Buy stock at a big discount? This strategy is often referred to as stock replacement. We buy calls, have the same upside as shares of stock but at a fraction of the cost. Look for two things: relatively high probability and low Theta decay.

Want to buy stock at a big discount? This strategy is one that is often referred to as stock replacement. With this strategy, we can buy options that have the same upside as shares of stock but at a fraction of the cost. In theory any time someone buys a call, there is the same upside as stock, but some setups give a trader more of the upside benefit than others.

When I think of using options in place of stock, I’m looking for two things, relatively high probability and low Theta decay. When buying a option with no hedge, the natural way to lower time decay is to buy a call well out in time where it will decay slowly. To get it to move with the underlying stock, having an in-the-money option can get most of the move up (or down).

So for this strategy, I look for options 6-12 months out with a Delta value of 75-80. These options will likely cost 10-20% of the cost of the shares as they have significant intrinsic and extrinsic value. With over 6 months until expiration, time decay is slow, but still present.

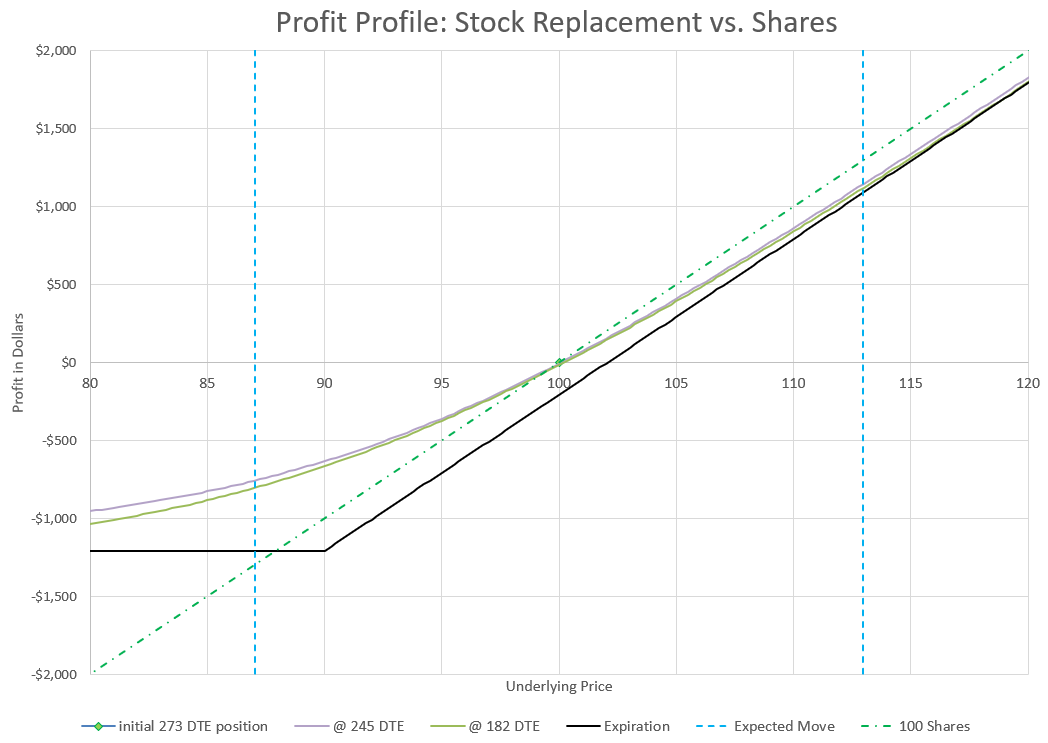

In this example, a call is purchased with 9 months (273 days) until expiration with a Delta of 0.78. Notice that even after a month or even three months, the profit curve is very close to that of owning stock around the money. Notice that the downside is significantly less than stock.

Because I’m buying an option with a Delta of 75-80, I have the equivalent of 75-80 shares of stock from a price movement stand-point. If the price goes up, over time the Delta will increase and the option will behave closer and closer to the movement of 100 shares of stock.

The risk to the downside is limited to the amount paid for the options, so a big market drop could wipe out the position, but even a big drop would still likely hold some value, but mostly the extrinsic time value. However, the really good news is that losses in the options on a downturn are less than the losses that would come from 100 shares of stock.

My goal in this trade is not to hold until expiration, but to either exit or roll to a longer duration before we get into the last quarter before expiration. If the stock price has gone up, I can roll to a new time at a higher strike price and collect the amount the stock has appreciated less the time decay that was lost.

This trade needs a small move up to break even, so the theoretical probability of profit is a little less than 50%. But, by getting out way before expiration, the odds get ever closer to 50/50, and in a bull market the unlimited upside with limited downside is a pretty compelling proposition.

One watchout with this trade (and other long call option strategies) is thinking that since we use just one fifth or one tenth of the capital of buying stock that we can now buy five or ten times as many options and really cash in. We have to respect the downside risk. A big move down will wipe out this position. So we don’t want to put all our eggs in this basket.

But when the market is frothy and looking like it is going nowhere but up, this is a good way to participate in the upside while protecting the downside, assuming that there’s plenty of capital left to deploy if the market suddenly goes against the position.

What level of option risk goes best with what type of underlying security? Depending on the option strategy, your choice of underlying security type can have a big impact on your outcomes.

What level of option risk goes best with what type of underlying security? Most people reading this might wonder what in the world is the point of this topic and why should I care? Depending on the option strategy, your choice of underlying security type can have a big impact on your outcomes. This might get a little deep, but hang with me and I think it will be worth your time.

Level 0: Covered options- cash secured puts and covered calls

Level 1: Buy options

Level 2: Option spread trades- buy an option, sell an option

Level 3: Naked option selling

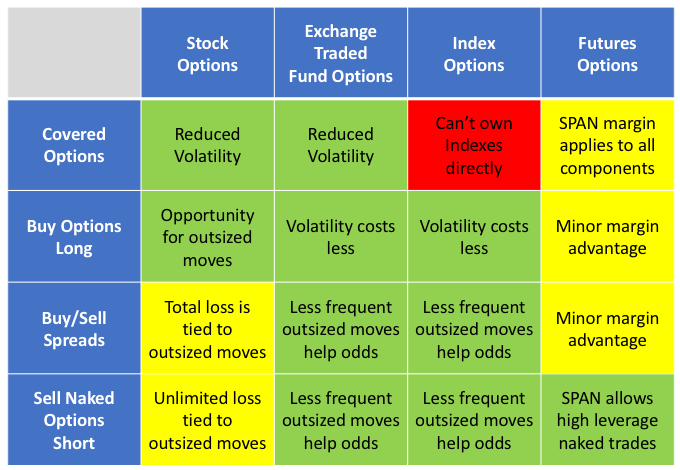

There are also four general types of underlying securities for trading options. With each comes different advantages and disadvantages. As a reminder the four types are:

So the question and point of this post is to examine which risk permission levels work best with which types of underlyings. It’s not an obvious question or an obvious answer. Most traders would say it doesn’t really matter- more risk is more risk, and less risk is less risk. But some underlyings are better built for certain strategies more than others. It doesn’t mean you can’t trade a strategy for a certain underlying, it is more of a question of what is optimal for the type of risk and potential return you are seeking in a trade.

The Matrix

I made a sixteen square matrix to evaluate each combination. I rated each pairing based on how well the option risk matched with the characteristics of the underlying. My conclusions are simply my opinions, and I welcome discussion and other opinions backed by data. So here is my matrix and what follows is the data and logic behind it.

Some types of option strategies and risk are better suited for certain underlying securities than others. With each combination is a brief explanation. Green choices are best.

Let’s review the boxes one row at a time, by risk level.

Covered Options

Covered or secured option strategies include covered calls, cash secured puts, covered strangles, and the wheel strategy. These strategies use the full value of underlying shares either in cash or shares to protect against loss from selling short options. The options being sold are much less volatile than the value of shares, so covered options are the only option choice that is a clear reduction in risk compared to owning shares outright. All versions of this option trading strategy limit upside growth while allowing the potential of losses to zero, but most of the time these strategies outperform owning stock outright. So how does this type of transaction impact different underlyings?

Individual stocks can be very volatile. Positive or negative news about earnings or products or lawsuits or mergers or management changes can make stocks move way outside their expected moves. These outsized moves happen more often than normal statistical distributions would predict. Even so, individual stocks tend to have options with much higher implied volatility than the overall market. For stock investors that want to dampen day to day moves of their portfolio balances, selling secured or covered options is a great way to participate in individual stocks with less drama. Because of the crazy volatility of individual stocks and the high implied volatility of options on individual stocks, covered options are a great match for individual stocks.

I would argue that for both the covered strategy and the stock underlying type, this is the strongest match in this row and column. There is no better underlying for covered options than individual stock, and there is no better option risk level for individual stock. I know a lot of people will disagree, but as we look at the other combinations, I hope you’ll at least understand my point of view.

Covered options on exchange traded funds are fine trades. It’s probably the safest possible option strategy there is if we want to call any kind of trading “safe.” We combine a bunch of volatile stocks together into a product that dampens volatility down substantially. Then we sell options against that new product that will rarely see moves outside the moves that are expected. The options may not pay a lot, but they won’t lose often either. A very boring way to make steady gains (and I’m thinking of boring as a good word here).

An argument could be made that covered options on ETFs is perfect for both, because it’s a double volatility reduction, and for risk-averse traders that’s a great combination. I get that, but for me, I think it’s a little too much volatility reduction, and sacrifices too much option premium for safety. Be less volatile with stocks by selling covered options, or be less volatile with riskier option strategies by using ETFs, not both. But I’m generally a risk taker, so maybe I under-appreciate the double volatility reduction of covered option strategies with ETFs.

Covered options on indexes is the easiest combination to rate on the matrix, because it is the one combination that can’t be done. We can’t own an index outright, so we can’t sell a covered call. If we sell a put and get assigned we don’t get the index, we just pay up the cash we lost. So, there isn’t a real way to sell covered index options on the underlying index. This is the only red square in the matrix because it can’t be done.

Covered options on futures can be done, but it doesn’t really make sense. Futures and futures options are all governed by span margin, so really there isn’t an official way to sell covered options on futures, because there is margin being used on every leg of the trade. No piece is fully “covered.”

I almost made the covered futures options block red, but you can kind of do it if you set aside the cash that the full notional value of the future is worth when you sell a call against a future, or sell a put on a futures contract. The problem is that your buying power won’t show that you’ve locked up the full notional value, so you have to track it yourself. It just isn’t what futures are about.

Let’s do a quick example to illustrate. Let’s say we have a futures product that trades for $1000 with a multiplier of 50. So the notional value of a contract is $50,000. If we buy a futures contract, the broker will use SPAN margin and only take away at most $10,000 of our buying power, even though we are on the hook for the full $50,000. If we sell a call on the same future, we’ll likely gain buying power, as we just reduced the volatility of the position. Maybe SPAN margin says we now only need $5,000 buying power, while we remain at risk for $50,000. So, our broker and SPAN margin don’t make us “cover” our options. You can keep $50,000 in your account to cover the trade yourself, but nothing forces you to, other than wanting to eliminate any risk of blowing up your account in a downturn. It’s fine to do this, but it technically isn’t a covered option, so it’s a yellow square on my matrix.

Buying options

When most people first learn about options, buying an option is the trade they can easily understand. You pay a premium to have the option to either buy or sell something. Margin is not a factor, because the risk is defined. The risk of the option is the cost, it can end up worthless, a total loss, but no more than what was paid to own the option. If the option ends up in the money, it may be profitable, maybe very profitable. Leverage comes from the possibility of virtually unlimited profit for a relatively low cost.

Buying puts or calls is like going to the security market casino. It’s a low probability bet that might pay off big, but often will lose what you gambled. But let’s not get all “judgy” against the strategy- lots of directional traders buy options to get the most out of a move they think will come. When implied volatility is low and the market is rolling up nice gains, it can be a very lucrative trade that exceeds its predicted probability. But which underlying security types are best fit to take advantage?

Individual stocks can make big moves up or down, and owning an option in the right direction when a big move happens can be great! But the market knows that individual stocks are prone to big moves so options are expensive to buy. A little move won’t cut it. A trader has to be very right on timing and direction.

But, if buying calls or puts is your thing, the biggest rewards are with individual stocks. So, I’ll give it a green square.

Buying options on ETFs is cheaper than stocks, but the likely moves won’t be as big. However, if the goal is to ride a trend that is going up faster than what implied volatility predicts or a slide going down, ETF long options are a good choice.

In a bull market, selling calls is usually a loser, which means that buying calls can be a winner. Buying calls on an ETF in a bull market will hit a lot of winners usually without a lot of capital required, so probably the best use of the strategy in this row.

Buying put and call index options is a very similar situation as options on ETFs. It’s really a matter of preference, depending on several factors. Some brokers restrict access to index options, so it might not even be a choice for some accounts. Most index options are bigger notional value, often 10 times as big as the equivalent ETF, so it might make more sense for a bigger account to use index options, while smaller accounts stick to ETFs. There are a lot more ETFs available than index options, so niche indexes either don’t have an index option or have such poor liquidity that the only choice is an ETF. Commissions per contract are often higher on index options, but per notional amount are lower. So, it depends on a lot of things. I’ve discussed the differences in much more detail in my write-up of different ways to trade the S&P 500. All the same trade-offs are true for the Nasdaq 100 and Russell 2000. So, for some traders buying options, the index option might be best so I’m coloring the combination green, but for most traders smaller, more liquid ETFs are going to be a better choice.

For futures options, the issues are similar as comparing index options to ETF options, except that buying futures options outright negates much of the advantages of futures options, but keeps the negatives. Futures options are a favorite of experienced and sophisticated traders because they can be traded with lower SPAN margin requirements, giving a trader more leverage, and also letting opposing positions reduce buying power. But, if a trader is only buying options, buying future options doesn’t gain much in buying power, but will cost a lot more in commissions and slippage from lesser liquidity than ETFs or index options. In my opinion the only time it makes sense to buy a futures option is to counter a bunch of short futures options or other futures position. I talked about this in my discussion of buying the 1 DTE straddle with futures options.

In the end, unless you have a really good reason to buy options on futures, it generally is a better trade to buy a similar ETF or index option product. So that’s why I colored this combination yellow.

Trading Option Spreads

Let’s define an option spread as buying and selling an equal number of puts or calls. There are a lot of ways to trade spreads, and many of my favorite strategies fall in this broad risk category. Option spreads have defined risk, but as strategies get more complex, understanding exactly how much risk a trade has defined can get a little tricky. It isn’t as obvious as the risk with buying an option, but the risk is known.

We can think of spreads in two main categories, debit and credit spreads. Debit spreads are trades where a trader pays to enter the trade, and credit spreads pay the trader to enter the trade. Credit spreads are often the highest leverage version of selling options, with the highest potential return on capital for many positions. With that potential high return on capital comes the risk of a total loss, often many times the amount that was collected to open the trade. How do these factors impact different underlyings?

With individual stocks having more likelihood of an outsized move, there is a bigger chance of a total loss on a credit spread, although that is somewhat balanced by higher premium from higher implied volatility. Debit spreads tend to limit max gain in exchange for improved probabilities compared to buying options outright. So, debit spreads on a individual stock miss out on big gains without a outsized increase in probability of profit.

Many traders favor spreads for individual stocks over naked options because of the defined risk limiting losses to a defined amount. My view is that both strategies have to contend with outsized moves and it’s a matter of picking which poison does the least damage. But because so many like spreads as a risk reduction for individual stock options and it is a viable strategy, I’ll rate this combination a yellow.

I’m going to lump ETF options and index options together for spreads. Just like with the earlier discussion on buying options, the difference between ETFs and indexes is a matter of preference and an individual’s account situations. Strategically, I like both for buying and selling spreads. Because ETFs and indexes are made up of many stocks, they have much fewer out-sized moves than individual stocks. This makes the leverage of spread trading work well, both in credit and debit type spreads.

As for buying spreads, I’ll occasionally buy a call spread when the market is particularly bullish and Implied Volatility is low. Buying options in any style is usually a low probability trade, but there are ways to improve odds, and using a spread to have decay on the short leg off-setting the decay being lost on the long leg can be a big help. We can get more exotic with diagonal trades selling a nearer term option while buying a longer term option and actually having positive Theta for our trouble. In all these trades I like ETFs and indexes because the results tend to be more consistent.

Many of the ratio type trades that I do utilize two sets of spreads, like the popular broken wing butterfly trade. Again, I like ETFs and indexes because outsized moves are less likely than individual stocks.

You may be sensing a theme. Less outsized moves make using the highly leveraged option spread on ETFs and indexes my favorite choice for spread trades. It’s green squares for both, and my favorite use of ETFs and indexes, as well as my favorite way to trade spreads.

In theory, futures option trades with spreads should also be as favorable as ETFs and indexes. They work about the same and have the same type of probabilities. But there are two things that I don’t like about trading spreads on futures. One is a personal nit-picky concern, and one is a concern that virtually any trader would have.

Let’s start with the most legitimate concern. Futures options are less liquid than ETF and index options. They have wider bid-ask spreads, and they are harder to fill close to the mid price between the bid and ask. In many trades, the tick size, or the amount you can adjust your limit price by is substantially bigger than for the same trade on an index option on the same thing. For example, on $SPX index, we can adjust our limit orders by 5 cents up or down, but with /ES futures, we have to adjust our order in increments of 25 cents. To make it worse, often the volumes are much lower and even giving up 25 cents won’t get an order filled. So, it can cost a lot to get filled, and we haven’t even talked about commissions, which are generally also higher, both per contract, and even more so as percentage of the notional value of the position. Maybe someday these costs will get lower and it won’t bother me as much, but I just don’t like it for spreads with futures options.

But what about SPAN margin you might ask? Doesn’t that extra margin make it palatable to pay a little more so you can get that super-duper leverage for traders that like more risk and more reward? Well, this is my nit-picky problem with spreads on futures. SPAN margin isn’t that much extra buying power for spreads with futures options compared to indexes, ETFs, and individual stocks. Because spreads have defined risk, the two sides of the trade already have formed a hedge and SPAN margin doesn’t give much more buying power than the reduction from calculating the max loss of the total spread being wiped out. To be fair, futures traders get some additional buying power, but it isn’t enough for me to justify the higher costs of trading spreads with futures options.

I know there are traders out there that like futures with spreads that little extra buying power that comes from SPAN margin, but for me it makes more sense to go with an index option or ETF option where my risk is defined and doesn’t change. So, I’m giving this spot on the matrix a yellow. Proceed with caution.

Selling Naked Options

Selling naked options is supposed to be the riskiest of the whole bunch of risky option trades. In one way it is in that maximum losses are essentially undefined, but even with margin, the leverage of Theta or Delta as a percentage of buying power is often less than what happens with spreads. So, as long as we avoid outsized moves (which we can’t, by the way) there’s a strong argument that selling naked options is not nearly as risky as it would seem at first glance.

Let’s be clear about what selling a naked option is about. With covered options, we can sell a call or a put and there is either cash or shares covering the short option positions. For naked trades, the broker lets us sell on margin. Often we are only required to have something like 20% of the notional value set aside for covering the option sale. That’s great for our account as long as the price doesn’t move against us more than that 20%. Actually, the broker will increase buying power requirements as price moves against a position, so the requirements are always in flux. But with plenty of extra cash as a buffer and markets not going crazy, it’s manageable.

So, we are selling options on margin. What underlying type does this work best with? Let’s check out our four choices.

Individual stocks are the most likely underlying to have an outsized move, so they are the most likely to get a naked option trade into trouble. It doesn’t take much, a change at CEO, a merger or acquisition, surprising earnings announcements, good or bad product news- any of these can trigger a move way beyond the expected move. With individual stocks, the probability of an outsized move both up or down tends to be greater that what Delta would predict, or it often just isn’t that great compared to the other products with diversified components.

That’s my reason for avoiding naked options on individual stocks. I know lots of people trade naked options on stocks all the time, diversifying their holdings to reduce overall risk. But for me, why not use an underlying that is already diversified? I know individual stocks have higher Implied Volatility to pay a seller to take on that added tail risk, but for me it just isn’t enough. I’ve seen too many situations where a trader has gotten a very nasty surprise and lost way more than they thought they could. It can happen with any naked trade, but it’s more likely with individual stock options. So, for me this is a yellow box- proceed with extreme caution.

Now, let’s not try to make the argument that naked options on the other types of underlyings are super safe. They aren’t, and you can lose big. Ask anyone who had naked puts on the S&P 500 (any version) when Covid hit in 2020. It was bad. But those kinds of moves happen much less often than negative moves in individual stocks. People that trade naked options take a lot of risk, and so the question for the remaining three underlying types isn’t which one is least risky, but which gives you the biggest bang for the buck? If you are selling naked options, you better know what the risk is, but how do you maximize return when you have a trade go your way?

Like the last two levels of risk, ETFs and index options have essentially the same pros and cons for naked options. While there is significant tail risk, it isn’t as high as individual stocks. So, naked options sales on ETFs and indexes tend to perform better than the expected move would predict. This makes these underlyings a better choice for underlyings on naked options. As a result, I’m giving these matrix squares a green rating.

Finally, we have selling naked futures options. On one hand this is a highly leveraged trade with ultimate tail risk due to SPAN margining. On the other hand, this combination gives a trader the potential for significant high returns on high probability trades that otherwise might not make sense.

I look at naked futures options as the ultimate “go big or go home” trade. If a trader wants to trade futures options, selling naked gives the ultimate amount of exposure for the least buying power. SPAN margin allows a trader to use a fairly small amount of capital to open a naked trade. And if a trader balances the Delta of both sides of a trade, buying power requirements become even less, as the total risk is considered in required capital.

SPAN margin also lets a trader have different sides of the trade be at different expirations and have the net exposure of each side be considered in the SPAN margin calculation. The point is that for the most agressive, risk-tolerant option trader, there is no higher leverage way to sell options than selling naked options on futures. For that reason, I really like futures for naked options.

Selling futures options naked still have the issue of poor liquidity and higher commissions, but the flexibility of SPAN margin finally makes it worth the cost for risk-tolerant traders. It is worth noting that the liquidity and commissions are significantly more of an issue for traders that trade “micro” versions of futures options, like /MES, compared to /ES. Whether it is a futures product on an stock index, a commodity, or a currency, the micro versions just have a lot less open interest and liquidity. So, if account size limits trades to micro futures, a trader has to watch which expirations and strikes can be entered and exited without huge price slippage, particularly when exiting early.

Despite the cost issues with futures options, selling naked futures is my favorite use of futures options, and my favorite way to sell options naked. I give it a green box on the matrix. I don’t rate it this way to suggest it is a safe trade, but that it is the ultimate use of options leverage.

Bonus sections

There are a few option strategies that don’t fit neatly into the four categories of risk that I think deserve a special mention because I talk about them in other parts of the site.

Bonus #1 Ratio Style Trades

Ratio style trades are a more complicated type of strategy where there is an unbalanced number of contracts sold vs bought- a lot of times a 2:1 ratio in some variation. If there are more contracts sold than bought, the trade becomes a level 3 naked trade, like the 1:1:1 or 1:1:2 put ratio trade that I discussed in other pages. But often, I use a level 2 defined risk version of the trade by adding long options to equal out the short options, usually creating a wide credit spread along with a narrow debit spread, like a broken wing butterfly (1:2:1), broken wing put condor (1:1:1:1), or 1:1:2:2 put ratio.

These trades are technically either a group of spreads (level 2), or a spread with a naked short option (level 3), but is there a difference in what underlyings are best for these kinds of trades because of the ratios and odd ways of managing these types of trades? The short answer is not really.

For level 2 defined risk ratio trades like butterflies, condors, and 1:1:2:2 trades, I like ETF and index options for their liquidity and reduced volatility. This is the same logic as with spread trades in general.

For level 3 naked versions of ratio trades where there are more short options than long, my preferred underlying is futures options due to the reduced buying power of SPAN margin. These trades tend to be fairly highly probability of profit, but with significant tail risk from black swan type events. SPAN margin considers this risk and allows a trader to use a fairly small amount of capital to enter this kind of trade. Anyone trading this way must consider the significant tail risk into their management strategy.

A trader can use ETF or index options for these naked ratio trades, but they consume a lot of capital with standard option margining. Traders with portfolio margin accounts might find this more acceptable. For understanding of different types of margin in options, see my post on the topic.

Bonus #2: 0 DTE trades

0 DTE trades have special considerations because of their short time frame. Let’s throw in 1 DTE and any options trade that has just a few days until expiration. All these trades focus on either last minute moves or the extreme decay that comes in the final days or hours of an option contract.

Individual stock options don’t have daily expirations, so expiration day trades are usually limited to Fridays or end of month at most. That essentially eliminates them as a candidate, but it gets worse.

With options near expiration, assignment at expiration or near expiration is a big concern. Individual stock options and ETFs in the money can be unexpectedly assigned into shares in the days before the options expire. And if options are held to the end of the expiration day, assignment can happen even if the market closes with options out of the money. A late after the market news event could trigger option holders to exercise their options on individual and ETF options, so you never know.

So, that leaves index and futures options. Index options are settled to cash at the market close. Futures options expire into futures contracts at the market close. A trader doesn’t have to worry about after market events impacting an expired position. The only exception to this is monthly index options that settle on the open of the market, but stop trading at the market close of the previous day. These contracts have AM expiration, where almost all other options expire in the PM, at the market close. The ticker symbols for index options expiring and settling at the market close generally end with a “W” for weekly, which originally was for the weekly expirations that happened every week, but now happen every day. The monthly options, which are the very original index options, don’t have a “W” at the end of their ticker indication.

Settling to cash vs settling to futures contracts or shares is a big difference. Most expiration day traders don’t want to deal with the underlying securities ending up in their account and the significant notional value that comes with them. Because of that, index options are far better choices for trades approaching expiration.

Traders with small accounts can choose between micro index options, like $XSP, micro futures options like /MES, or ETFs like SPY. They have different pros and cons. Micro index options have fairly poor liquidity with wide bid/ask spreads and big tick sizes for poor fills, but settle to cash at expiration. Micro futures options have worse liquidity and bid/ask spreads, plus high commissions, and settle to futures contracts, all negatives, but are usually half the notional size of the other two low capital choices. ETF options tend to have good liquidity, but settle to shares at expiration, or after expiration. None of these are ideal, but if a trader wants a small option stake on expiration day, these are the choices to consider.

Conclusion

So, there you have it. A fairly exhaustive analysis of the various combinations of trade types vs underlying security types. Some of the factors I consider most important in this analysis, may be less important to other traders, and some accounts at certain brokers may not even give a trader a choice to have some of these types of underlyings available. Others may not have some risk permissions available.

In any case, my hope is that whatever level of risk or underlyings a trader has available, it is clear what combinations make might more sense from a viewpoint of risk, potential reward, capital usage, and trading costs.

Most people have full time jobs. Can someone manage an options portfolio and work full-time without watching the market all day? I say yes.

Most people have full time jobs that don’t involve the financial markets. Can someone manage an options portfolio and work full-time without watching the market all day? I say yes, and they may do even better than a full time trader. The reasons may surprise you.

For several years I was a full time options trader, watching positions in a bunch of accounts, adjusting every day as the markets moved. Many of my positions were short duration, which meant that I needed to stay on top of them. Much of my strategy involved rolling to avoid getting to expiration or to keep my strikes out of the money. There were lots of good reasons to spend the day reviewing every position in every account to determine if any adjustments were needed. And I enjoyed it. It was fun managing accounts that were growing and generating the income I needed.

But in 2022, I had a series of events that drained my accounts that provided my spending money. (Separately, I’ve written about my lessons learned in 2022.) I’m not yet to the age where I can take money out of my retirement accounts without penalty, and I didn’t want to get into Substantially Equal Payment Plans (SEPP) to commit to withdrawls- that’s a big topic for another day in itself. The bear market coincided with some unexpected expenses, so I liquidated most of the liquid accounts I had available at bad times. My accounts that had been providing nice streams of income lost a lot of value when I needed them most. So as the year came to a close, it was clear I needed to get a “real” job again.

Changing to a full time “real” job

In January of 2023 I started working full-time, a typical 9-to-5 job. But I still had a number of accounts to manage, a combination of retirement accounts and leftovers from my cash/margin accounts that I hadn’t completely used up. (I didn’t go broke, I just wasn’t flush enough to live off my accounts that I could draw from.) I had to have a different approach to account management- the days of full-time trading were over.

I still wanted much of my portfolio to be option-based. I’ve seen how options give me leverage and the ability to manage in any type of environment. But I knew that my approach to managing daily had to dramatically change. I couldn’t watch the market and do my job, so I needed to completely change my trading routine.

First, I decided to stop all 1 DTE and 0 DTE trades. Honestly, these had not been that profitable and were the most time-consuming positions I had been trading. It was almost like I had been trading them to keep my day completely filled with activity. If you read about my 1 DTE Straddle management approach, you’ll see that I try to take profit and adjust positions throughout the day, which is very time-consuming. 0 DTE trades are just as time-consuming for most strategies. I know some traders open a position and set up stop and profit limit orders and go about their day, but even that seemed like more than I wanted to do. So, no more expiring option trades.

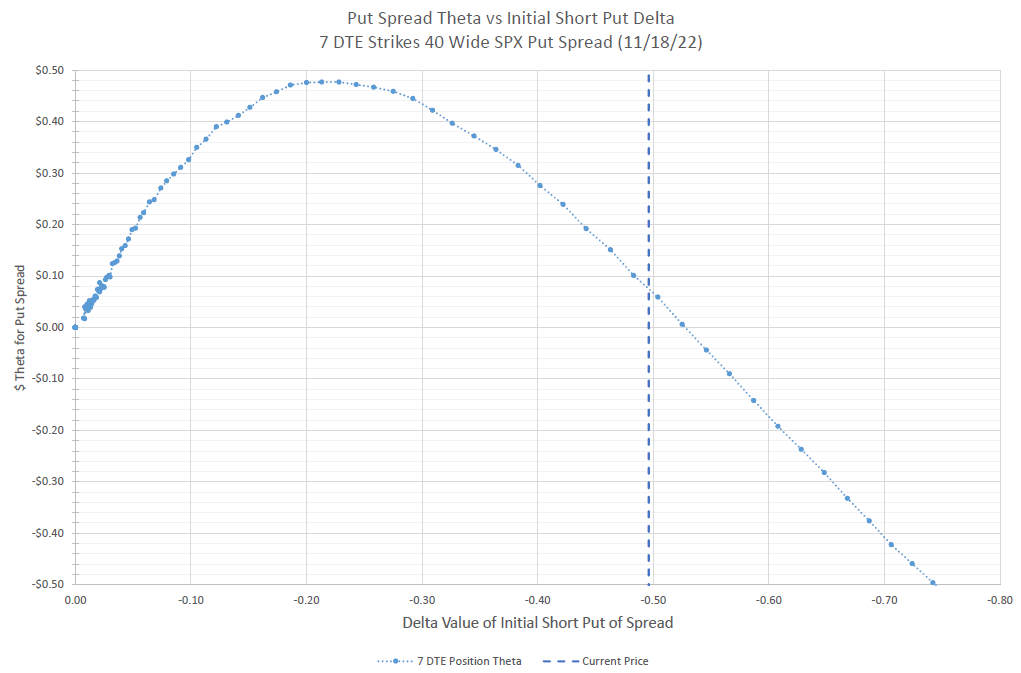

Next, I moved all my shorter duration trades out in time. I was doing some 7 DTE put spreads, rolling almost every day. These were problematic in the 2022 bear market anyway, so it wasn’t a hard decision to get rid of them. I also decided to mostly stop doing 21-day broken butterfly trades. This was a harder decision, as I’ve had good success with defending these even in tough times, but I knew that I just didn’t want that responsibility to keep an eye on them.

So, I was left with positions mostly 4-7 weeks from expiration- put spreads, iron condors, covered calls, covered strangles, some 1-1-2 ratios, and some long duration futures strangles. All these trades are far enough out in time that a move during the day won’t be a huge loss or need an immediate adjustment.

Initially I thought I’d try to spend a half hour each morning when the market opened before I started my job. For a few weeks I did this, but I found that my work often required me to be available for an early call during that time, or there were urgent items that couldn’t be delayed, and that time wasn’t available. I’d miss a day, then it was two or three in a row, and I realized I needed to be able to have an approach that could go several days at a time without requiring action. But, I also noticed that missing several days wasn’t hurting my market results, especially in a choppy market.

Since almost all my trades are based on profiting from premium decay, time is my friend. I need time to pass and the market to remain somewhat stable. Getting away from the daily noise of the market up for some reason one day and down the next for another reason helped remind me that selling options is about being patient. It also reminded me that market movements are mostly noise that is statically insignificant. If I don’t react to every move, the market tends to chop up and down and not really move that much or that fast over time, which is exactly what a seller of options needs.

My new routine

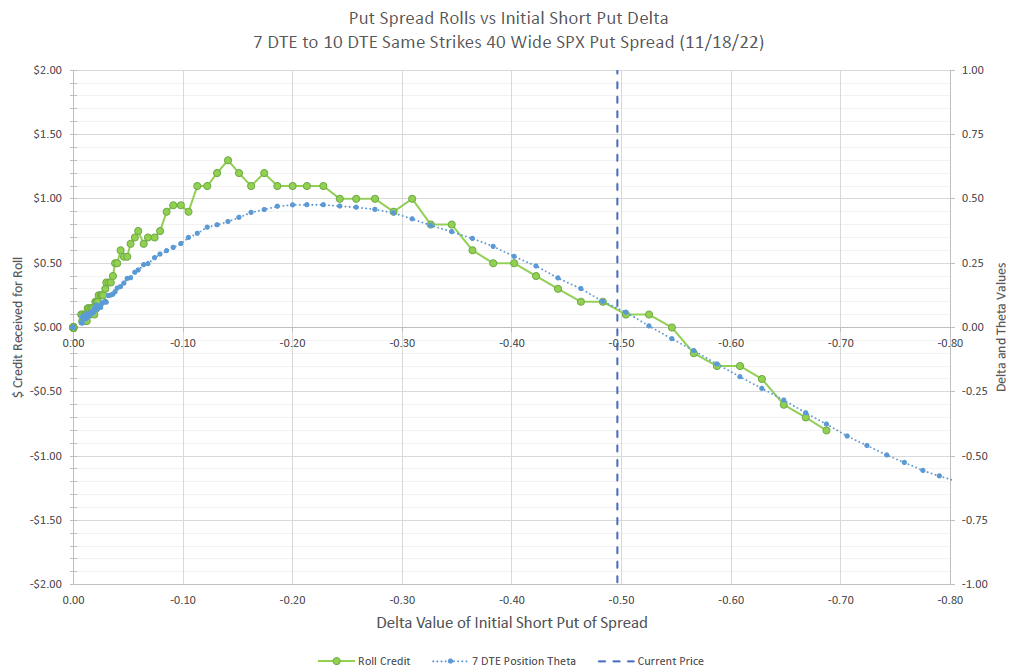

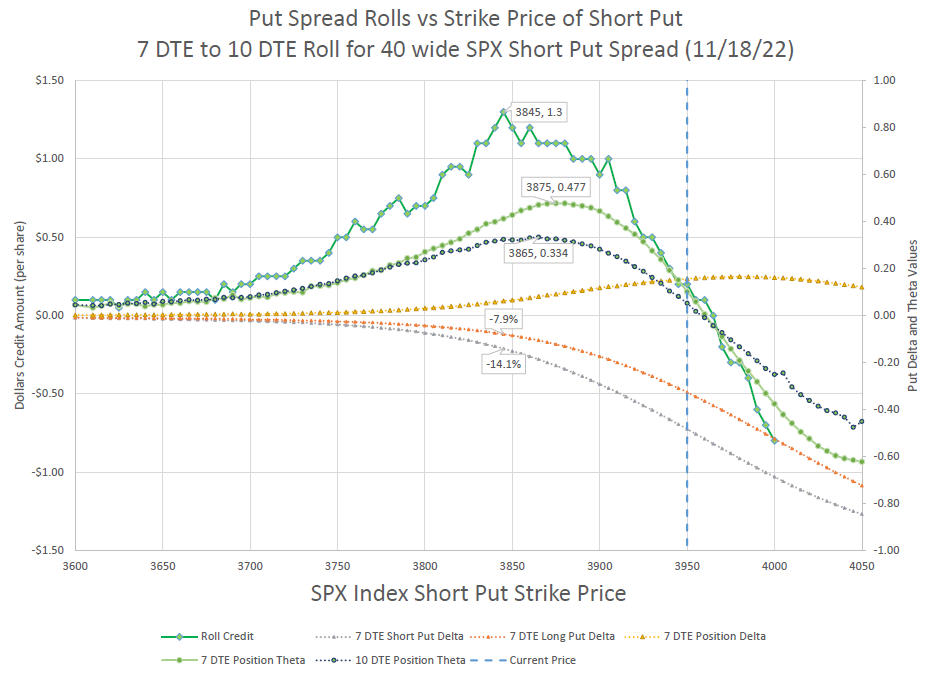

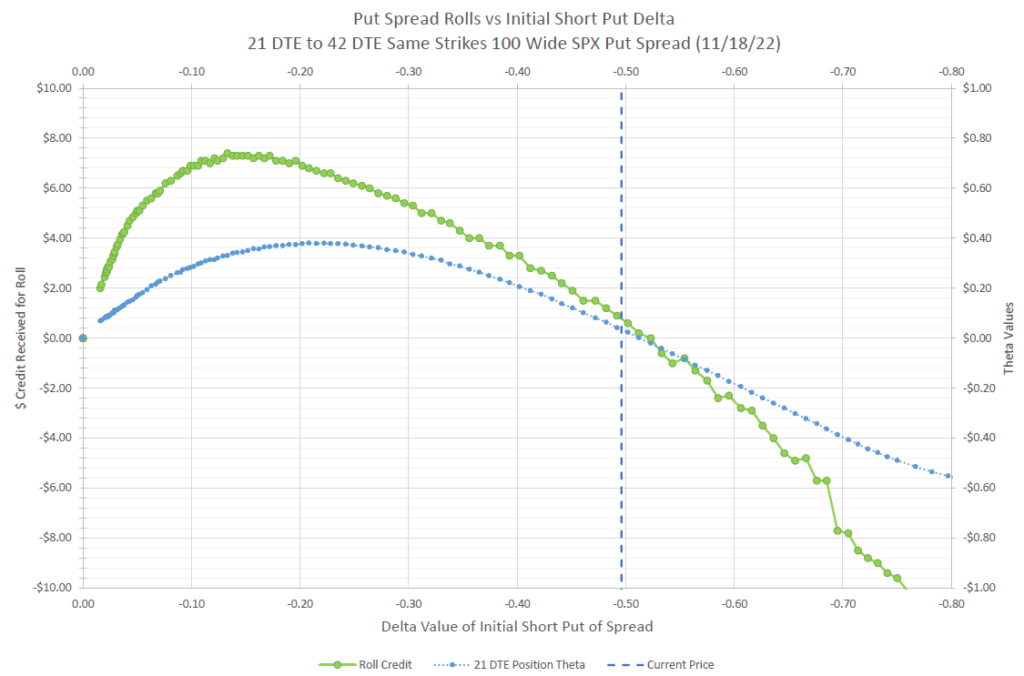

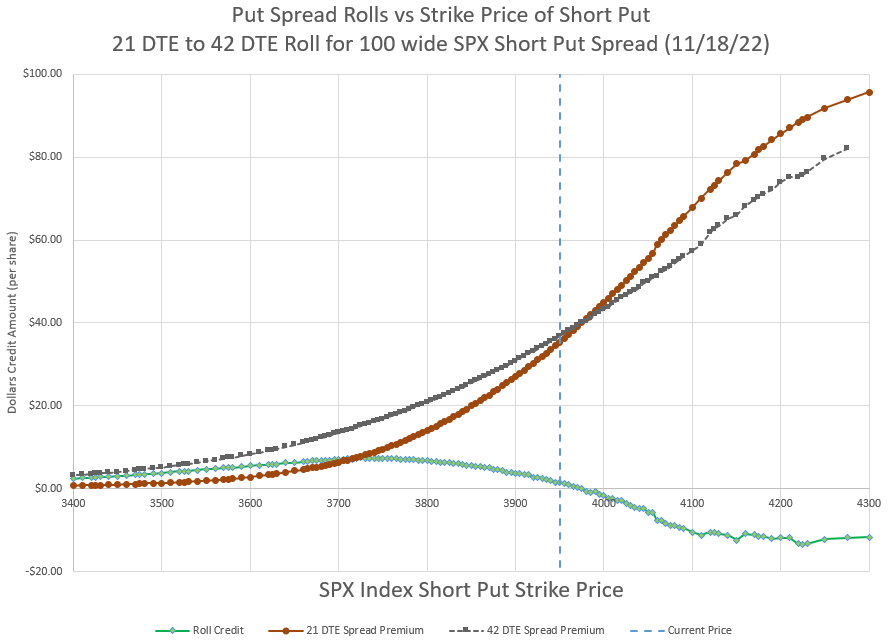

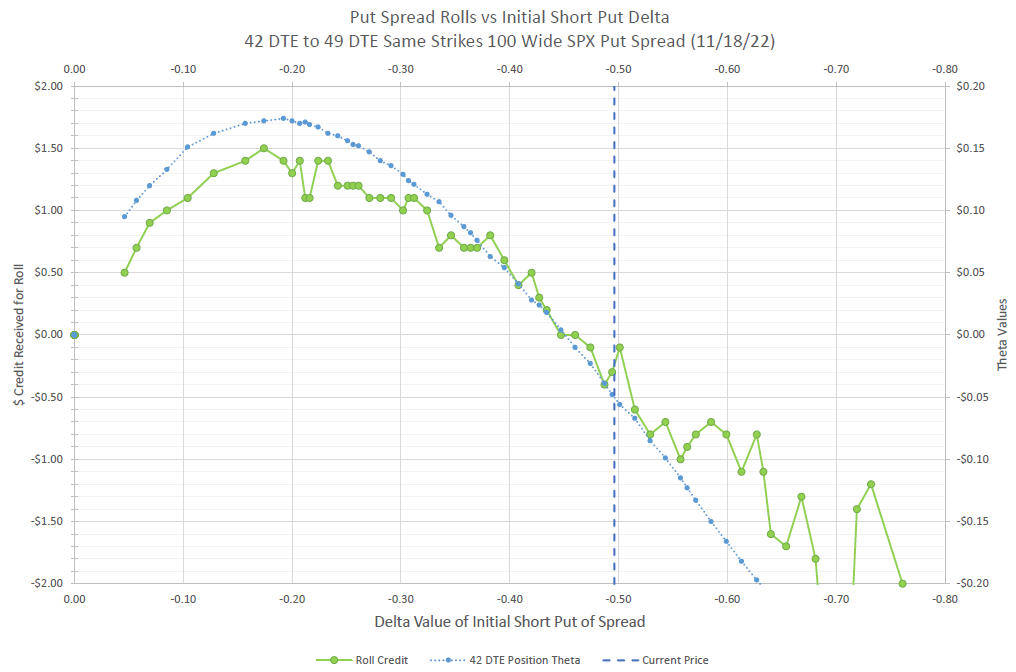

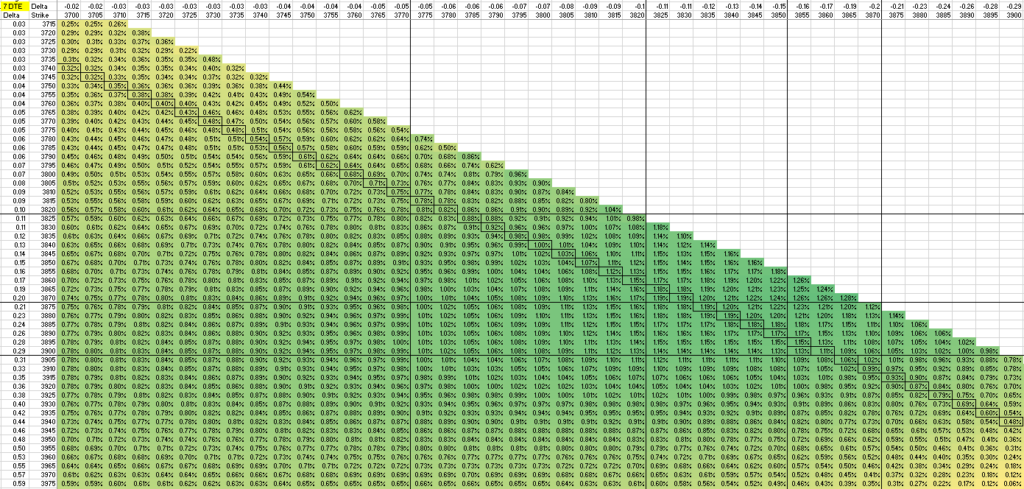

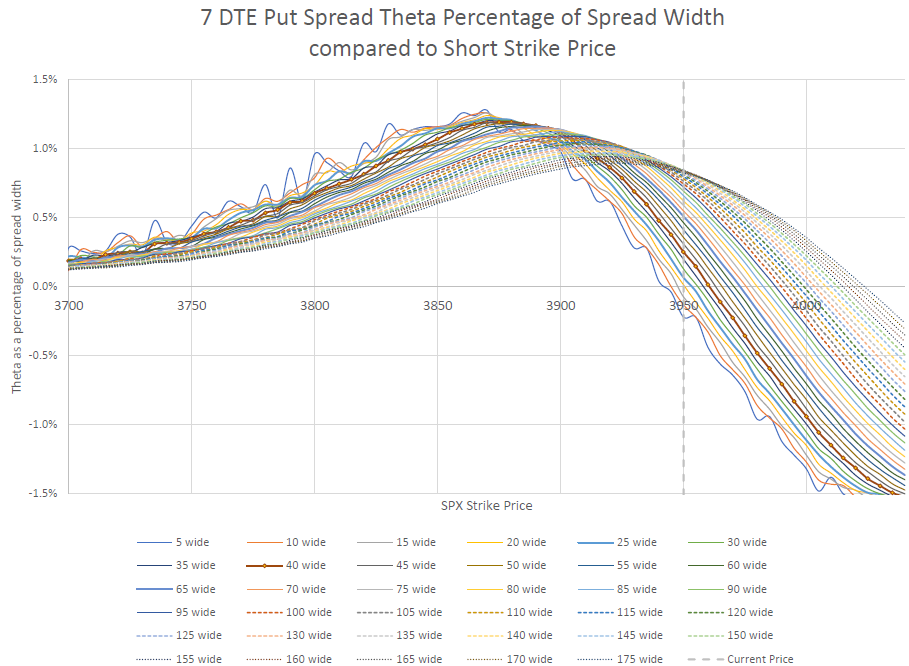

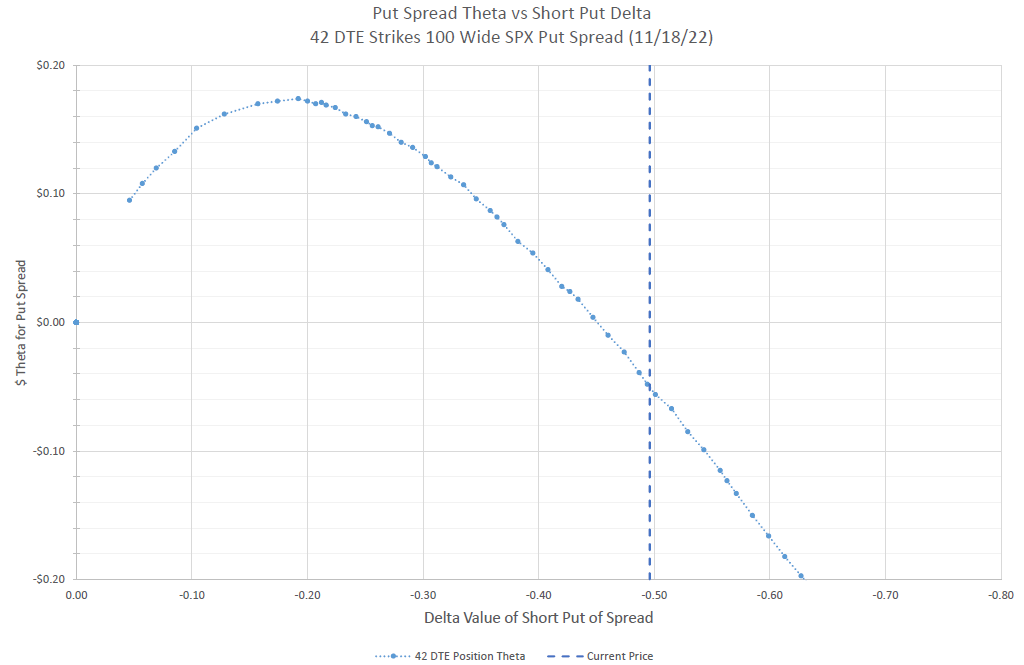

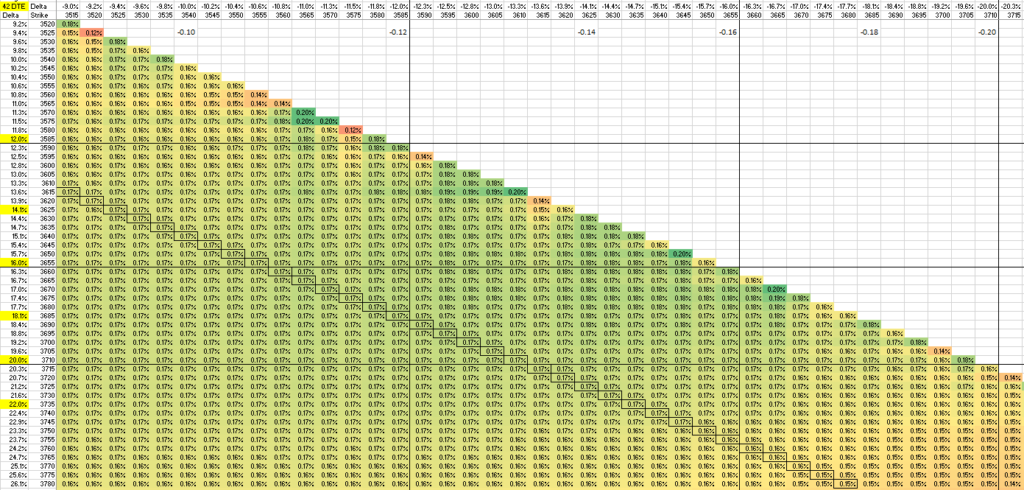

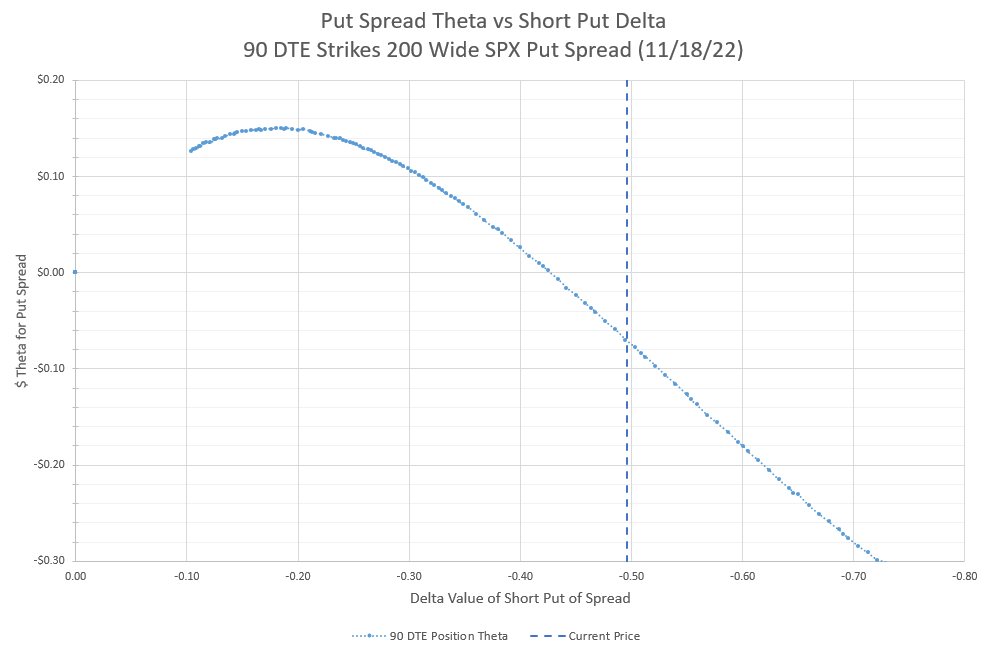

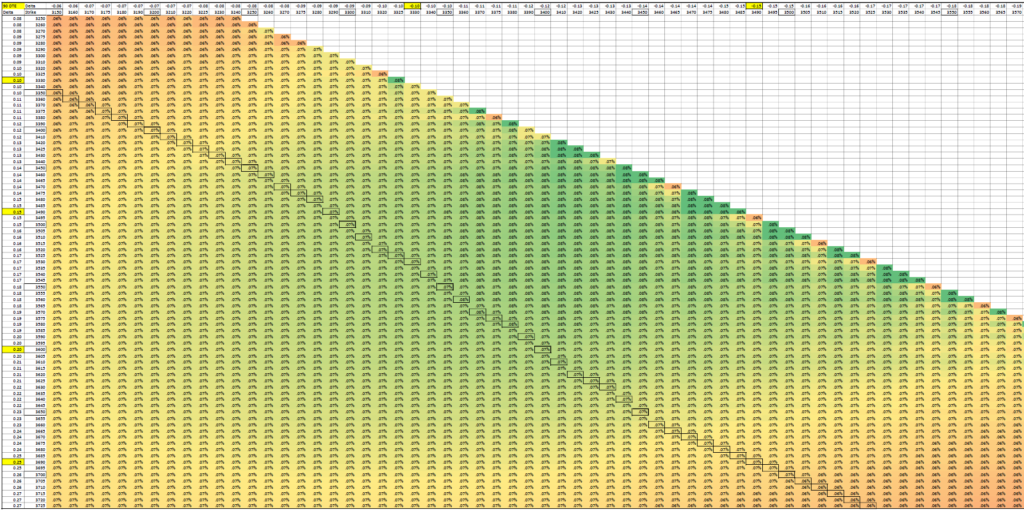

With time, I’ve settled into a trading routine of doing a thorough review of all my positions about once a week. For positions in the 4-7 week to expiration window, I like to roll and adjust Delta about once a week, essentially kicking the can down the road, trying to pick up a percent or two of return on capital each time. Timing isn’t critical, but I want to keep my spreads in the sweet spot where they decay the most, with short strike’s Deltas in the high teens to low twenties. I’ve written about this in many posts that address best Deltas for put spreads.or for rolling put spreads. I’m leaving a bit of money on the table, missing the very best timing, but I’m making up for that by not over trading, which I clearly was in 2022.

Some of my longer duration trades, that are 2-4 months out, can go weeks or even a month or more without an adjustment roll. My weekly checks just make sure that they are not getting close to being tested or getting to a duration that I want to extend. My philosophy with those positions is an “if it ain’t broke, don’t fix it” approach. So, not much to do with these.

So, it takes me about an hour a week to make adjustments during market hours. I find a break in my day, or a day when I can get trades in early before my work day starts. I’ve been surprised at how manageable it all is. I’ve realized that when the day comes that I don’t need a job anymore, I will be able to manage my trades with a lot less time than I was using the last several years. I don’t plan to ever trade all day long again.

Results

The great news is that I’m very happy with my results. My most aggressive accounts have been pulling in about 10% returns each month so far in 2023, and all my accounts are handily beating the market. So, I’m very happy with my new approach. I know that the market isn’t always this calm, but I also know from 2022’s bear market that longer duration trades in high volatility have much better outcomes than short duration trades, so I’m confident that this approach would have done well in that environment, better than I did trading every day with short duration trades.

A covered strangle? It’s a conservative three component trade made up of long stock and selling both a put and a call out of the money.

What’s a covered strangle? It’s a three component trade made up of long stock, selling an out of the money call, and selling an out of the money put. It’s a high probability trade that is less volatile than owning all stock, but uses a lot of capital keeping returns somewhat limited. It’s a great way to ease into strangles, which typically are reserved for very experienced traders. It can be traded in almost any account because it only requires Level 0 option permission approval, so most retirement accounts will even allow it.

A covered strangle is bullish, making money when prices go up.

Technically, a covered strangle is a combination of a covered call and cash secured put, two strategies that are a favorite of many conservative option traders. It’s “covered” by stock on the call side and cash on the put side. Let’s say we have 100 shares of the SPY ETF trading at $400 per share, a value of $40,000. We can likely sell a 420 strike call a month out for about $2.00 premium or $200 total for the 100 share contract. If we have another $38,000 cash in our account, we can sell a 380 strike put for around $4.00 premium or $400 for the contract. We’ll likely collect a little around 1.5% of our capital at risk. We have $40,000 in stock and $38,000 in cash securing our strangle. We can hold to expiration and let the chips fall where they may, or my preference of managing early and rolling out for more credit.

A trading friend has been talking up covered strangles to me for years. Honestly, I’ve looked past it as it seemed like a boring trade that takes a lot of capital for a somewhat small return. At first glance, there’s limited upside because gains are capped by the call, and unlimited (to zero) downside. If the stock price goes up, the call can be triggered and the stock sold for the call strike price. If the stock price goes down, the stock and the put both lose value. And we are doing this for a 1.5% return on capital? And this is supposed to be a good conservative trade? Actually, yes! Let’s dig a little deeper and see why.

Probabilities, Volatility and Manageability

There are three major factors that make this trade desirable. First, there is a better than 50% probability that this trade will deliver a profit. Second, this position is significantly less volatile than being fully invested in stock. And finally, strangles are one of the most forgiving trades to manage, allowing continual repositioning, or a variety of other trade variations if held until expiration or assignment. As a bonus benefit, we are invested in stock, often with dividends, and over time the market tends to go up for a gain. Let’s review each benefit in detail.

Probabilities of Profit

If we look at our example trade mentioned earlier, let’s assume that we are selling a 20 Delta put and a 20 Delta call. We can quickly see that if held to expiration, there’s a 40% chance of one of the options expiring in the money- 20% for the call, and 20% for the put. If the concept of Delta matching percentages is new to you, refer to my webpage on Delta. But even if an option ends up in the money, it doesn’t mean the trade loses. We can look at it from just the stock, just the strangle,or the full covered strangle.

The stock itself is a slightly better than 50/50 proposition. On average, we expect to see a bit better than 0.5% return per month. But that’s on average. Our expected move for a month tends to average about 4%. (See the page on Expected Move if this is a new concept.) So, a lot of up months and a lot of down months, but we also expect the stock to stay inside the strike prices of the options sold. Historically, our monthly probability of profit is between 55 and 60%. Individual stocks may have somewhat different probabilities than indexes, but most are in this range.

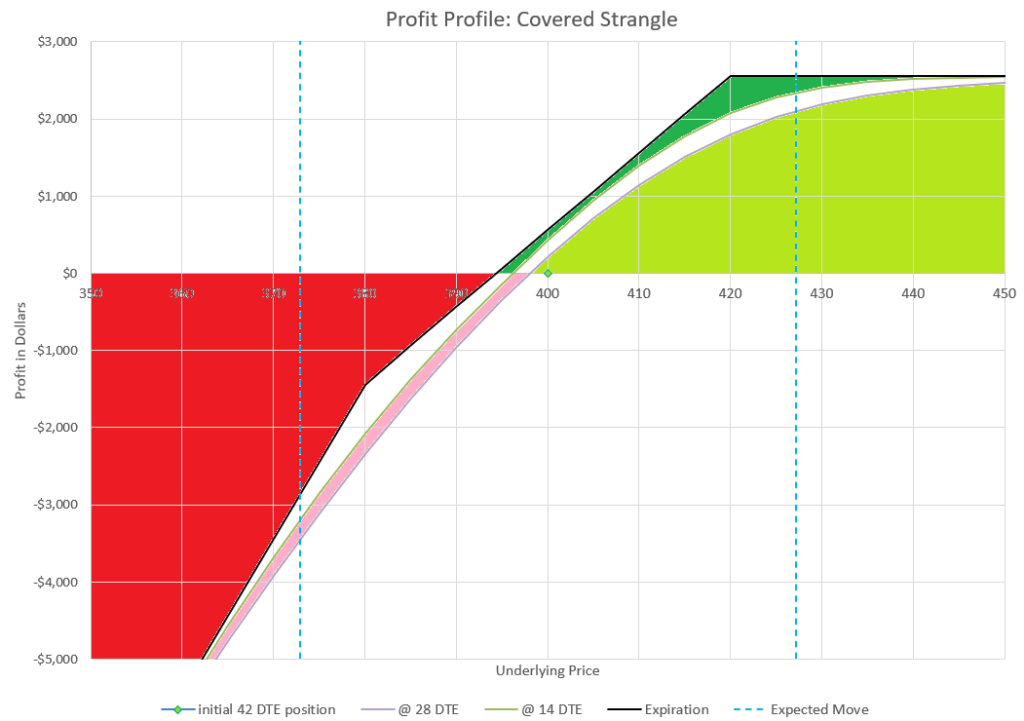

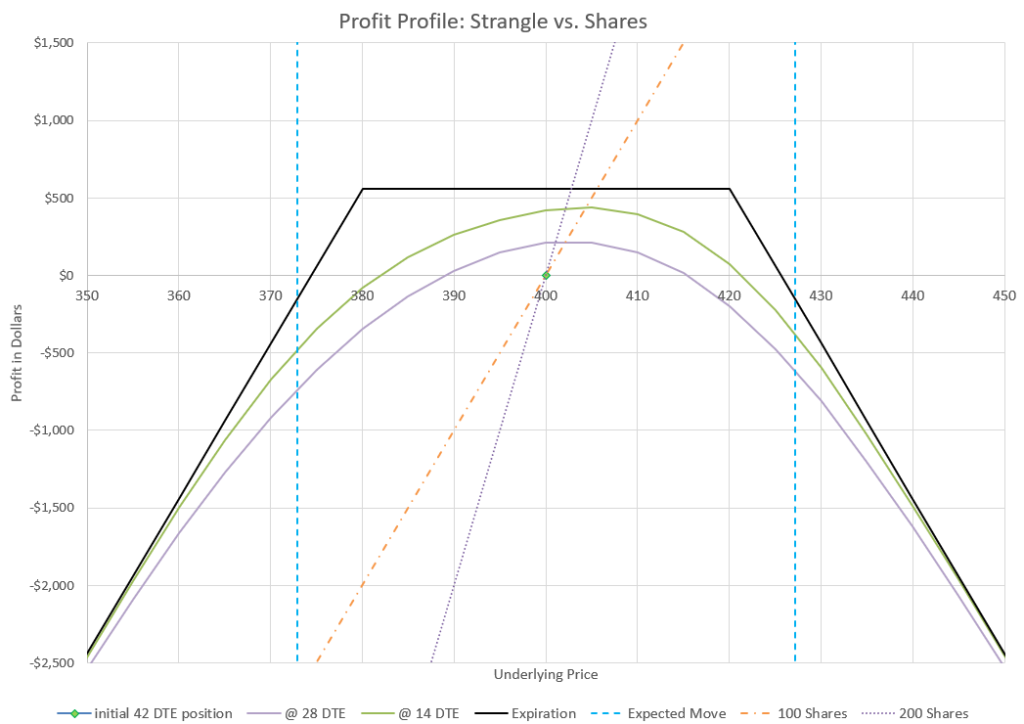

This chart illustrates the profit contribution of the strangle components and the 100 share components. For contrast 200 shares profit is also shown. Notice that only the strangle profit changes with time passing- the shares profit only based on price changes.

The strangle of a short put and short call have well defined probabilities. While the probabilities of ending in of the money are 40% at expiration, we also have to consider that we have collected premium that gives us an additional cushion before we actually lose money. In our example, we have collected $6 premium and have strikes $20 away from the current price. We don’t lose money at expiration until the stock price ends up over $26 away from our starting price. A quick check of options Deltas will show that we have about a combined 25% probability to expire over 26 points away from our starting price, so we have a 75% probability of at least some profit from the strangle. If we manage early, we can improve this probability to an even higher rate, reducing the possibility of an outsized move blowing through our strikes.

If we do some basic math, the average probability of the stock and strangle would be a little better than 65%, based on our probabilities of each part of the trade. But there’s a little more subtlety to probabilities of the covered strangle, due to the interaction of options and stock. On the upside, we could be assigned and have our stock called away if the market goes up more than 5%. We’d make $2000 on our stock plus keep the $600 option premium we collected, a $2600 profit on $78,000 capital, a 3.3% return. No matter how high the stock goes, our gain is capped at 3.3%. On the downside, our stock starts losing money immediately, but we still have our $6 premium collection that buffers our total position down from $400 to $394 before the covered strangle is at a loss at expiration. The put doesn’t add to the loss at expiration until it is in the money, but below that both the stock and the put lose equal amounts as the price declines. If we check the option table, we have somewhere around a 38% probability of our stock expiring more than $6 below our start price, so actually we have a 62% probability of profit for the full covered strangle.

If it wasn’t already clear, the covered strangle is a bullish trade. Up moves are always profitable, and the only way to lose is a market decline more than the total premium collected. That shouldn’t be a surprise, owning stock is bullish, a strangle is neutral, and the combo covered strangle is still bullish.

We’ve discussed in other posts that Delta actually overestimates moves and that probabilities are actually higher for profit, especially on the put side of the trade as put buyers buy up insurance to protect from big moves down. Since our risk is to the downside, our probabilities actually are a little better than Delta might suggest.

From this discussion, you can see that there are a number of ways to think about probabilities with a covered strangle. The takeaway should be that probability of profit is high. In a bit, we’ll talk about how management can help improve our odds even more. But first, let’s talk about how a covered strangle reduces portfolio volatility.

Portfolio Volatility Reduction

It should be somewhat obvious that when we combine a pure bullish strategy of owning stock with a neutral strategy of a strangle, we have a combined strategy that is somewhere in between. Let’s compare a covered strangle to being fully invested in stock.

Comparing the profit and loss of a covered strangle to 100 shares or 200 shares of stock shows more profit if price doesn’t move much and less change with price overall. The only time that being fully invested in stock outperforms is when there is a large move up.

Using Delta to represent equivalent stock (another way Delta can be used), 200 shares of stock has a 200 Delta value. A fully neutral strangle paired with 100 shares of stock has 100 Delta value. Both positions use the same capital, but the all stock position will move up and down twice as much day to day as the covered strangle. Delta will vary from neutral as the underlying price changes, reducing with price increases and increasing as prices go down. So, position volatility will go up if the underlying price declines, and vice versa. It should also be clear that the strangle and the stock behave differently, and that difference diversifies the price response of the covered strangle.

You might think that with a decrease in position volatility, we would be giving up a lot of potential return. But actually, we can expect as much as 0.5% average return per month from the strangle, about the same as the stock. But since one side of the covered strangle is likely to do better in each point in the trade, returns are likely to be more consistent than either by itself.

Managing Strangles

Of all option trades, strangles are about the most manageable of all strategies. Both the short put and short call can almost always roll out in time for a credit, whether the strike is in or out of the money. With spread type options, only out of the money strikes can collect credits from a roll. For single short options, there is no long strikes to buy back.

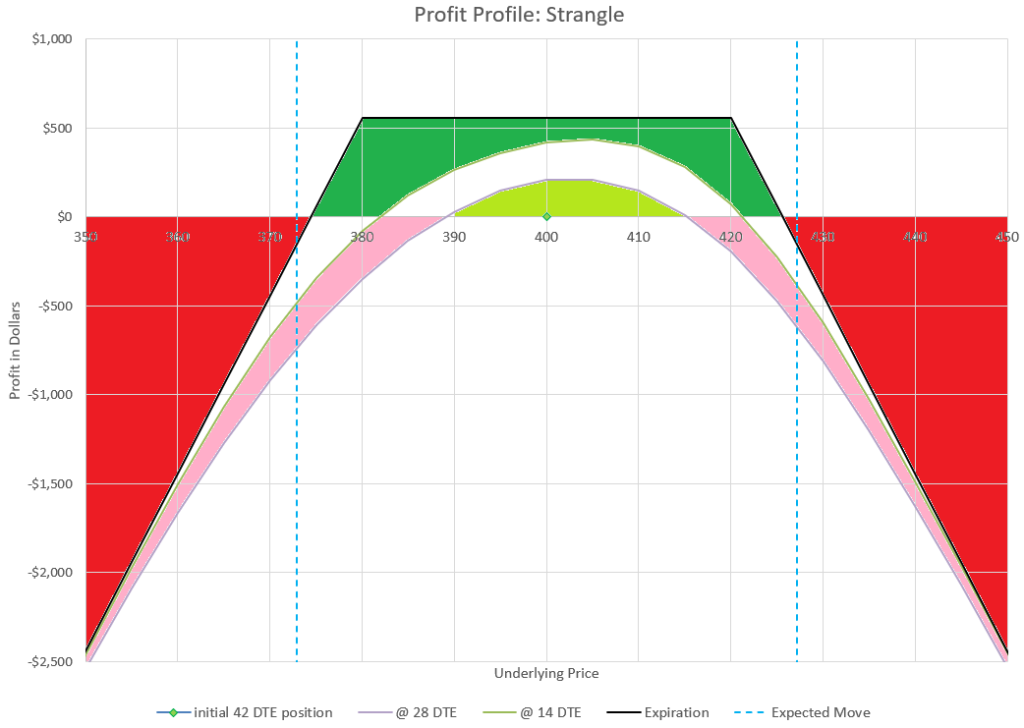

The Strangle portion of the Covered Strangle is profitable at expiration when prices stays inside the expected move.

I like to use rolls to recenter my strikes around the latest prices. Going back to our example, if the underlying price went down to 390 after a couple of weeks, we should be able to roll our strikes out a few weeks more with 370 put and 410 call, and collect a credit. The idea is to use rolls out to just keep collecting credit. Compared to rolling spreads and iron condors, there’s way more forgiveness, and more likely profit even in moves that test the strike prices of either option. Sometimes, I may pay a debit on the tested side to move the strikes well out of the money, and collect a bigger credit on the untested side and move the strikes closer to the money when they are very far away. Even if my strangle position is showing a loss, I can usually still collect a credit and keep the trade alive and let time decay the increased premium.

My goal is to consistently collect credit from rolling the strangle as the underlying stock goes up and down. Using SPY at around $400 a share, I’ve recently found I can roll out weekly from around 25 DTE to 32 DTE and collect a $2 premium net credit, or about 0.5% of my cash secured capital. A year of that would be 25% return, which would make most conservative traders very happy. I can’t do that every week because sometimes a big move sends my positions into a tested area where I need to adjust strikes to recenter and the net credit is smaller.

Many traders don’t mind the assignment either way and happily wheel between covered calls and cash secured puts, but I like to try to keep both options of the strangle in this situation if I have the capital available to support a position. The strategies aren’t that different, but with a covered strangle, I can adjust easily no matter which way the market goes, and not have to buy and sell my shares of stock.

Assignment due to dividends is a possibility, which I find as a minor annoyance, but actually manageable. Remember that the calls are covered, so worst case when a stock goes ex-dividend and is close to being in the money, it will get called away. Then, a trader can use the wheel strategy and sell a put to get the shares assigned back. I avoid this by adjusting strikes so my calls are far enough out of the money that it never makes sense for an assignment to occur. I also don’t hold options that are near expiration and most likely to get assigned, especially at dividend time. But again, since the calls are covered, there is no real risk, just the selling of shares for a profit.

Level 0 Strangle?

Brokers have different levels of option trading permissions. I’ve written about this in my pages on different levels of risk and comparing risk. Level 0 is the lowest level of risk and easiest for a trader to be permitted. Most brokers consider covered trades as Level 0, although some brokers may have a different name for it. The reason most consider this option permission level as zero is because it is actually less risky than holding the same amount of stock, whether the position is a covered call, a cash secured put, or a covered strangle. That means less risk for the broker and for the trader. This makes covered option trades a favorite of conservative traders.

Since we are talking about strangles, how different is the risk of a covered strangle from a margined and naked Level 3 strangle, or a futures option naked strangle? The big difference is that there is nothing covering the risk in either direction with higher risk levels of strangles. There is absolutely no limit to the risk to the upside. Prices can keep going up, and a naked short call keeps losing no matter how high prices go. On the downside, most brokers only require around 20% of the capital at risk for a trade to be executed. So losses can greatly exceed the initial capital in a big downturn. In contrast, a cash secured put can’t lose more than the cash required at the start of the trades, because 100% of the value of the stock that would be assigned at the strike price has to be in the account. The highest strangle risk is from using naked futures options which utilize SPAN margin, and even less capital required, which also means even more potential for crazy losses if the market gets out of hand.

Because Level 0 covered strangles have several times less risk than naked Level 3 strangles, they provide a great way to get used to trading strangles. Traders can get familiar with the mechanics of strangles without the risk of naked positions. And covered strangles are still a viable way to make a return on investment that often beats the market, particularly in flat and down years.

I’ve written about different types of underlying securities, but covered strategies including covered strangles can only use stocks or ETFs, because a trader can’t own an index. Stocks and ETF are familiar to most all traders, and many aren’t even aware of index or futures options, so covered strangles mean nothing new to learn.

Probably the biggest issue for trading covered strangles is the amount of capital required. For my favorite ETF underlying, SPY, trading at $400 a share, the shares alone are $40,000 and selling a cash secured put ties up approximately another $40,000. So, for the smallest 1 contract increment of a covered strangle, a trader needs $80,000. For many traders, this is out of reach. A low priced stock might be more of a practical choice, so Ford Motor (F) trading recently at around $12 a share needs about $2,400 to get a covered strangle going.

Because individual stocks typically have more implied volatility than ETFs, there is more premium to collect, making individual stocks good candidates for covered strangles. Since the trade is covered and risk is slightly less than owning stock outright, it can be argued that covered strategies are best used with individual stock. Assignment is more likely in individual stocks because outsized moves are more likely, but the position is covered by cash and stock, so assignment is just a feature of holding a covered strangle. For traders who haven’t experienced assignment on a naked position or spread, assignment on a covered position is a much less stressful way to be introduced to the concept.

It may appear that I’m portraying the covered strangle as a beginner option strategy, but it is really a sophisticated method of reducing risk. Most people are scared of options because they are considered risky. The covered strangle is one strategy that uses options to reduce risk compared to owning equivalent shares of stock. Many conservative investors utilize covered strategies, not to speculate, but to lessen the volatility of their returns. Most financial planners will give you a deer-in-the-headlights look if you ask about this strategy even though it reduces risk and should be a common tactic. But most financial professionals are completely unaware of ways to use options to reduce risk. So for that reason alone, don’t ever think of covered option strategies, including the covered strangle, as a beginner strategy. I think of it more of a way to be fully invested and sleep better at night strategy.

Many people are buying and selling options with zero days to expiration (0 DTE in option lingo). But is this a good idea? Are there strategies that actually work? Or is this just gambling? Well, like many things in options, it depends. There are strategies that have been successful with years of history, and we’ll dig in to discuss them.

In 2022, the option exchanges rolled out options on a few indexes that expire every day of the trading week. This has caused a frenzy of option trading by individuals who are trading a variety of expiration day strategies every day. Many people are buying and selling options with zero days to expiration (0 DTE in option lingo). But is this a good idea? Are there strategies that actually work? Or is this just gambling? Well, like many things in options, it depends. There are strategies that have been successful with years of history, and we’ll dig in to discuss them.

Over the past several years, the frequency of option expirations has increased dramatically, particularly for the major indexes, the S&P 500, the Nasdaq 100, and the Russell 2000. Initially, there were only monthly expirations that expired on the third Friday of the month. Options expiring every Friday were added several years ago, and Monday and Wednesday were added a few years back, and finally in 2022, Tuesday and Thursday expirations were added. Trading volume has grown exponentially, and trading on options expiring within the next few days are now the majority of option trades. Clearly, expiration day trading is very popular.

I’ve been exploring trading strategies for expiration day for several years, going back to when we started having expirations available for Monday, Wednesday, and Friday. I’ve discovered that 0 DTE is not for everyone, can have many elements of gambling for many, but has a few strategies that have a positive expectancy of profit.

Things to know about 0 DTE

First off, 0 DTE requires a different mindset than longer duration trading. Profits and losses explode in minutes, making the importance of having a plan critical. Options in general require strategies and planning, but 0 DTE is significantly more volatile. So, for traders that can’t handle huge swings in value over very short periods, 0 DTE may not be a good place to go.

For traders that do trade 0 DTE, I highly recommend keeping a log of all trades to be able to evaluate whether the strategy being used is actually working. Some trades have fairly high win rates, but have big losses when they lose- a log will help a trader determine if the wins outweigh the losses over the long run. Also, keeping note of what went well and what went wrong will help a trader learn from success and failure. I can tell you that most traders that fail do so by not sticking to their own rules for managing risk.

One key consideration is the Pattern Day Trade Rule that applies to accounts with less than $25,000. Federal regulations prevent small accounts from opening and closing the same position the same day more than three times in any 7 day period. Doing so will place severe limits on the traders account. If you have an account with $25,000 or less, or even just slightly more, you need to be very aware of this rule and how it works before even thinking about 0 DTE trading or any short duration in and out trading strategies.

There are a number of ways to trade 0 DTE. Some traders try to get in and out, while others hold a trade to expiration at the close of the day. Some are net buyers of options, what I will call debit trades, while other are net sellers, or credit traders. I say “net” because many strategies involve trading spreads, buying one option and selling another, generally the more expensive being hedged, protected, or partially financed by the cheaper option.

When options are expiring at the end of the trading day, all the characteristics of options are sped up. From a data driven standpoint, there are three key Greeks to consider. The two most obvious are Theta and Gamma which essentially battle it out for the day. But Vega also plays a key role, as big moves spike up Implied Volatility and option’s premium, and calmness can sap premium almost as fast. With hours or even minutes until the options expire, the Greeks’ calculations stop meaning as much as the concepts behind them.

Options sellers are banking on Theta eating away the premium as the day progresses. If the option ends out of the money at the end of the day, it is worthless. On the other hand, Delta will end the day at either 100 or zero and is likely to swing huge amounts during the day, which is the measure of Gamma, the change of Delta. So option buyers are looking for options to get in the money and run way up in value.

Since we are talking about expiration, it is important to understand the implications, which vary depending on what underlying the option is based on. Remember, there are four types of underlying securities, and at expiration the differences really stand out when an option expires in the money. For stock and ETF options, in the money options are settled with shares, which may not be the best outcome for day trading. In addition, while expiration option trading ends at the closing bell, expired stock and ETF options can be exercised until midnight, so even options that end trading out of the money still might be exercised if market conditions change after hours from news or earnings impact. Index options are much more straightforward. Index options are cash settled based on the price of the index at the closing bell. Because of this, index options, like SPX, are generally the preferred trading vehicle for traders holding options through the closing bell. Futures options settle with futures contracts unless the futures contract is also expiring the same day. However, futures options are assigned based on the price at the closing bell, not any after hours moves, so a trader knows at the bell whether there will be an assignment or not. So switching between underlying types for 0 DTE trades in not a trivial decision.

As mentioned before, because 0 DTE trades can rapidly change in value, having a mechanical trading plan becomes critical for consistent success. Most traders that trade short/selling strategies use stop losses to keep losses from getting out of hand, and long/buying strategies use some type of trailing stops or rolls to protect winning positions and keep upside unlimited. There are a few trades where holding to expiration (no matter what happens) could be considered, but I think 0 DTE are best managed by active trading based on market action.

So let’s get to it. Let’s discuss some typical strategies, both from the long and short side, considering what it takes to be successful.

Selling options with 0 DTE

Most 0 DTE option sellers I know actually sell spreads to define risk. Selling naked options on expiration day simply requires too much capital and carries too much risk for the average trader. The width of the spread can vary based on the strategy or capital available to the trader, but wider spreads tend to decay faster than narrower spreads. These trades are expected to win a high probability of the time, but to avoid severe losses, stop losses are also critical parts of the strategy.

While there are many variations of these strategies- different times to enter and exit, trading one side or both sides (puts and/or calls), entering or exiting all at once or legging in based on the market, the core of the strategy is the same. Sellers want to sell at a relatively high premium and buy it back for less or even let it expire worthless. I’m going to focus in on two common strategies that I have had success with and 0 DTE trading friends have done successfully- a wide Iron Condor and an Iron Fly. For discussion, let’s assume that we are selling spreads directly on the S&P 500 Index, ticker symbol SPX.

0 DTE Iron Condor

Iron Condors on expiration day seem to perform best way out of the money, selling options with 10 Delta or less and buying 30 to 100 points further out of the money. Greek calculations for 0 DTE can be flaky and vary widely, so many traders are more comfortable choosing strikes based on the premium available. For example, a trader may sell the lowest put strike that sells for over $1.00 or maybe over $1.50, and buy the put that sells for under $0.75 or $0.50. For perspective, you can estimate the expected move at any time in the day by adding the premium of the at the money put and at the money call. Generally, these strikes are between 1.5 and 2 times the expected move for the put being sold and another half expected move further for the put being bought as a hedge. So, it’s highly likely that the strikes will expire worthless.

Similarly, we do the same thing on the call side, selling a call and buying a higher strike call for less. If we choose similar Delta values, the premium for each call will be less, but the difference in premium may actually be more if we have the same width wings. It is a matter of preference as to whether to try to collect as much on the call side as the put side.

The risk vs reward for this set-up is the net premium difference between what was sold and what was bought and the difference between strikes. For example, if we sell a put for $1.50 and buy a put at a strike price 40 points lower for $0.70, we are risking 40 to make 0.80. Then, if our calls were sold for $1.20 and bought for $0.40, we have another 0.80 on another 35 wide spread. So in total we have 1.60, but still only 40 risk because the options can’t expire in the money on both sides. Actually, because the options are for a multiplier of 100, we risk $4000 to make $160. So, if all goes well, we make a 4% return on the capital needed in one day. Some traders sell slightly closer strikes to try to collect more premium, and others sell for less to improve probabilities.

While probabilities are fairly high that the strikes will end up out of the money, we never know for sure, so we have to protect our capital. Most traders I know use a 2x stop loss on each side. They limit their loss to twice the premium they collected on each side. So, if a put was sold for $1.50, losses are limited to $3.00 by entering a stop loss on the short put at $4.50. While a stop can be entered for the price of the spread, it isn’t recommended because during the day prices can vary in weird ways and stops can trigger on spreads when the price hasn’t really moved much. I’ve read numerous posts of traders who were frustrated by a stop that was executed when there position was in no danger because of a rogue quote. If possible, it’s best to have the stop trigger based on the bid price of the option if your broker allows it- for the same reason- to avoid bad quotes triggering a stop.

It can be frustrating when a stop triggers just as the underlying price hits the high or low of the day and reverses. A trader looks at this and thinks, “Gee, if I wouldn’t have triggered the stop, my option would have expired worthless. I took a 2x loss when I could have had a gain.” Unfortunately, a trader never knows when the price will reverse and when it will keep going. The goal is to stop our loss at 2x and not let it get to 10x or 20x. We can recover from small losses, losing all the capital of a spread trade can be devastating.

The Iron Condor is a 4 legged trade, so if one leg is stopped out, we still have three legs. On the side where the stop occurred, the long position will have gained value, although not as much as the short strike lost. We can hold the long strike in the event that price keeps moving, making the long strike more valuable. However, since the strike is likely still well out of the money, it is likely to expire worthless and probably is best to be closed out soon after the short strike stop occurs.

When we are stopped out on one side, it is even more likely that the opposite side will expire worthless. However, there is a small possibility that price action could reverse and move far enough to stop out the other side as well. For that reason, some traders will close out one side if the net premium has decayed 80 or 90% of the way while there is still a lot of time left in the day. The choice is take risk off the table, or hold out for that highly probable last 0.25%. Again, it’s personal preference.

So, let’s look at the various potential outcomes of our $1.60 Iron Condor: 1. most likely (~70%) both sides expire worthless $1.60 profit 2. sometimes (~25%) one side is stopped out and the other expires worthless ($3.00 loss on short stop, $0.20 gain on long, $0.80 profit on other side) $2.00 loss 3. rarely (~5%) both sides stopped out, assume no net gains from long strikes so $6.00 loss ($3.00 each side) Adding all the probabilities together, we get an average return of 0.33 profit, or $33 on our $4000 capital. That’s just under 1% per day.

Can some traders do better? Yes, there are lots of variations that some traders believe give them a better advantage. But lots of traders do worse. Why? Because managing trades while sticking to a plan isn’t easy for most traders.

How can the trade be varied? Some traders enter the trade at different times in the day. They may enter at market open and again a few hours into the day. They may open on just one side based on technical indicators predicting movement in a certain direction. They may add based on one side based on market movement. They may have plans to add new positions when an old one is stopped out. Which variations work and which ones don’t? The probabilities are essentially the same but can be tweaked by collecting a little more or less in each trade.

Some may wonder why we wouldn’t just look at stopping out the whole Iron Condor when it loses twice the premium collected instead of managing each side separately. While it could be done that way, the challenge is that each of the legs of the trade are very dynamic in their values and the relationship between them changes dramatically during the course of the day. If the trade is opened early in the day, it is likely that by the final hour of the day only one position will have any meaningful value. Also, managing puts and calls separately allows traders to add and take away positions on either side independent of how they treat the other side.

On an ideal day for this trade where the market doesn’t move much after the Iron Condor position is opened, all the legs will decay proportionately and have little value left by the afternoon period a few hours before expiration. This is because expectations of the remaining move for the day will decrease and the price distance that was 1.5 times the expected move will become 3 to 4 times the remaining expected move. Since the probabilities are exponentially smaller of being tested, the premiums simply evaporate. One doesn’t have to wait to the very end to see the result.

Other days Iron Condor traders may see the price creep around moving toward one of their short strikes. Big moves early in the day can quickly lead to executing a stop, but the nerve-wracking position is the one is close to stopping out all day as the price moves ever closer to a strike price but not close enough to trigger a stop. For some traders this is stressful, for others fascinating. To avoid stress, many traders set their stops and go on about their day knowing that the market will decide whether the trade wins or loses.

Iron Fly 0 DTE trades

A completely different approach to capturing decay on expiration day is selling an Iron Butterfly or Iron Fly as it is more commonly called. The Iron Fly is created by selling an at the money call and an at the money put and buying protective wings outside the expected move of the day. The trade simulates a straddle, but defines the risk as the width of the wings to keep buying power reasonable. Most traders try to open these trades soon after the market opens and get out fairly soon, taking advantage of early morning premium decay as the market settles in.

As discussed earlier, the at the money put and call premium imply an expected move for the remainder of the life of the option. How big the expectation is varies from day to day. For example, on days when the Federal Reserve announces interest rate policy, the expected move is much higher than other days. Other anticipated news events can also trigger uncertainty about pricing changes to expect later in the day, driving premium higher. Other days, little news is expected and low premiums reflect that. So setting up this trade requires a review of prices to pick wing strikes that are appropriate.

Generally, most traders look for Iron Fly wings that are 1.5 to 2 times the implied or expected move. For example, if the total premium of the at the money put and call is $30, one might choose to buy puts and calls $50 away from the money. These should be fairly cheap compared to the at the money strikes. The idea is that there isn’t much decay left, these long options are simply protection from a sudden outsized move. An alternative is to use a set price for one or both of the longs, like $1 for the long call and buying the equidistant long put, which may cost slightly more due to pricing skew.

The most common management strategy I’ve seen for this trade is to set a win target and an offsetting stop loss, and let the odds play out. Iron Fly sellers pick either a percentage target or a dollar target for profit and typically set the stop loss at twice the win target. For example, one trader may target a profit of 5% of the premium, while another may target $1.50 profit every day. There’s logic for either approach, big values may hold value until the news event that is expected to move price, while low values may decay slowly. The key is that the bigger the target, the longer a trader is in the trade.

Why not go for it all and let the position expire? First of all, one short strike will definitely be in the money at expiration while the other short strike will be worthless. The day to day variation in results would be huge, perhaps making 50% return one day and losing 140% the next day. In addition, most studies I’ve seen on this approach suggest that this is a net losing trade over time.

The idea of getting in and getting out is that there are periods of time during the day, primarily at the open, when the level of uncertainty drops significantly in a matter of minutes or a few hours. Even with price movement, expected moves drop faster and the premium of the Iron Fly decays for a win.

In practice, the Iron Fly can tolerate a move of a few strikes up or down initially without stopping out. Early in the day the market often moves around searching for a price to stabilize on. The Iron Fly seller expects that movement to be small enough most days that a stop isn’t triggered and the settling price is close enough to the price where the trade started that the profit target can be achieved.

Setting a stop order or profit limit order is trickier with an Iron Fly than with the Iron Condor. The issue is that with the Iron Fly, a price move of the underlying generally impacts three of the four legs. One short goes into the money and the long on that side starts increasing in value, while the other short starts decreasing in value. The long on the untested side goes from low value to nearly worthless and isn’t a factor. A set and forget stop strategy would be to set a stop for the whole four legs, but triggers and fills can be inconsistent. Another approach is to watch the direction of price and set a stop for the three legs that are most impacted. Another is to set a mental stop and manually close if the price goes beyond your mental stop.

For example, let’s say we open an Iron Fly for $30 credit and target $1.50 profit. We can enter a limit buy to close order to buy the whole position back for $28.50. We could alternatively place a stop loss order at $33. Some brokers allow a bracket order that combines the two orders into one for a situation like this. If we want to watch and mentally manage the order, we may choose to only close the three legs that have meaningful value.

Time in the trade can vary from minutes to hours. Some days the price sticks right where the Iron Fly was sold and the price decays in 5-10 minutes. Other days, the price may grind away varying premium between the profit and stop targets for hours. Many traders set a time limit- if the trade doesn’t hit a stop or profit target in 2 hours, close it and move on.

Time to enter is a bit of a personal preference as well. Some traders try to enter within seconds of the market open when there is the absolute most premium available. Others wait five to fifteen minutes for the initial big move to stop. Some do just one of these trades a day, while others open several at different points in the day. Some avoid Federal Reserve days while others embrace them. There are advantages and disadvantages to each way of entering, but often it comes down to comfort of the trader with a chosen approach, the probabilities are similar.

Over time, the math is fairly simple with this trade. We need to win more than twice as often as we lose. The studies I’ve seen show this as a net winner. The other key is stay mechanical and respect identified stop values. Most people who fail at this trade do so by getting sloppy with their stops and hoping for prices to reverse while the loss multiplies. Discipline can’t be overstated.

Long Strategies for 0 DTE

Buying an option on expiration day requires a strategy that can overcome the rapid time decay of the option purchased. Since there are huge volumes being bought each day, there must be some validity to this approach.

Buy 0 DTE Straddle

One simple approach is to buy a straddle and hope for an outsized move. This is essentially the strategy discussed in the post on the 1 DTE Straddle I’ve written about separately, just done on expiration day. The difference is that at 1 DTE, there is overnight movement that may impact pricing, while once the 0 DTE trading day has started, we only have the day’s price movement to consider.

This strategy is essentially the opposite of the Iron Fly strategy and counts on movement of price to exceed time decay. Since risk is limited to the premium paid, there isn’t much value in selling wings, which would limit the upside of any move.

When would one open a 0 DTE straddle? Perhaps right at the open, looking to capture a big early morning move. Or just before a big announcement, like the Federal Reserve interest rate announcement or press conference. Or maybe at a point in the day where there is time left but the straddle is just very cheap and a small move will make it profitable.

The biggest challenge is deciding when to get out both for winning and losing positions. The position won’t expire worthless, so should there be a stop loss? When a position wins, when is the profit enough to justify the strategy over time? Since the trade has theoretical unlimited profit, shouldn’t we preserve that potential? Tough choices, so thinking through a plan ahead of time for the situation is critical.