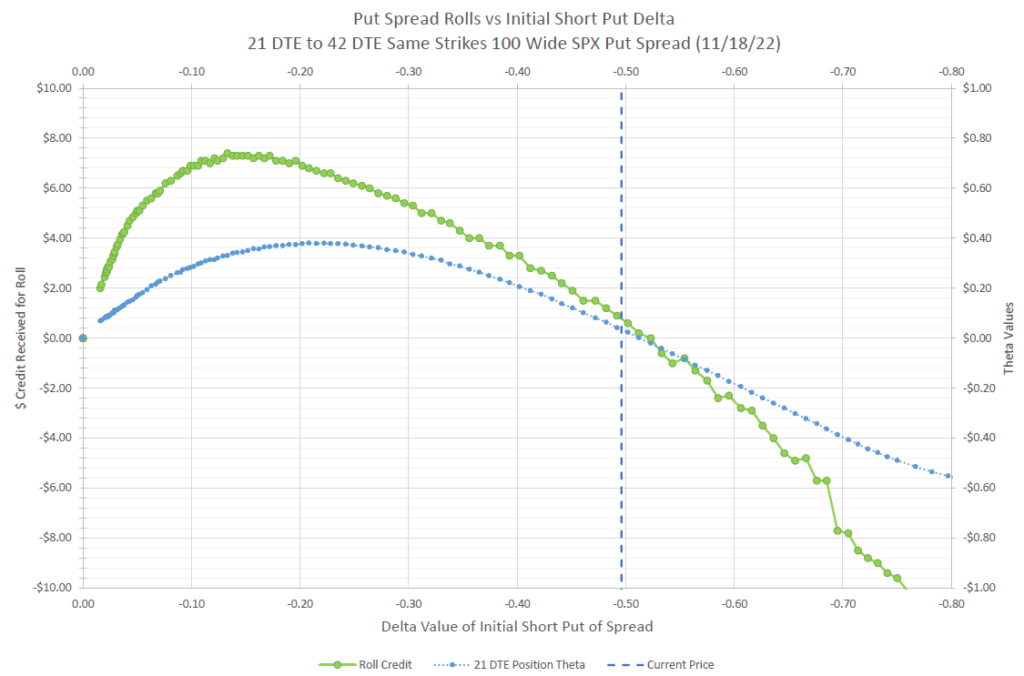

This example shows rolling from 21 DTE to 42 DTE, essentially doubling the time until expiration.

Again, the best premium for a roll is in the mid to low teen values of the Delta value of the short strike of the 21 DTE spread. Here we are collecting just over $6.00 to roll our 100-wide put spread out to 42 DTE. In that case, we would be collecting an additional 6% of the width of the spread. The 21 DTE spread would be decaying about $0.30 per day, so the roll allows us to collect around 21 days of decay in cash.

Notice that the observations we made on the 7-10 DTE roll hold almost exactly the same on the 21-42 DTE roll, even though we have much higher time to expiration, wider spreads, and proportionally longer rolls. One difference to note is that amount of premium and Theta are much less on a daily basis, but that should be expected as daily decay for similar Deltas gets higher as expiration approaches.

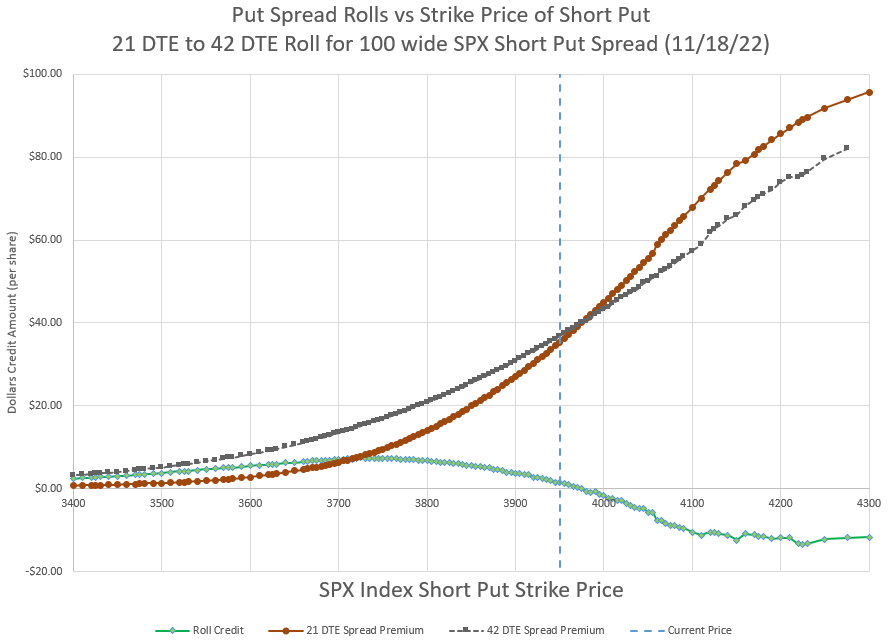

This graph shows the premium levels of 100 point wide spreads at 21 and 42 DTE, as well as the premium collected to roll out at the same strikes.

Another key difference is the distance that our strikes can be from the current price, giving the position more wiggle room for price changes. The above chart shows the premium of the various spreads available at 21 and 42 DTE. Notice that the lower strikes approach zero value while the spreads at higher strikes approach 100, which is the width of the spread and would be maximum loss for a credit spread at expiration. With spreads, the closer expiration gets the more of an S-shape we get when charting the premium. Since we are selling the spread, we’d like to see the value decay, either by staying out of the money as time goes by, or seeing the price go up, which would shift all the lines to the right on the chart.

What if we want to roll down to lower strikes when rolling out from 21 to 42 days? Let’s look at what would be available by zooming in a bit to the chart above to the area where there is credit available to roll out.

In this chart, we can see that the further we are out of the money, the more we can roll down for a credit. Once a spread is in the money, the opportunity to collect a credit is gone.

With plenty of time to expiration, we can roll out for nice credit or roll down quite a ways for some credit. For example, in the chart above, the 3700/3600 spread could be rolled down 150 points to 3550/3450 for 20 cents credit or rolled to the same strikes for $7.50 credit. The closer our strikes are to the money, the less credit we get to roll and the less we can roll down for a credit. And as we’ve seen, if our strikes are in the money, we would have to pay a debit to roll out. Having more time allows us to sell spreads that are much further away from the money and be able to roll out and away much easier than spreads that are closer to expiration.

42-49 DTE

One last example for contrast, we will roll out a relatively short amount of time from a 42 DTE put spread.

Again, we compare rolls at different Delta values, along with the net Theta of our current position.

So, this roll is from 6 weeks to 7 weeks until duration. However, our previous observations generally hold. The peak premium is at a bit higher Delta, in the high teens. This makes sense if we consider that we are only rolling out for about 16% more time, so our new spreads will have peak Theta much closer to our old spreads. This would point to the idea that the best roll is the roll that gets us to a new spread with a short strike Delta of around 20.

Again, our max roll amount equates roughly to the daily Theta multiplied by the number of days we are rolling out.

How to Use This Information

Readers may wonder, what good is this? A trader can’t really control where prices move to, so the Delta value is not really controllable by a trader. This is somewhat true, but prices do move up and down all the time, and so if I’m looking to roll out to get to a timeframe that has less volatility, I might be able to enter a limit order that seeks to collect close to the maximum roll credit possible. Often, I’m not in a big hurry to roll, so I can check out where the maximum should be and set up an order for 90% of that amount and go about my business. If it doesn’t execute after a day or maybe even a week depending on the timeframe of the position, I could change the order to something less lucrative.

Another way to look at this data is to realize that if my position has both strikes down in the single digits of Delta, I’ll likely want to roll up my strikes when I roll out to get to optimal Theta. On the other hand, if my position has strikes with Deltas in the twenties or thirties, I may want to try to roll down and out, and hopefully still collect a credit.

If my position has gotten even closer to the money or even into the money, I’m going to have trouble rolling for a credit, and I have some tough decisions to make. I need to consider all my choices: holding, folding, or rolling. If I’m deep in the money I might consider taking desperate measures. It all comes down to risk appetite and an overall plan of action. It’s best to have a plan for all possibilities ahead of time, and not try to figure it out when times get tough.

Final Take-aways on rolling put spreads

My thought process for looking into this was to find optimal credits for rolling spreads, so I could devise strategies to improve my results. After studying this, I was excited to find an answer that makes sense. Deltas in the teens for the short strike of the spread are ideal for rolling. The further out in time the roll is as a ratio of current DTE to future DTE, the lower the delta of the current spread for best credit from the roll.

A good starting point for estimating the best credit is to take current Theta of the spread and multiply by the number of days that are being rolled out. So, if Theta is 20 cents and the roll is going out 5 days beyond the existing spread, the best credit will be around $1.00.

Finally, realize that this study was for put spreads, not call spreads, iron condors, or naked options. Spreads have unique characteristics compared to naked positions, and their behavior does not translate over. So, I only apply this information to rolling put spreads.

I am studying how naked puts best roll as well and plan to do a write up in the future on the topic.

Selling put spreads is a fairly simple trade that can generate one of the highest returns on capital of all option trades. The trade is fairly flexible to adjust for higher returns with higher risk, or more consistent, but lower returns with lower risk based on choice of duration until expiration. While I’ve written about put spreads in detail before, I recently did some additional studies to see if my earlier conclusions on best Delta values for entry were still accurate.

I’ve noticed from Google Analytics that many traders are searching for the answer to “What are the best Delta values to use for selling put spreads?” or some variation. While I think my earlier webpage on put spreads covers that fairly well, there have been enough people question me, and enough questions pop up from my own trading to cause me to go back and dig into the data a little deeper. The quick answer that I usually give to anyone on Delta values for a put spread is to sell the put strike with a 20 Delta value and buy the strike with a 13 Delta value. This optimizes position Theta, and also provides a nice, relatively high probability of profit. But is that answer true if the expiration timeframe is short, like just a few days, or really long, like several months?

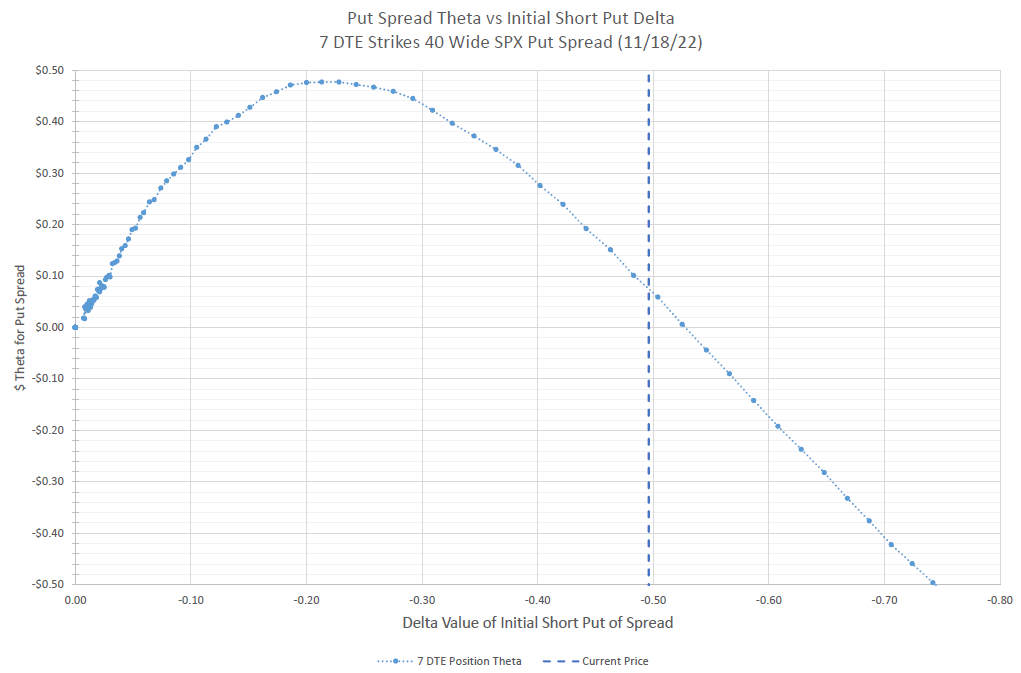

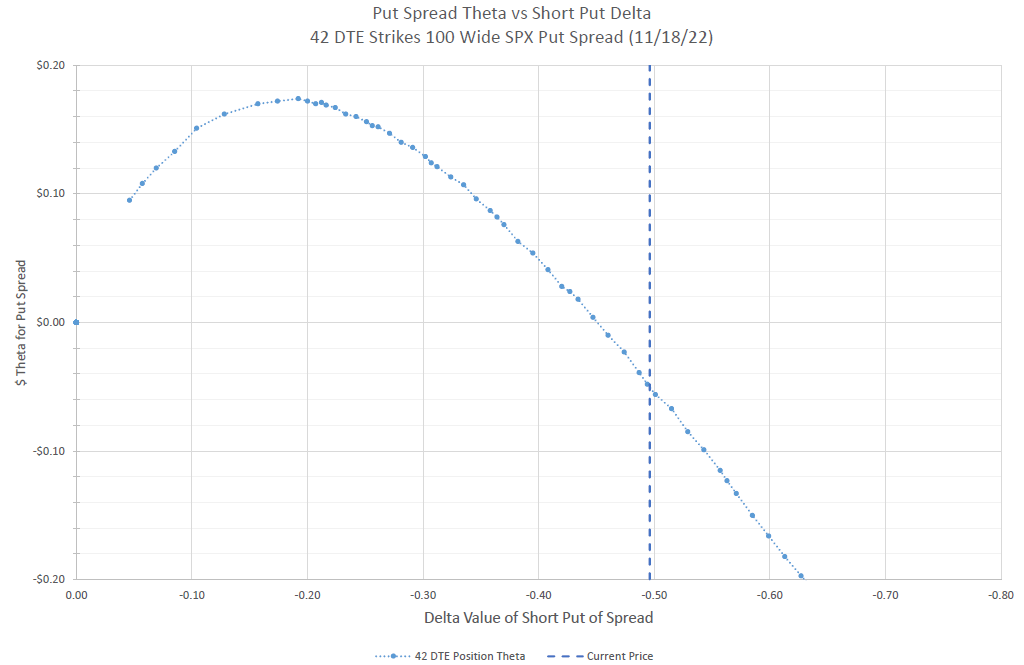

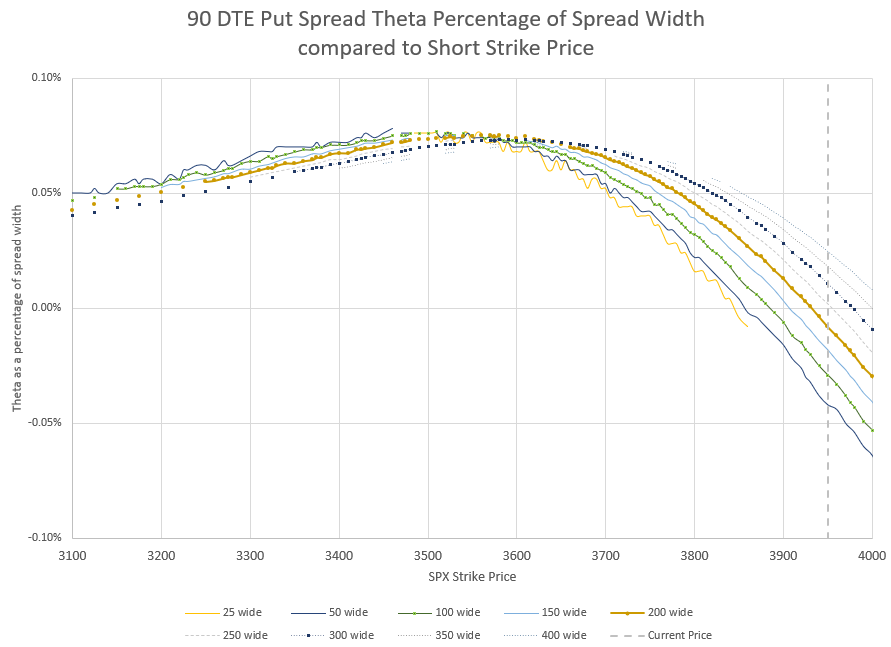

Readers likely have a hint at results from the featured chart image at the top of this post. I decided to look at all the possible Theta values of short put spreads at different strikes. For the first example, I looked at 7 days to expiration (DTE), and chose 40 point wide spreads on SPX, the S&P 500 index. SPX is generally my go to choice for options on the S&P 500, but as I wrote in another post, there are lots of different ways to trade options on the S&P 500. So, the graph shows the Theta value relative to the Delta value of the short put of the spread of all possible 40 wide put spreads, expiring 7 days from November 18, 2022. The chart shows a very smooth curve peaking around 22 Delta.

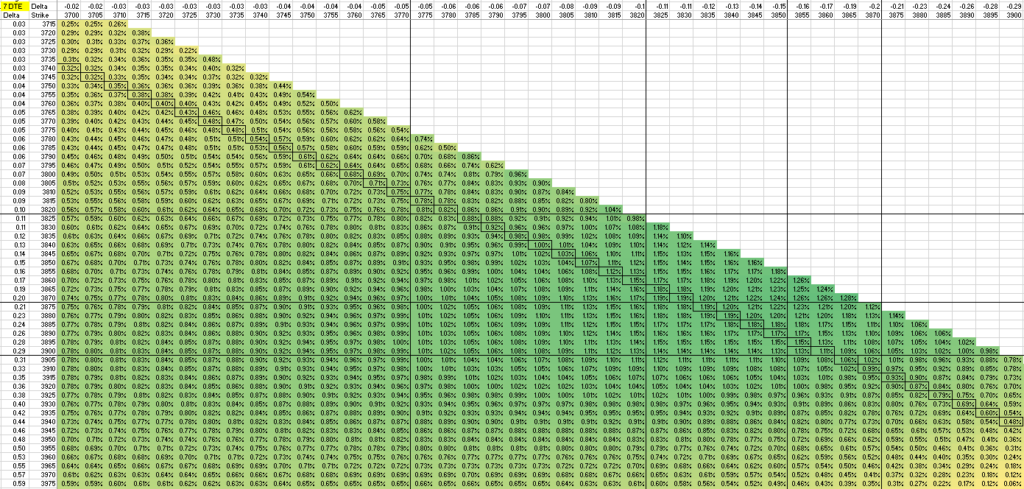

This chart shows all possible short put spread combinations around the peak Theta values as a percentage of the spread width.

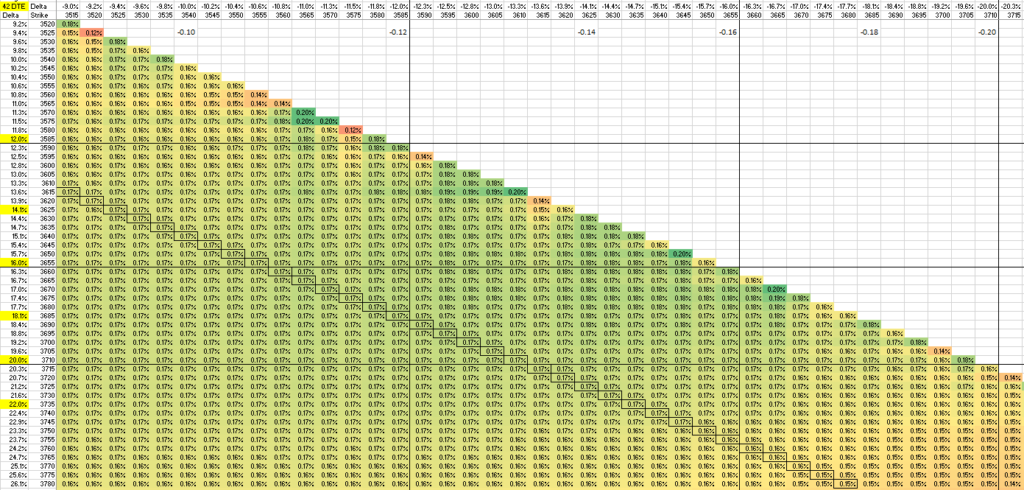

Here’s a slightly different way to look at the different Theta possibilities of 7 DTE put spreads. The horizontal axis is the long strike value, and the vertical axis is the short strike. The various values are color-coded, where the greener the cell, the higher the Theta value is as a percentage of the spread width, while yellow means lower Theta. As I’ve written elsewhere, this is one of my favorite ways to evaluate decay of a spread. I also drew boxes around all the values where the spread is 40 points wide- the points that are plotted on the earlier chart at the top of this post. If you zoom in on this green-yellow table, you can see that each cell is a percentage value, while the left and top lines show the strike prices and Delta values of each strike price. This table goes out much further than what I’m showing, but this is the part of the table where values are highest, and you can see the values are lower at the edges of this chart.

Note that delta values of between 5 and zero for the long put tend to have lower Theta values. And when the short puts get into the mid-twenties to thirty, Theta drops off. There are a number of combinations in between that have good Theta, and one could make an argument for many different ones.

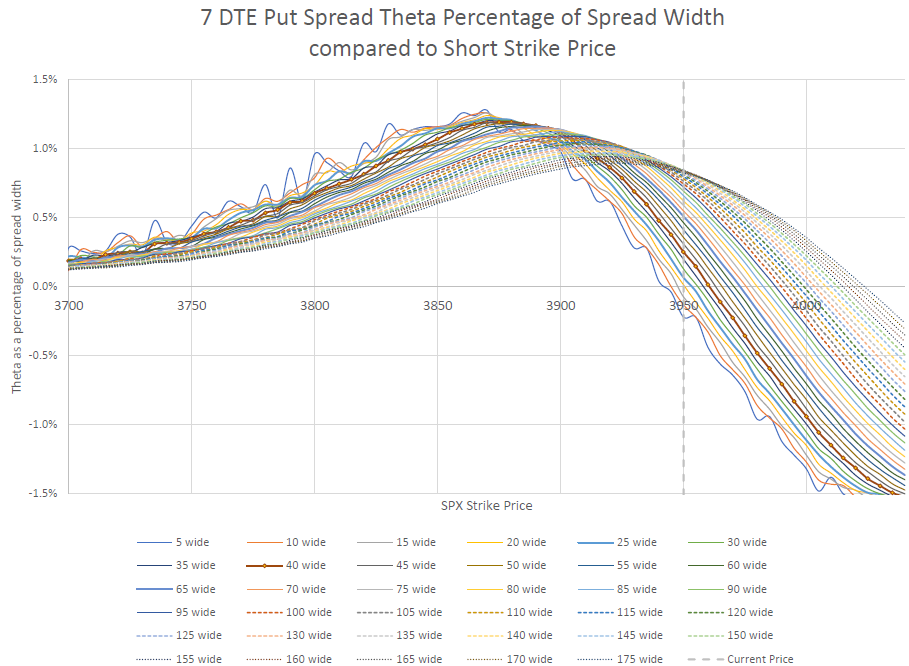

On this chart each line represents the Theta values of different spread widths at different strike prices.

One more way to look at this is to look at a graph with each line representing a different spread width. Notice that the most narrow width of 5 points has a lot of variation- this is because the Theta difference is so small, yet divided by a small width and a few nickels change in the difference in Thetas doesn’t scale smoothly. I’ve highlighted the 40 wide line that I’ve used earlier. One could argue that another line might be a better choice, but as we go wider, the peak gets closer to the current price which makes the probability of expiring in the money higher and higher.

Since the chart is made based on the short put strike, the curves move higher and higher as the spreads widen. Notice that as the spreads get wider, the peak Theta percentage gets smaller.

Longer Duration put spreads

Let’s go a little further out in time and see if the data is different. At 42 days to expiration, we get somewhat similar results.

For 42 DTE on SPX. I chose 100 wide spreads and Theta peaked right at the 20 Delta short strike.

I also did a similar thing with a table of percentage Theta values, highlighting the 100 wide spreads.

This table shows the Theta as a percentage of the spread width, and is color coded with more green meaning more Theta return. Lines on the chart mark key Delta values.

Even longer duration put spreads?

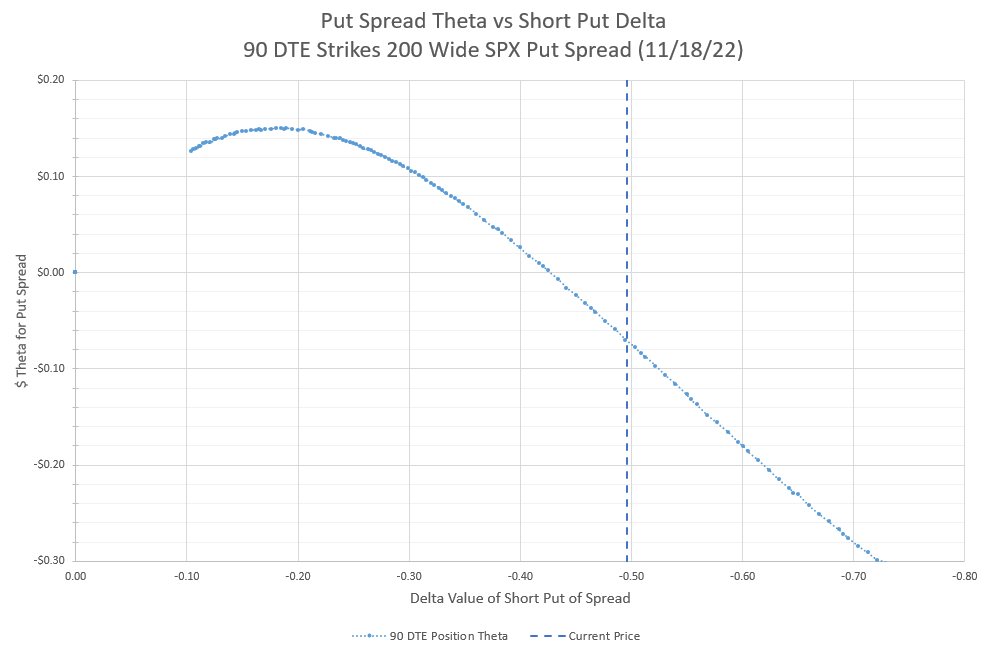

Let’s look at 90 DTE for an even longer duration.

At 90 DTE, Theta peaks out just under 20 Delta

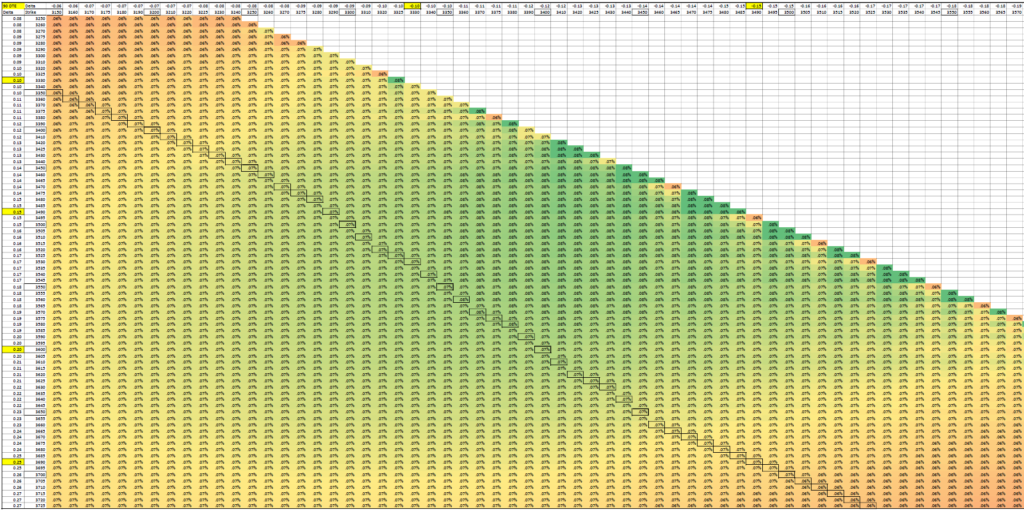

We can also look at a table of Theta values as well for 90 days to expiration.

The boxed values are 200 point wide spreads.

Again, the highest values have short strikes in the teens and low twenties for Delta. However, it probably is worth noting that the values shown are not that different between the yellow and green cells. So, maybe we should look at different spread widths to see it graphically.

Virtually all spread widths have a lot of combinations of strikes with values over 0.06% Theta per day. Compared to shorter durations, these Theta values are fairly low.

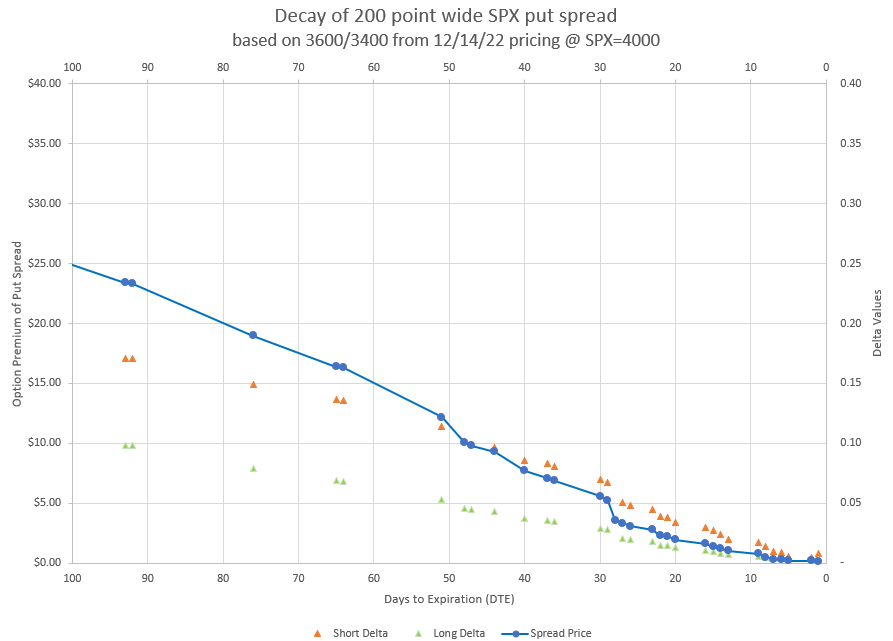

When selling spreads this far out in time, the idea is to have a large buffer from the current price and get much of the premium to decay well before expiration is even close. Let’s look at an example of how this might work.

This chart shows how the premium of a 200 point wide spread is likely to decay over 90 days, assuming no change in underlying price or volatility. The small triangles represent the Delta values of each of the strikes in the spread as time passes.

Starting with low deltas below 20, we can see that much of the decay of this spread happens well before expiration is even close. In fact, the last 20 days have virtually no premium left, which would suggest closing early and moving on. I plan to do a lot more studies on the decay curves of different spread widths and strikes to help identify the pros and cons of different entry points.

Conclusion

I think it is safe to say that the original study on spread width still stands. However, the data shows that there is some wiggle room around our old ideal of 20 Delta short and 13 Delta long strikes. We just need to be in the neighborhood. We don’t have to be exact.

Where’d the data come from?

Readers may wonder the source of the data for all these charts and tables. Actually, it’s a source that anyone can access and replicate. I simply copied an option table from my broker’s site and pasted it into Excel. Then I used a pivot table to organize the data so that it was friendly for the analysis I wanted to do. The option table had Delta and Theta values for each option contract available, and I had to use some formulas to figure out percentages of spread widths, but it wasn’t any really difficult challenge.

I do worry that my broker is changing the format of the option tables it presents, and copying every contract may be a bigger challenge in the future, but for now, I can display all contracts and select all with Control-A, then paste as text in Excel. In the future, I may have to paste a smaller amount of data each time. Readers trying to replicate these studies may face the same problem.

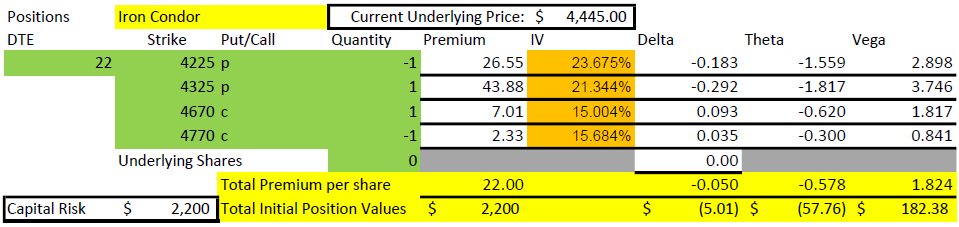

The goals of rolling are to neutralize delta, harvest profits, collect credits, and widen body width of the Iron Condor.

I see four ideal goals for executing a roll of any position, but specifically Iron Condors. First, I want to neutralize the position delta. Next, I want to harvest profits from the existing position. I also want to collect a net credit with the roll from the old position to the new. And finally, I want to improve probabilities of success by widening the body of the Iron Condor. If I can achieve all four, that’s the quadruple crown of rolling.

Often I see posts in social media lambasting rolling positions as a way to lock in losses and having no point. While that can be a possible scenario, I’d like to take a moment to discuss the ideal outcome of a roll, and share a recent example of what we are striving for with a rolling strategy.

For more information on the initial setup of Iron Condors, refer to my earlier post on the subject. This post is meant to build on that earlier post.

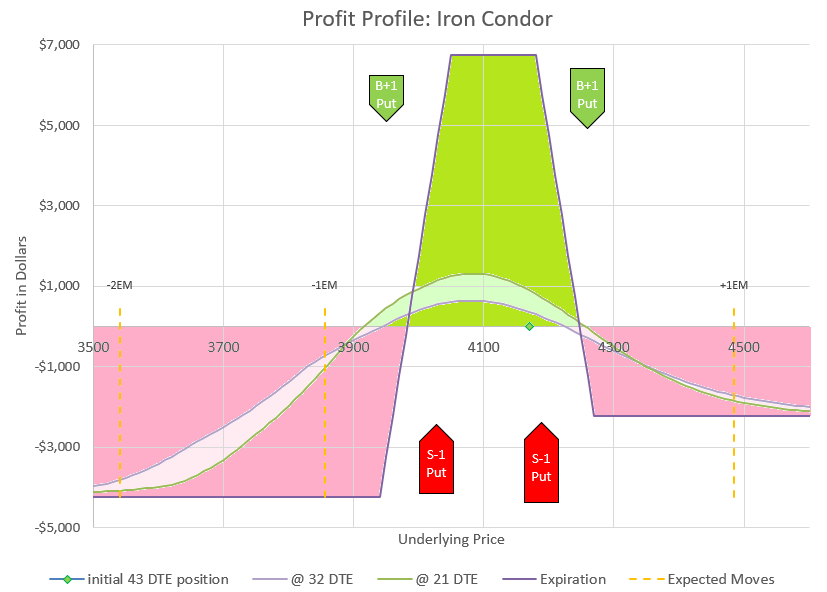

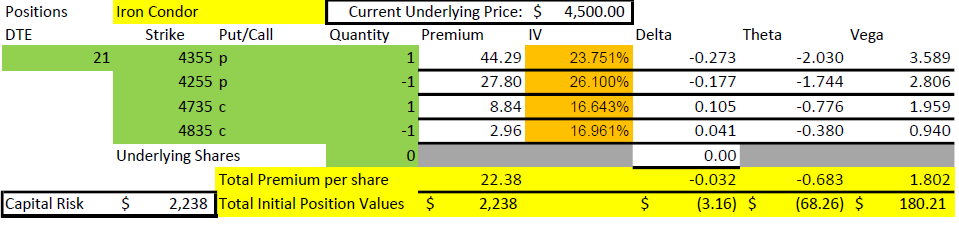

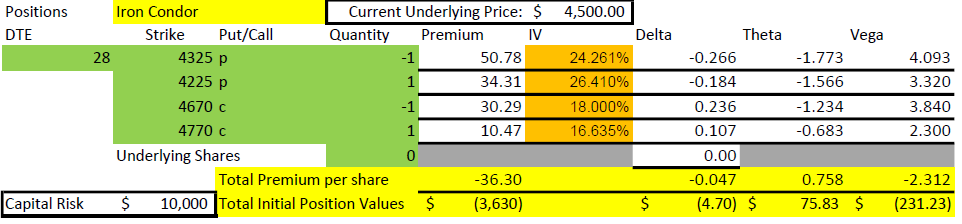

Example Iron Condor Roll

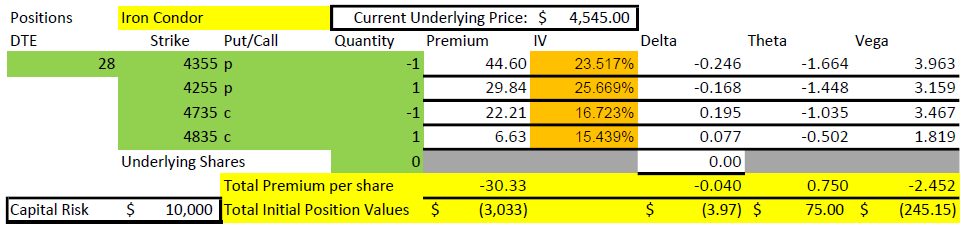

Earlier today I rolled an Iron Condor from 36 days to expiration out to 43 days to expiration. I opened the old position 10 days ago when the market was a little higher. Today, I wanted to better center my position to bring in my position Delta, and be less at risk for a move up. So, I rolled both sides up, rolling the calls up 20 points and rolling the puts up 10 points, which widened the body of the Iron Condor from 120 points to 130 points. Here is a summary of the old and new positions, with key points highlighted for further discussion.

Here is the key data from my tracking sheet for the old and new positions involved in this roll.

Let’s look at each goal and see how I did.

1. Neutralize Delta

While I don’t track Delta in my trade records, I do look at it for my open positions every day. For background on what Delta is for an option, a position, or a portfolio, see my posts on the topic. The account with this position was showing a lot of negative Delta, so I wanted to bring that in to a more neutral amount. Specifically, this position had a position Delta of -4.7, which equates to a Beta-weighted Delta of -47. This would be the equivalent of being short 47 shares of SPY. With my short call strikes slightly in the money, I wanted to reduce delta, get out of the money, and get more time. Rolling out a week accomplished all of that.

By rolling up 20 points, I got my short call out of the money. I rolled out a week, so I have more time. But most importantly, I cut my Delta almost in half from -4.7 to -2.5. I’m not zero delta or completely neutral, but it is a move in the right direction. I try not to over-adjust and chase being neutral too much or I can get whipsawed back and forth. So, now my premium value will be less volatile as the market moves up and down. Goal 1 accomplished.

2. Harvest profits from old position

The market has moved the direction I was positioned for, and today seemed like a good time to roll and recognize some profit. I’ve been in this position for 10 days, just over 20% of the life of the option. I’ve had some help from all the main pricing factors- price has moved down while I had negative Delta, time has passed while I had positive Theta, and volatility has come down slightly while I have negative Vega. All good for me. Notice that my put side lost money and my calls made money. I track them separately which helps me see trends, but the goal is for the net profit to be positive. And this position made $611 over 10 days. That’s around 8% return on capital. Goal 2 accomplished.

3. Collect a net credit from the roll

With a roll up on both sides, I had to pay a debit to roll up the calls, but I collected a bigger credit to roll up the puts. So, the net of the transaction is that I collected $0.35 per unit, or $35 overall. I try to collect credits in every roll because this is cash going into my account, while debits are cash leaving my account.

This old position wasn’t centered, and I widened the position while rolling out, factors that limited my net credit. However, I was able to find strikes that accomplished my other goals while still collecting a net credit. My new position isn’t ideal, but it is better than where I was and I got paid to make the change. Setting up a roll is an exercise in balancing many different desires, and I focus on collecting a credit as a way to determine how far I can go with my other desires. It isn’t a lot, but I collected a credit, so Goal 3 is accomplished.

4. Widen the body of the Iron Condor

The body of my Iron Condor is pretty narrow. How do I know? Look at the profit profile and it is clear that the whole position is inside of one expected move either way. Ideally, I’d like to get the expected moves inside my short strikes, but I’m managing a trade that is much tighter. So, every chance I get, I want to widen the body, the distance between the short strikes. Why do I want to do that? Because wider strikes have faster decay, up to a point, and we aren’t near that point. This position has strikes close to the money and the Theta values of the longs tend to cancel out the Theta of the short strikes more than I’d like. And the wider the distance between short strikes, the higher the probability of the price staying out of the money. Over several rolls, I want to get wider to where the position can tolerate moves without getting into the money as often. I went from 120 points between short strikes to 130 points, so Goal 4 is accomplished.

Quadruple Crown!

This roll accomplished all four of my goals for an Iron Condor roll. As I mentioned, I had to make some trade-offs along the way to accomplish all four goals, but this is an example of how I use all the data at my disposal to pick the trade that best suits the current situation.

Not every roll can be hit all four goals. If the current trade is a loser, the best you can do is meet the other three goals. Sometimes, I have to miss one goal to make another. In those cases, I choose based on what goal I’m most concerned with- do I need to neutralize delta more than I need a credit, or do I need to maintain body width more than I need a credit? Generally, I have a good shot to meet most of my goals if the current underlying price is inside the short strikes. As short strikes go deeper into the money, it becomes more and more likely that a roll will miss many of my goals.

This mindset of positive goals for trades isn’t exclusive to Iron Condors, but I thought today’s example would be a good way to illustrate the thought process involved in rolling for positive outcomes.

In the bear market of early 2022, I re-discovered a strategy that I had mostly discarded during the bull market of the preceding years, the Iron Condor. The Iron Condor is primarily a neutral trade that when managed with aggressive rolls can provide good returns in choppy, down-trending markets. My goal is to maintain a position that can tolerate fairly big market moves up or down, while benefiting from time decay.

I had discarded the Iron Condor trade because I found I was always losing on the call side of the Iron Condor. Initially, I liked the idea of making money on both sides, but I found in a constant up market, I often lost more money from calls than I made from puts. So, I switched to mainly put spreads and other short put strategies, which did great. But then 2022 came along, and it was clear that the market was no longer going up, and that we were heading for a bear market. I started adding credit call spreads to my credit put spreads to balance risk and have a neutral strategy. Over time I saw that some of my set ups and management strategies were working better than others, so I investigated and came up with a process that now works well in the current bear market environment.

The basic setup of an Iron Condor

Selling Iron Condors is an extremely common option trading strategy. The strategy is a combination of two calls and two puts, four separate options working together. Usually, an out of the money put and out of the money call are sold, and then a further out of the money put and call are purchased to define the risk and reduce cost. The trade wins at expiration if the price ends up between the short strikes, and hits max loss if the price moves beyond one of the long strikes. However, I rarely if ever hold to expiration and roll my position way before expiration is a concern.

Here is an actual California Condor with a profit curve of an Iron Condor option trade drawn over it.

An Iron Condor is named after the shape of the profit curve at expiration, which kind of looks like a condor with a bit of imagination, kind of like how star constellations are named. The iron part of the name designates that it is made up of a combination of puts and calls, as opposed to a put condor, or call condor which has four legs of the same type of contract. An example of a put condor is the broken wing put condor strategy I have described in a separate post.

To build on the condor metaphor, the difference in option strikes are often referred to as the body and wings of the combination trade. The body is the difference between the short put strike and the short call strike. The wings are difference between the call strikes or between the put strikes. The wings on the puts may be equal in width to the wings on the call, or they may be different. Wings that are different widths might be call unbalanced, or broken wings, as the profit profile will no longer be equal levels each end of the price ranges of the trade.

My preferred Iron Condor setup

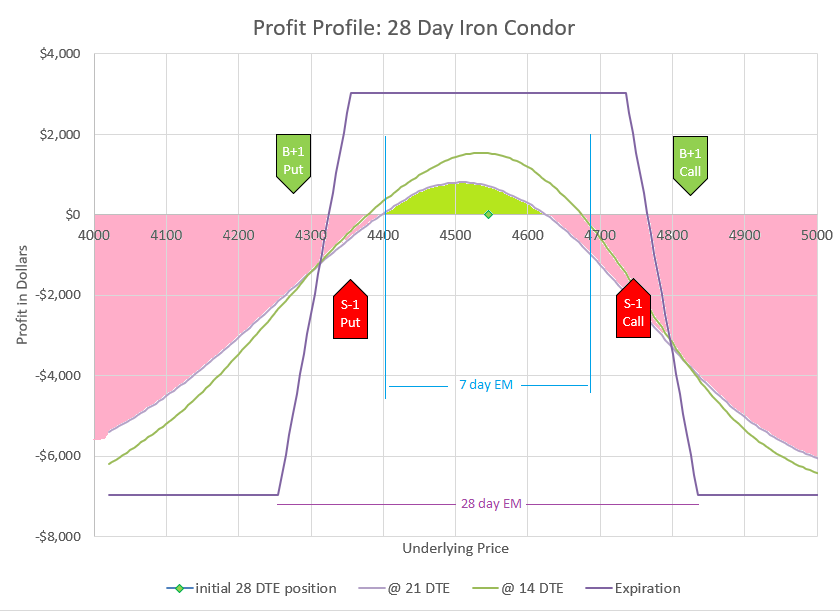

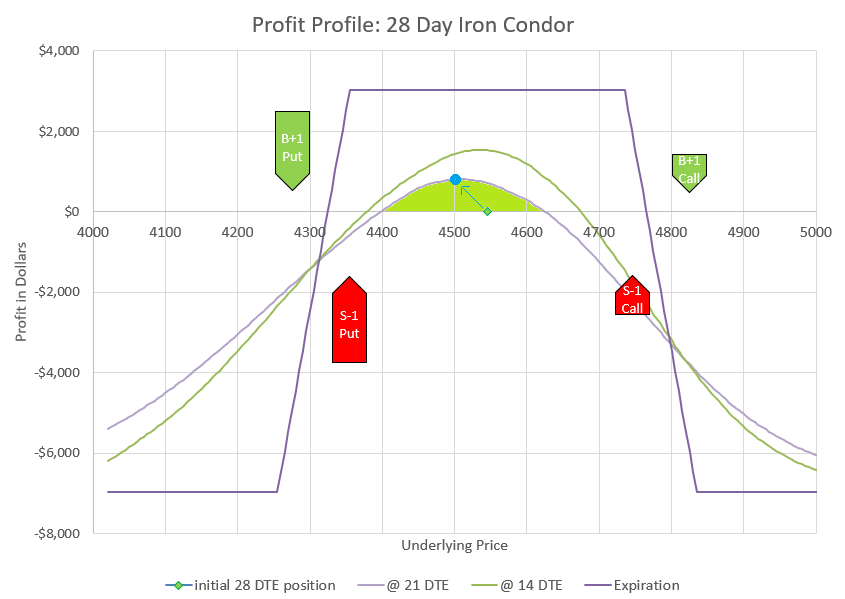

What I have determined works best for my management strategy is to use the S&P 500 index options (SPX), targeting a starting point 28-35 days from expiration, with option Delta values of 30 for the short strikes and around 20 for the long strikes. I like equal width for the put side and call side, so the Delta values for calls will be a bit wider than the put side, and the net Delta of the Iron Condor will be slightly negative. With implied volatility between 20 and 30%, I generally target 100 wide wings, with the body between the short put and short call of around 15o points on SPX.

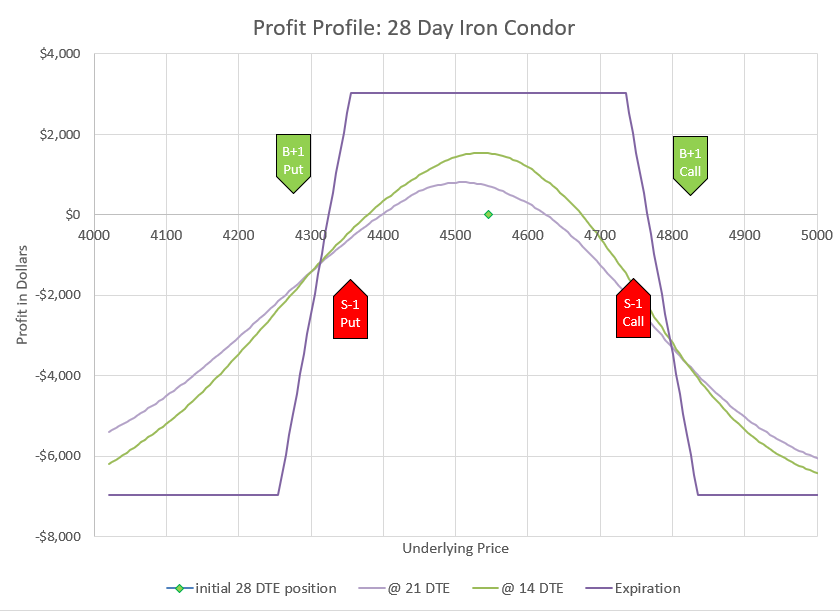

Here is the setup of an actual trade from early 2022 on SPX using the criteria from this post. In this example 30% of the wing width was collected, and a little lower deltas were used.For the above example trade, the goal is to keep in the profit zone for the first several days of the trade- the positive area under the 21 DTE curve.

I use SPX because it is the least likely underlying to have outsized moves. It is also very liquid to trade, has tax advantages in taxable accounts, and has expirations multiple times per week in the timeframes I trade. Depending on account size or type, other option products for the S&P 500 may be appropriate and can be used instead with essentially the same strategy. Other indexes or even individual stocks can be used, but managing can tougher with bigger moves, less expirations, and less liquidity.

I use 28-35 days to expiration (DTE) because my position can tolerate most reasonable moves while still having decent decay. I’ve used timeframes as low as 7 DTE, but find that many one day moves can push a position out of the profit zone, and I find myself fighting a losing battle too often. Longer durations of up to up to or over 100 DTE can work, but decay is slower, and there are very few expiration choices to roll to for the way I like to manage. All that said, my plan can vary to different timeframes, with the goal that I will only hold the position for somewhere between 1/10 and 1/5 of the time left to expiration- for example, a 30 DTE would be held 3-6 days before rolling, while a 100 DTE position would be held 10-20 days.

I choose 30 delta for short strikes and 20 delta for long strikes because they are the most forgiving in a move, while still offering reasonable decay as a spread. Higher deltas allow for more premium to be collected, and price movement will often be well tolerated as the long strike of the tested side will increase and the short strike of the untested side will decrease in value, compensating for much of the increase in value of the tested short strike. The goal of my management strategy is to keep this relationship intact, so that price movement has little impact on my option position value. I think of the area where deltas of the four options balance each other out as the profit zone. Staying in the profit zone allows Theta, or time decay, to do its work and deliver profits. I have used strikes with a bit higher delta values, but if too high, the two sides will get tested more often and then require more management. In the past, I often used lower delta spreads for safety and better percentage decay. However, I have discovered that low delta positions don’t actually tolerate price movement well because the untested side of an Iron Condor quickly runs out of premium to offset any of the movement of tested side. This observation has been a game changer for my use of Iron Condors.

I use equal width wings on the Iron Condor for a couple of reasons. Equal width seems to tolerate price movement, both up and down. Equal width also leads to a net negative Delta position, decreasing the total position profit when prices go up and increasing profit when prices go down, which is good in a bear market where downturns are frequent. Negative delta actually is somewhat neutral if the value is only slightly negative- Iron condors also have negative Vega, or decrease profit when implied volatility goes up. So, typically when prices go down, implied volatility goes up, and impacts of the negative Delta and negative Vega cancel each other out.

My Iron Condors are opening somewhere around 50% of the width of the wings. For example, if I have 100 wide wings, I would expect to collect $50 premium. I initially resisted this, thinking that the probabilities would be too low. However, since the time in the trade is so short, and I plan to actively manage moves against my position, I find that the risk reward ratio becomes favorable. However, the example trade that I’ve used is a little wider body and collected only 30% of the width.

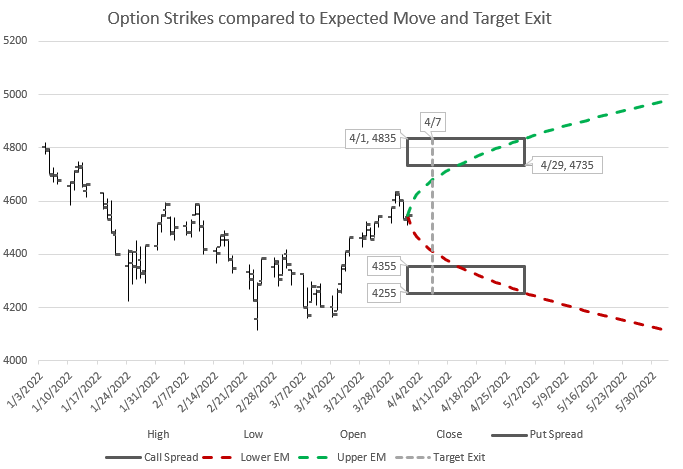

This chart shows previous market movement at the time of entering a trade, along with the expected move based on implied volatility and boxes to illustrate the strikes of the Iron Condor. The dates are the opening date, the expiration date, and the planned target date to close. This trade used long strikes that were at the expected move at expiration.

I have devised a graphic that may help to visualize this setup in regards to the expected move and time frame of the trade. The graph has several components- a historic rendering of what the index has done for the past several weeks, a curve showing the expected move for the next several weeks based on current implied volatility, and two boxes to represent the put and call strikes shown from the time of opening until expiration, and the target date to take action. My point with this chart is to show that while the strikes chosen are within the expected move at expiration, they are outside the expected move through the time I expect to be in the trade before I manage it. Said another way, if the position were held to expiration, it is very likely it would be breached on one side, but because the plan is to manage early, a breach is not likely- it would take an outsized move beyond the one standard deviation expected move.

Managing the trade with rolls

I manage my Iron Condor with what I think is a fairly unique rolling strategy. I roll my positions out in time and change all strikes in the direction that price has moved. If price goes up, I roll all the strikes up. If price goes down, I roll all the strikes down. I just roll whichever way the market goes. Here’s the interesting part- if I keep in the “profit zone,” I can roll up or down for a net credit with each roll, and my existing position will have a net profit. Usually, one side will be sitting with a profit and one side with a loss. The losing side is being tested- its strikes have higher deltas than when the trade started. The profitable side will have lower deltas than when the trade started. My profitable side should have a bigger profit than the loss of losing side. When I roll, I will likely have to pay a debit to get my losing tested side back to a good set of strikes at the new expiration. However, I should be able to collect a bigger credit on the profitable untested side than my tested side cost. Ideally, every roll is closing a profitable trade and collecting a net credit to open its replacement. All of this sounds great, too good to be true, but there are a number of details to unpack.

The first challenge is to stay in the profit zone. My general rule is that if I keep my untested short strike must never drop to a Delta value below 15. The reason is that when the Delta of the untested side gets below this point, it quickly stops being able to meaningfully contribute to offsetting price movement in the tested direction. For example, if the price drops, the short call will get further out of the money and drop in value, while the puts will go up in value. For a while the Deltas will mostly balance each other out, but as the Delta of the short call drops below 15, the put spread will start increasing much faster and the calls decreasing less. If this happens, it is time to act and roll all the puts and all the calls down to where there is again premium on both the put and call side. If price has gone up too much, it’s time to roll up all the puts and calls.

Actually, I try not to wait until the untested side gets to 15. I think of my position of having three possible states, green, yellow, or red. Green is when both short strike’s Deltas are above 20- everything is great and there is nothing to do. Yellow is caution, one of the short strikes are between 20 and 15, and probably will need to roll soon. Red is stop and take action, one of the short strikes is 15 or below, so it is time to roll immediately. So, my choice is clear for Green or Red, but I need to use some judgement in the Yellow state. If the day starts in the Yellow, I am more likely to let it ride for a while and watch to see if it recovers or gets worse. If the market has trended throughout the day and moved into the Yellow, I am likely to roll before the end of trading so I don’t end up deep in the Red overnight. If there is a strong trend pulling the position quickly toward Red, that may also be a good indication to act. Yellow is a judgement call.

I find that it is harder to have a profitable, credit roll when tested on a quick up movement. As mentioned earlier, equal width wings means that there will be a negative delta overall, and while volatility reduction can help, big up moves can be hard to stay on top of. That’s why this strategy works best in a bear environment, when the market is trending down.

Don’t over manage. Markets bounce around a lot, and it can be tempting to want to act on each little trend that happens. If I have the right strikes- the right body width and wing width for the market conditions, my position should be able to tolerate price movement. If I’m trading at 30 DTE, I want to wait 3-6 days between rolls, so I need to be choiceful about not rolling too often. If the market moves a huge amount in a couple of days, I may need to roll early, but then I’ll want to try to go longer before the next roll. The other thing to consider is that often the markets overshoot in one direction or the other, so I try not to move too far to chase moves that go on for days, and stay patient that the market will counter the trend.

If a position isn’t winning regularly and isn’t holding its premium in control, that’s a sign that the strikes aren’t right for the market and the duration. For a while I was trading 7 DTE Iron Condors on SPX with around 100 wide bodies and 50 wide wings. I would adjust nearly every day, but I couldn’t keep the position in the profit zone, and I often took losses. There wasn’t enough space in the body and the wings weren’t helping enough. By widening out the body and wings and adding more time, I found the position much easier to manage, and more likely to be profitable, and much less likely to take a big loss.

One way I can tell if I have a forgiving position is to compare my premium to the premium of the same position a few strikes higher or lower. For example, with Schwab StreetSmart Edge, I can pick Iron Condor as a strategy, pick an expiration date, pick a body width and a wing width. The application will then give me a list of strike combinations and premiums for those parameters. If all the choices around my preferred strikes have similar premium, then I know that price movement will have minimal impact on my chosen position. If there is a rapid change in premium for other strikes above or below my choice, it means my Iron Condor parameters are not very forgiving, and I should adjust time or widths or both. Other brokers will have similar ways to compare prices by shifting up or down all the strikes.

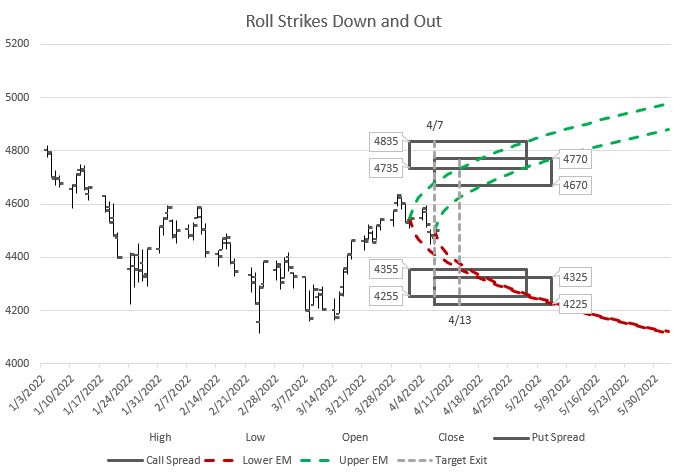

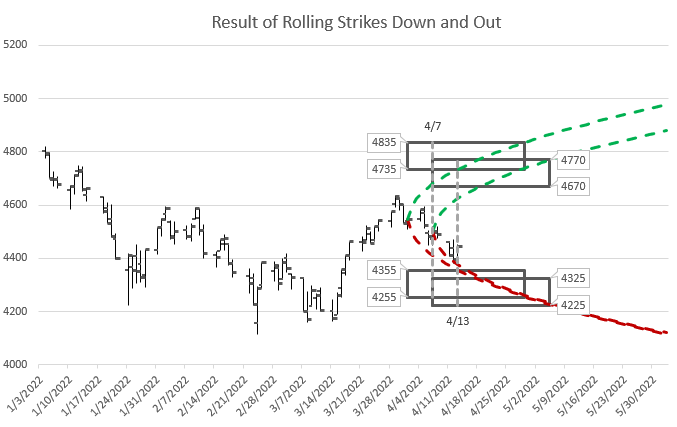

I have updated the earlier graphic to illustrate how a change in price over time will dictate the choice of a new position to roll to. The new price now dictates a new expected move, and new ideal strikes and expirations. Hopefully, this chart will help those that are fond of graphical illustrations.

After 7 days of mostly down moves, I decided to roll down my positions and roll out to a later expiration. In this image, the old position and expected move are there along with an updated expected move and new strikes.

Eight legs in the Roll

Since an Iron Condor has four legs, rolling involves closing four legs and opening four new ones. I don’t think any broker or exchange allows a eight-legged trade, so at a minimum this will take two trades to complete the roll. My preference is to roll the puts as a trade, and roll the calls as a trade. I usually start with the side that is being tested and might need a debit to roll to a new expiration and strikes. Then I do the other side, usually moving the same amount and keeping the same width, expecting to collect more to roll the untested side than I pay to roll the tested side.

At times, I may have a situation where I don’t have enough buying power to roll one side while the other side remains in place. If that happens, I’m probably using more of my buying power than I should, or the position is just too big for my account. It isn’t that big of a deal to manage the situation, however, I just close the untested side out and roll the tested side, then open a new position on the untested side. Worst case scenario, I can close the whole Iron Condor at once- freeing up its buying power, and then open a new one with the same buying power. As long as the wing widths are the same and the new Iron Condor collects more to open than the old Iron Condor cost to close, there should be a net gain in buying power. But again, any time buying power restricts a trade, it is probably time to pare down some positions in the account.

How Iron Condors tolerate price movement

Probably the best way to explain how an Iron Condor tolerates price movement is with an example. Earlier in this post I showed an opening trade from April 1, 2022. Let’s look at it again and look at how it fared after 7 days.

Here is the setup of an actual trade from early 2022 on SPX using the criteria from this post.

Notice that the premium collected is approximately $15 each on the put side and the call side.

After a week, price has dropped to 4500, but the premium has dropped for a profit.

The premium on the put side has gone up to around 16.50, while the call side has dropped to just under $6.

After 7 days the premium increased on the put side but decreased on the call side, as illustrated by the larger and smaller strike position arrows, and the result is a net profit.

So, after 7 days, the trade made about $800 on $10,000 risk, an 8% return. But, that’s just the start- the plan is to roll, and so the closing trade above was combined with the following opening trade:

On April 7, this trade was opened while closing the old position for a net credit and strikes that are back at the edge of the expiration expected move.

The combination of closing the old trade and opening the new trade is a net credit of just under $14 premium. This is the result we are looking for- a profit on the trade being closed, and a credit to move out in time and get to better strikes for the latest situation.

And just to finish the example trade, let’s look out another week and see what happened to the market and the trade that was rolled to.

After rolling down, the market kept going down, but stayed within the new strikes with plenty of space to spare.

By April 13, the market had dropped even further, approaching where the puts from the original position had been. However, the roll down gave the new position plenty of space and the trade was sitting at a profit, and ready to roll again.

After 6 days, the rolled position had decayed even after a market move. Again, puts lost money, but the calls made the position profitable.

This trade made $1430 in 6 days, a 14% return on capital. Since the market went down, the put side of this trade lost money, although not that much since the price didn’t end up that close to the put strikes since our new strikes were lower than the old ones. Time decay helped counter the price movement against the puts. The money was made on the call side through both price movement and time decay. In the end time decay, represented by Theta, eats away premium as long as price doesn’t get too close to the strikes.

These are examples of trades I did during the Spring of 2022 in the face of a bear market. Not every trade faired this well. Some market moves were too fast and too far for me to be able to roll before the position went too far to one side. But more often than not, this rolling methodology has kept me from having positions blown out, and keeps day to day portfolio value from varying out of control.

You may notice that the example trades shown here don’t exactly follow all the mechanics I’ve described. Since those trades I’ve become a little more likely to intervene early, although it’s a balance with avoiding over-adjusting.

Finally, I don’t always get my rolled positions re-centered, like I did in the example I presented here. Often, I’m happy to just move in the direction of the market and make sure my new strikes are a bit out of the money on the tested side. In this crazy bouncy market, we get lots of reversals, so I let my positions stay a little off when the market has moved a long way and technical indicators suggest the last several days move may be about finished. However, these choices come down to individual trader preference and market outlook. No one knows what is happening tomorrow or next week, so we each have to decide what trade is best based on the information available. For a real life example of this type of decision making in action, see my post on the Goals of Rolling an Iron Condor.

I’ve used my go to option strategies of credit put spreads, complementary back ratio call spreads, and using call spreads to cover calls to take advantage of the reversal from the mid-March lows

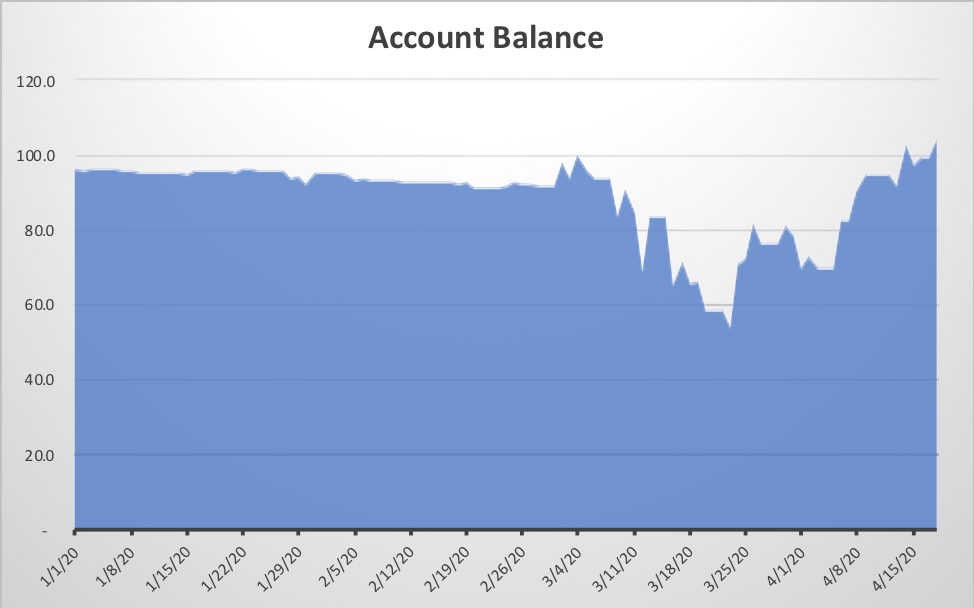

What a difference four weeks can make. From the end of February until March 23, my account dropped over 45% in value, worse than the stock market. However, since March 23 the account has gained back all of the loss and then some, a much better performance than the overall market. At the end of the day Friday, my account was up around 9% for the year, and up 4% from the high value at the end of February. All this from an account of mostly short option spreads, specifically credit put spreads. What happened, and what can be learned?

I’ve used my go to option strategies of credit put spreads, complementary back ratio call spreads, and using call spreads to cover calls to take advantage of the reversal from the mid-March lows. It’s been a fight every day, and a different approach than normal, but the positions are working.

Lots of mistakes on the way down

I made a number of strategic errors along the way that accelerated my losses. For months preceding the COVID crash, I maintained a negative Delta position in my portfolio as the market moved up to new highs seemingly every day. I watched my short calls go deeper and deeper into the money, while I sold puts just below or at the strikes of my short calls for lower and lower Delta values. I took some losses and reset my positions with more neutral to positive Deltas to go with the run up as the new year started. As the news of the coronavirus started hitting the news from China in late January, I scrambled and went negative Delta on a down day, which backfired when the market proved resilient after a one week drop. I discussed this error in a previous post. The market went on to hit new highs in mid-February and I held my own, moving to a positive Delta as it appeared that the coronavirus would not be that big of a deal. I even let a large group of underwater short call spreads be assigned for a big loss after many earlier rolls had kept hopes alive for getting my money back if the market went down.

The following Monday, the market started making big drops down. Initially, this worked out okay. I still had a number of short call spreads deep in the money that benefitted from the initial drop. But at strikes just below these call spreads were short put spreads that started growing big negative values. I had sold these to collect premium to offset the rolls I did to the call spreads, thinking that they would never approach being in the money.

In the early weeks of March I was worried that a whipsaw up would drive my call spreads back negative, so I bought the call spreads back when they reached 25% of the width of the spread, a nice improvement from values of over 90% of the width of the spread, but a loss compared to selling them originally for 15-20% of the width of the spread. Meanwhile, I let the put spreads keep going deeper into the money. I even sold some additional put spreads at what seemed like high volatility and low Deltas, only to see them get swamped a few days later when the market dropped 5-10% multiple days in a row. By this time, whatever the market lost, I lost double. One day the market went down 10% and I lost 20% of my account- in one day! Those were hard days to keep a positive attitude.

The data that kept me going

I never really considered cashing out to stop the losses. If anything, I knew that getting out would simply lock in the losses I had in my account. The losses were paper losses- once the position is closed, the loss or gain is real. That doesn’t mean that there is any guarantee that a paper loss will reverse- in fact, the raw option probabilities at the time suggested otherwise. But other data gave hope for better days.

Volatility is mean reverting. When volatility is at historic highs, it is likely to come down sooner than later. At its peak, the VIX was just over 80, implying an 80% move in the S&P 500 in the following year, based on option prices. Normal VIX values are around 18. It will take time to get back to normal values, but values in the 50s, 60s, and 70s are unsustainable. The way the VIX comes down is for the market to go up. The only question was when it would turn around.

The VIX almost always overstates what future moves will be. And volatility skew drives put premiums to high prices in all market environments, but especially in times of high volatility. The only time that owning puts makes money is while the market is dropping quickly, and that is the only time that being short in puts loses. My position lost money due to both changes in underlying prices that moved my put strikes into the money, but also due to increased volatility that made the premium go up. Knowing that these premiums were unsustainable, I felt comfortable that I would get my put premium back if I could hold on long enough.

The options I sell are typically 5 to 8 weeks out from expiration. That gives me time to wait for a reversal, time to adjust positions without panic. Normally, I close positions 2-3 weeks prior to expiration, but conditions will sometimes drive me to either act earlier, or go closer to expiration. The key is that having time gives me choices. Normally, I look at time decay as my primary consideration for how I manage my positions. During this crash and partial recovery, price movement was my main concern. In Greek terms, Delta (price movement) was the primary concern, while Theta (time decay) and even Vega (volatility changes) took minor roles.

All of these factors have been drilled into my head from watching and studying the research of the great folks at TastyTrade.com. They have presented numerous studies that show how market downturns are opportunities for those who can take advantage. Of course, you have to have capital to really take advantage, and I was pretty tapped out by the time we hit bottom.

I have my own approach, and I also build a variety of models and studies to help guide my strategies. I’ve never been comfortable with undefined risk strategies, the use of naked options. This recent period has re-inforced that point of view. My research has focused on how to use spreads to define risk, but also provide a profitable rate of return. Spreads behave differently than naked options, and require different strategies. Ideally, I get the majority of my profit from far out of the money credit put spreads. On the other hand, I mostly sell calls as part of a back ratio spread, because I’ve found credit call spreads to be problematic due to long periods of market up movement.

My recent winning approach

As we approached the bottom on March 23rd, I closed the remaining credit call spreads in my portfolio. My sense was that we were getting to a point where upside risk was greater than downside risk, and I didn’t want to lose on the way back up.

1. Rolling the credit put spreads

With the market down 20-30%, I had many credit put spreads that were deep in the money with strike prices as much as 20% above the underlying price at the time. I figured that if I could move the spreads even half way closer to the current trading price, I’d have much better odds of getting some or all of my money back. On the worst down days, I rolled my put spreads down, either widening the spread, or paying to be closer. This meant rolling short puts with Deltas of 90 or more and moving them to around 70 Delta. Many of these moves paid off big within a week of the move when we had a 10% move up of the market in a day. I used up days to roll out put spreads that were at the money or slightly out to later expirations, collecting premium and giving myself more time. I wrote a separate post on this strategy a few weeks ago.

2. Adding delta neutral back ratio call spreads

I generally take both sides of the option spectrum in my trades. I sell puts and calls on the same underlying at the same expiration. I use the same amount at risk capital on each side. As I got rid of my call spreads and rolled my credit put spreads down, I wanted to double-dip with calls, but without the risk of getting beat up with a whipsaw move up. If I sold credit call spreads, I feared that big up moves would drive these new call spreads into big losses. I didn’t want to lose on both the way down and on the way back up. So, I used back ratio spreads instead. The way I set these up is I find call strikes that have the same width as my put spread, and have Delta values where higher strike is half the Delta of the lower strike. I sell the higher Delta call and buy TWO of the lower Delta calls. The call position is Delta neutral and takes on no additional capital risk, because I use the same width as the put spread I already have. For example, I may sell a 30 Delta call and buy two 15 Delta calls. If my puts are out of the money, I may even sell calls in the money, for example sell a 60 Delta call and buy two 30 Delta calls. I collect a premium, which I keep if the strikes end up out of the money. If the underlying goes up, I make money from owning twice as many calls as I sold. For more details, read a further explanation on my web page on back ratio spreads.

I do have some long stock positions where I have sold covered calls in the past. Most of those calls have gone deep in the money a long time ago, and I rolled them periodically to collect a small premium. The recent COVID crash gave me an opportunity to finally get out of these positions and reset for a turnaround. Even out of the money, these positions still had a lot of time value due to volatility being at high levels. As I looked at each position, I generally did one of two non-traditional things- I sold a credit call spread, or even a back ratio spread in a later expiration. What this means is that while I still sold a call on my position, I used some of the proceeds to buy higher strike calls. By doing this, I have choices if prices go up substantially, but I’ll still keep premium if prices go down or stay flat. The back ratio spreads have the potential to create additional profit, with two long calls outgaining one short call, on top of the return from the underlying shares that are being covered. There are some minor downsides to this, but in a period where price movement is the key consideration, back ratio spreads are a great use of calls, even when covering long shares of stock.

How it worked out

From late March through the middle of April, the market has gone back and forth, up and down, with more up days than down. The market is up substantially from its low on March 23, but still well below the highs reached in late February. My positions have taken advantage of these moves.

My put spreads get more and more healthy as the market moves up. Almost all of them are now out of the money, although I still have a few under water. I’m rolling them out as they approach 21 days to expiration, and only for a credit. I actually rolled up a put spread that had gotten too far out of the money- the short strike had a Delta in the single digits, so I reset the spread to a 19/13 Delta because expiration was still 35 days away. I now use down days to open put spreads with slightly higher volatility. It feels more like normal times.

The call back ratio spreads have generally worked out great. They benefit from big price swings, but are vulnerable to decreases in volatility. They work best with long expirations- 4 to 10 weeks, so I’m pushing my expirations out to accommodate them. I also adjust them frequently, rolling up when the market goes up and rolling down when the market goes down. I collect premium both ways, moving to Delta neutral each time. In a declining volatility environment and an up and down market nearly every day, collecting additional premium keeps me ahead of Theta and Vega decay.

I do have a few regular credit call spreads where the width of my put spreads were too small for a corresponding back ratio call spread. These are my new problem positions because the big up moves have put some of them in the money. I’m determined to fight these, and one by one, I’m converting them into back ratio spreads or closing them before they get out of control. I’m also only opening new put spreads that have a width that a optimal back ratio call spread can match.

Of the upswing back, I’d say that 50% of the gains have come from put spreads getting out of the money, 25% from my long stock/ETF shares, and 25% from call strategies.

Looking ahead

Now that my portfolio is getting closer to my normal strategies, I’m starting to pay attention to Theta values and work toward a more neutral Delta position. I’m still negative Theta because of how many long calls are in my back ratio call spreads, but I’m working these down by going to strikes further out of the money where Theta is more in decline. The underwater put spreads also have negative Theta, which should reverse when they get out of the money. I’m still long Delta, but my call positions are slightly negative. As my puts get more out of the money, Delta will go down. I’m also working to free up capital, so I can have funds to jump in if volatility spikes back up.

Conclusion

While I’m not happy with how I got into this mess, I’m feeling quite fortunate to have beaten the market back to positive for the year. The challenge is to keep up the positive momentum.

Earlier this week, I decided to go all in on adjusting the Delta of my option portfolio. Monday, to be specific, I moved from a somewhat positive portfolio Delta to a very negative portfolio Delta. In hindsight, this was a bad move for a variety of reasons, and I thought it was worth writing a post to share.

Background

For those of you new to option Greeks, Delta is the option parameter that measures how much a underlying security price change will change the price of the option. If a stock goes up $1, how much will the option price change? For every position in your portfolio, you can measure this impact, and with a little math, you can figure this out for your whole portfolio. The key is to price weight the Delta values so that different priced stocks and ETFs are weighted proportionally to their impact on the portfolio. There is a whole section on Greeks on this site that goes into the particulars if you need more information. There is also an overview of Delta included. However, it isn’t necessary for you to fully grasp all the theory to understand the point of this post.

Before my changes, my portfolio moved about half the amount on a percentage basis as the market moved in the same direction- if the market went up 1%, my portfolio went up 0.5%. After the change, my portfolio moves two times the market in the opposite direction- if the market goes down 1%, my portfolio goes up 2%.

Why did I do this, you might ask? Well, the market has gone nowhere but up for the past three months, and is due for a reversal. It is up so much that I saw in the weekend Barrons publication that one indicator says we reached “Euphoria” levels this past week, which says we are likely to be lower a year from now. Also, the coronavirus was in the news and could have a big impact on the global economy. Last week the market was down for the first time in three months, and we had all four days close at a loss. (The market was closed Monday for MLK day.)

Over the weekend, I decided I was positioned the wrong way- my portfolio was positive Delta and all indications were that the market was going down. And Monday, the market opened way down, over a percent and a half lower than the close on Friday. My portfolio showed a loss of just under 1% for the day. If this is what we are going to see for the next several weeks, I needed to get positioned to profit.

If you aren’t familiar with my approach to option trading, I’m a big proponent of defined risk credit positions. In other words I sell options spreads for a premium and then expect them to decay in value so I can buy the spreads back for much less than I sold them for. I sell both put spreads and call spreads, often on the same underlying security on the same expiration, an Iron Condor. Typically, I try to be Delta neutral (price neutral), so I benefit whether the market goes up or down, but mainly when it doesn’t move very far in either direction. But for three months the market has gone up- a bunch! The call spreads of my Iron Condor were getting breached and were losing money. It is no fun to lose money when the market is going up.

To adjust for the very bullish market, I’ve started selling many more put spreads and call back spreads for the last month or so. I stopped opening new Iron Condor positions. I have several put spreads without calls. These positions benefit when the market goes up more than when the market goes down. The Delta value of these new positions are all positive. That was working well with the market climbing almost every day, and profits were rolling in. Then last week the market turned….

Monday’s adjustment

So, what did I do? Since my read was that the market was at the beginning of a downturn, I wanted to reverse how my options behaved. I went through my positions and closed out every put spread that is expiring in the next four weeks. If I had opened them several weeks ago, I could close them at a profit. However, if they were recently added, I had to take a loss, especially on Monday with the market down, when puts are more expensive.

I also converted many of my call backspreads to simple credit call spreads. If you aren’t familiar, a call backspread is when you sell one call and buy two calls further out of the money. I often buy the two calls at just less than half the Delta of the call I sold, and can collect a credit. If the market goes up a lot, the two calls I bought become worth more than the call I sold. But if the market goes down, the long calls quickly drop in value. On several backspreads I had, I sold one of the long calls that I had bought. I took a loss on each of them, but I thought they were going to soon be worthless with the market going down, so it made sense to sell. The remaining spread of one short call and one long call could then decay in my favor when the market tanks.

Why do I think this was wrong?

Tuesday, the market went up 1%, and I lost a little over 2%, because of the changes I made. So, I lost on an down day on Monday because I had positive Delta, and I lost on an up day on Tuesday because I then had negative Delta.

I still think we are likely to see a down market over the next month, and I think my position will eventually benefit. But, my approach to adjusting was wrong on several fronts. Generally, my timing was terrible and the magnitude of the change was too much at once. Here are the key principles I violated.

I closed into weakness and not into strength.

I made too big of an adjustment at once.

I should have known the odds were against me on Monday.

I didn’t pay attention to how much Delta I reduced

Let’s take these one by one.

Closing into weakness

Everyone knows that the goal of trading anything is to “Buy Low and Sell High.” For an option seller, it is actually to “Sell High and Buy Back Low,” but the idea is the same. When you have a short put position (or a credit put spread), the best time to buy it back is on a day when the market is up and it is less valuable. In a choppy market with the market up one day and down the next, picking the right day to open and close positions makes a big difference.

The same is true of selling a long call position- sell calls on an up day when the call is most valuable.

Not only was the market down the day that I closed my short puts and long calls, it was down the largest amount that it had dropped in three months! A terrible day to make this change. I paid way too much for my puts, and I received way too little for my calls.

Too big of an adjustment at once

As I already said, I think the market is still headed down over the next several weeks and I think negative Delta will do well. However, I might be wrong, and I pride myself on avoiding big directional bets.

I moved to a portfolio Delta that is negative twice the value of my portfolio. If your broker provides a SPY-weighted Delta measure, you can see this by multiplying your SPY weighted Delta times the value of a share of the SPY ETF. As an example, if you have a SPY-weighted Delta of -100, it is equivalent to being short 100 shares of SPY. At today’s SPY price of $327 per share, the portfolio will behave like negative $32,700 of SPY shares. If your portfolio had a dollar value of $16,000, you would lose 2% if the market went up 1%. That’s essentially my new position.

So, what would have been a better approach? Well, if I was absolutely determined to adjust my portfolio Delta on a down day, I could have adjusted just until my Delta was zero. Then, when there was an up day in the market, I could have adjusted into negative delta territory.

In any case, moving from a Delta value that is 0.5x my portfolio value to one that is -2x is too far, too fast. I’ll be looking for a chance to work myself back closer to Delta neutral in coming days, even if I stay with negative Delta.

Odds were against me

There were at least two predictors that I should have paid attention to on Monday before making the changes I did. I should have known that it was very likely the market would go up on Tuesday, making Tuesday a much better day to adjust than Monday. As it turned out, the market was up 1% Tuesday, the largest up move in three months.

How would I have predicted this? The first reason is a bit weak, but often true market myth- Tuesdays generally bounce the opposite direction of Monday. This is the kind of story that I tend to doubt, but many market veterans quote it every time it happens. For me, it is one piece of information to consider, but especially after a big move on Monday.

The second reason is more data-based. The most losing days in a row we have had in the past 20 years is six. It has happened only a few times, but we have not had seven losing days in a row in the past 20 years. How do I know this? Tasty Trade did a study on this last year and it stuck with me. You can see it yourself in this segment on Fading Market Moves. Monday was the fifth losing day in a row. It is very rare for there to be six losing days in a row, so the end was in sight and I attacked too soon.

There are other reasons to reconsider timing, especially on down days. We generally have more up days than down, so unless the situation is critical, there is usually a better time to reduce your bullish position than on the biggest down day in months.

If the opposite situation were true, I’d feel a little different. The market can have very long winning streaks, and you really can’t wait for a down period to fix a bearish situation.

Not knowing the number