This post lists recent additions and changes to the website. For frequent users, this change log might be helpful to see what has changed from past visits.

The following is a listing of recent additions and changes to the site. For frequent users, this change log might be helpful to see what has been added new or changed.

January 13,2026: Added a new post on using a household balance sheet. Slightly off the topic of options, but something every trader should use in some form or another.

December 1, 2025: Added a new page on Best Option Order Entry Practices. Sometimes, it’s good to get into the nuts and bolts of trading a bit.

October 14, 2025: Added a new page on Rolling Credit Put Spreads. While I’ve written about this before, this is a more thorough version explaining how rolling works mechanically with put spreads.

September 17, 2025: Added a short post explaining that the site was back up after a week down. I appreciate the patience of all who had to wait, and the persistence of those who found ways to reach out to help get the site back up.

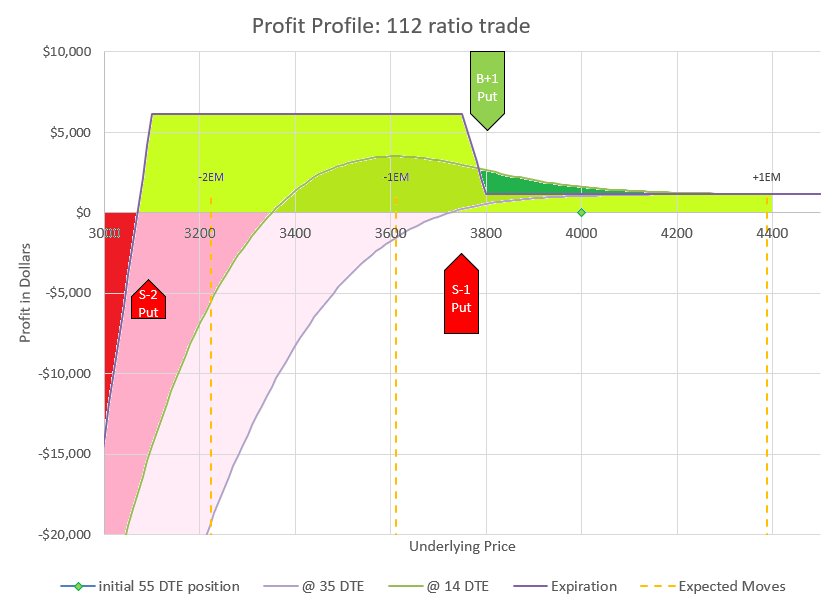

August 2, 2025: Added a page comparing the 111 and 112 put ratio trades. It’s been a year since the Implied Volatility blow-up that crashed so many naked traders, so it seemed like a good time to re-visit.

June 26,2025: Based on popular demand, I’ve added a page on selling covered call spreads. This strategy allows a trader to collect premium on existing shares without giving up all the upside potential if the stock goes up a lot.

March 13, 2025: Added an update to the Very Long and Very Short Diagonal Put Trade. This trade becomes truly unmanageable during extended down markets, making it an interesting concept to study and test, but not viable as an ongoing practical strategy.

February 9, 2025: Added a page with an updated write-up of the Delta Neutral Back Ratio Call Spread, as featured in the new YouTube video interview with John Einer Sandvand from ThetaProfits.com. This is an updated analysis from an earlier page on the same topic.

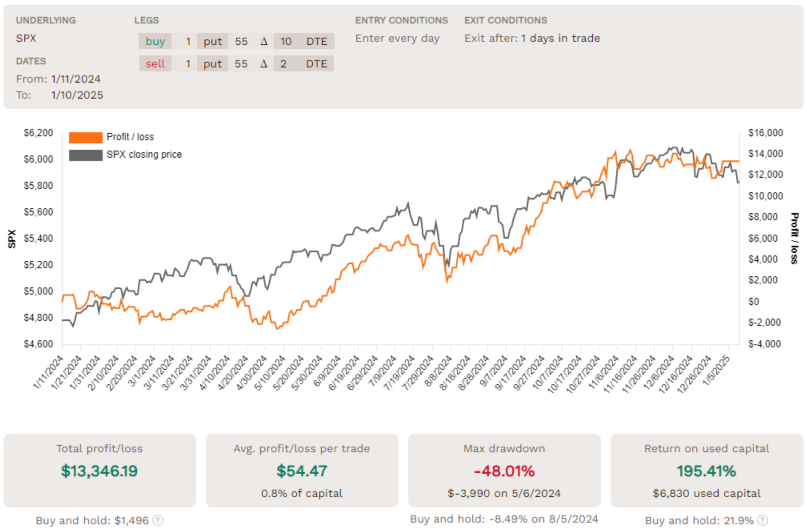

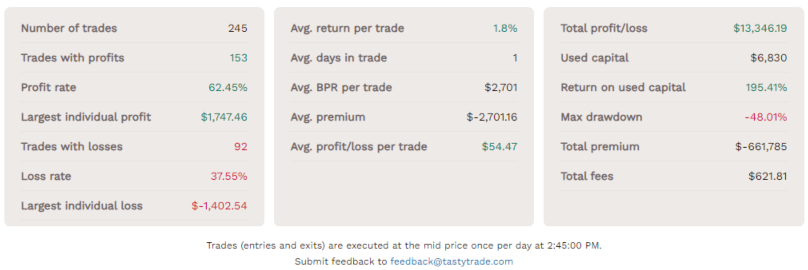

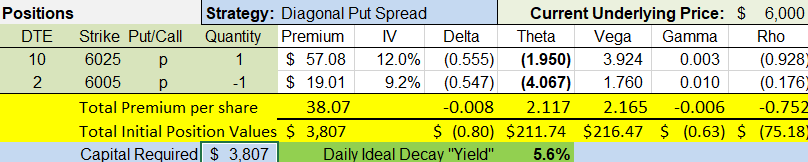

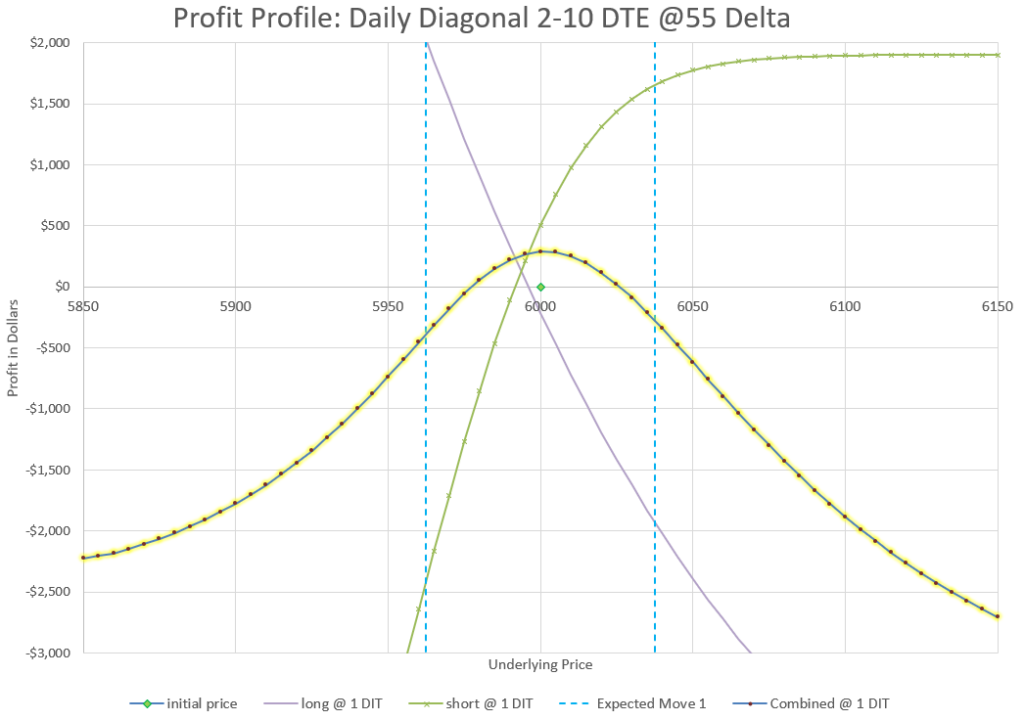

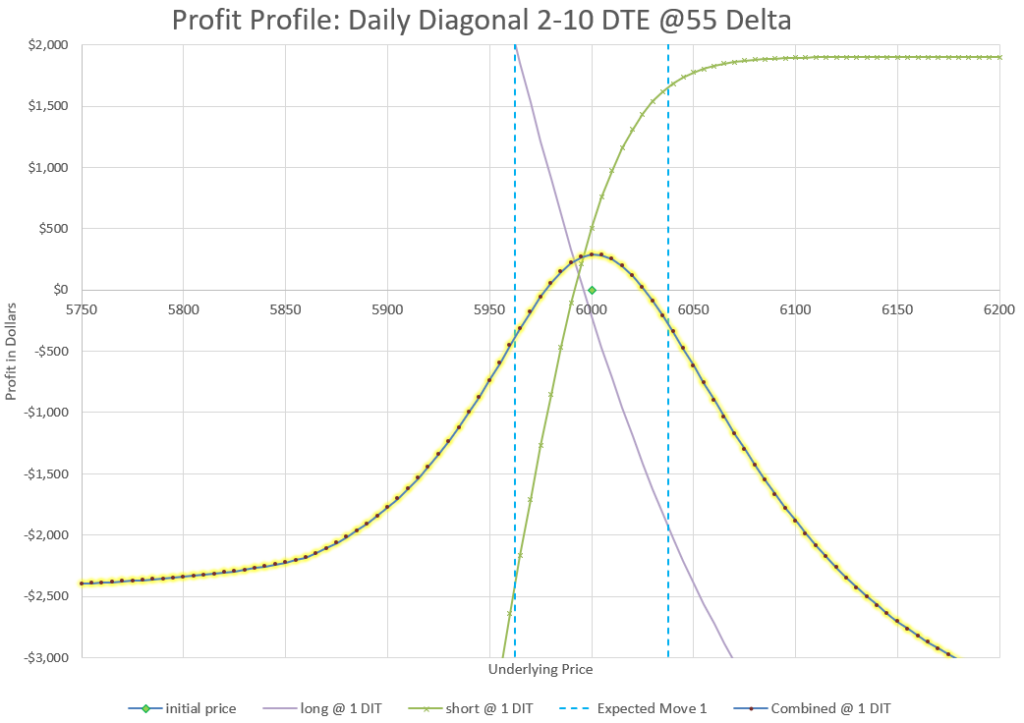

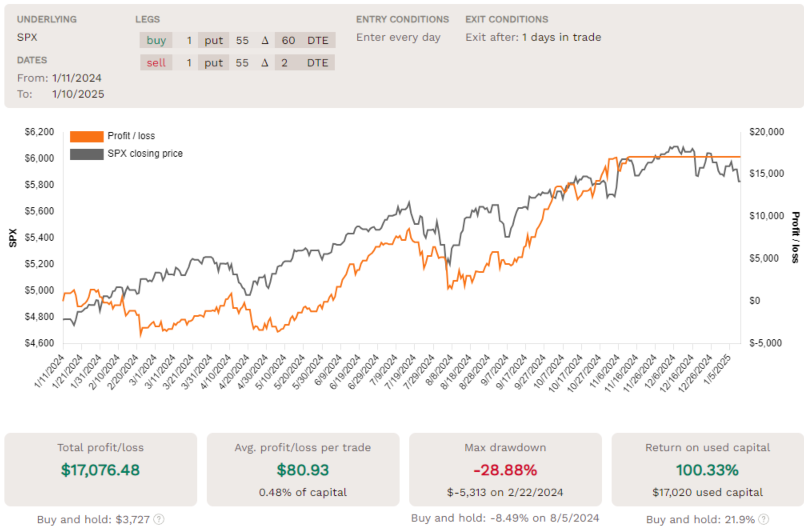

January 14, 2025: Added a new page on the Daily Diagonal Covered Put trade. This is similar to the earlier Very Long Very Short Diagonal, but with much shorter duration and less capital required. I even included a backtest.

December 16,2024: Added a new page for the Very Long Very Short Put Diagonal Trade. This trade, also a version of a “Poor Man’s Covered Put” has much more to than what one would expect at first glance. However, this trade has elements of almost every aspect of options there is, so a lot to study for every option trader.

October 2024: Lots of new comments from readers and responses on various pages of the site. Keep those questions and ideas coming!

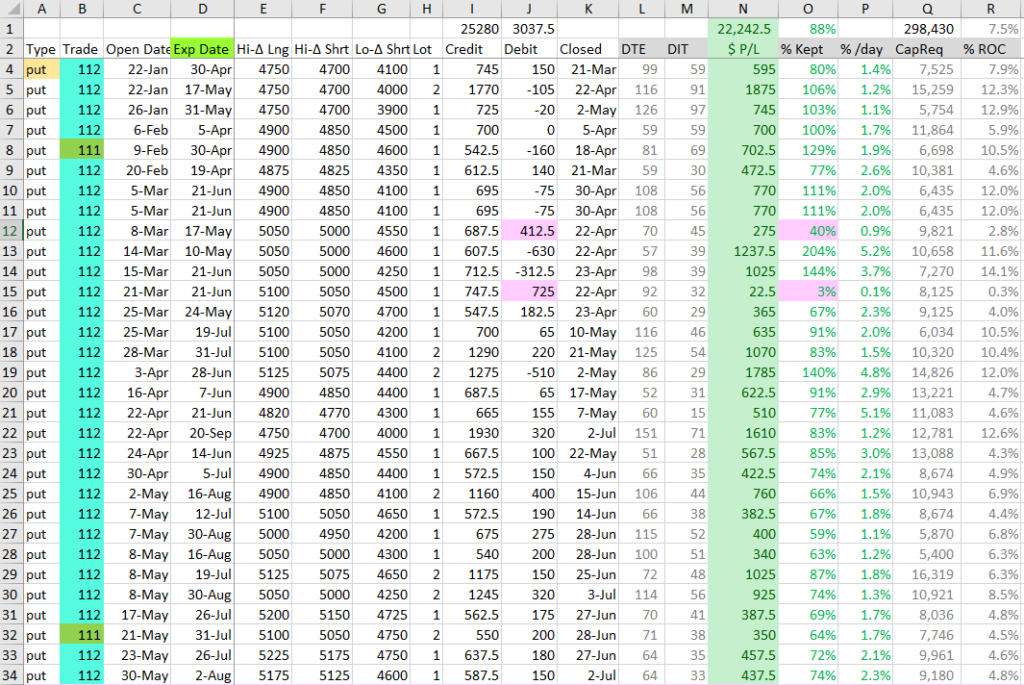

August 24, 2014: Added an update to the page about 100% success in the 112 trade to highlight the issues with the August 5 volatility debacle that did wiped out many 112 traders.

July 23, 2024: Added a new post sharing results from the 112 trade in the first half of 2024. 100% success.

July 2,2024: I added a new page contrasting debit vs credit option trading strategies. It’s one of a few considerations traders should consider when picking strategies that work best for their style of trading.

May-June 2024: Lots of new comments and replies came in from readers. Always good to hear from folks with their questions and comments.

December 30, 2023: I added a couple more books to the Resources page. I also updated Tasty links for their new TastyLive.com URL.

December 20, 2023: Made a number of changes and additions to the home page of the site. With all the new content, it seemed like it was time to highlight some of the content that isn’t as obvious.

November 22, 2023: Added a duplicate post on the 1-1-2 Put Ratio Trade. I did this to capture the search engine traffic from the numbers of traders looking for information. So, whether it’s 112 or 1-1-2, there’s a write-up. Just read one or the other- they are the same.

November 14, 2023: Added a page on the 112 Put Ratio Trade. While I mentioned it a bit in the post on the 1112 Put Ratio Trade, I decided the naked option version deserved a write-up of its own.

September 19, 2023: Added a page on Covered Calls. Yes, I know I just wrote a post on the same subject. (Secret note: the write-ups are exactly the same. This is actually a test to see if pages do better than posts in getting search engine connections. Universally, my most read articles are always pages, but maybe that’s just a coincidence. Most readers would never recognize the difference between a page and a post, but posts are supposed to be part of an ongoing blog, while pages are more “permanent.” I’ve used them interchangeably, and I want to make a data-driven decision on what the impact of that choice is.)

September 18, 2023: Added a post on 5 Bullish Call Trades. This is the culmination of a series of trades that I felt like I had overlooked regarding data driven ways to utilize calls in a bull market without absorbing too much time decay. With the market in what appears to be a bull market, it was time to focus in on this topic. 4 of 5 of these trades have recent extensive write-ups that were completed in the past 3 months.

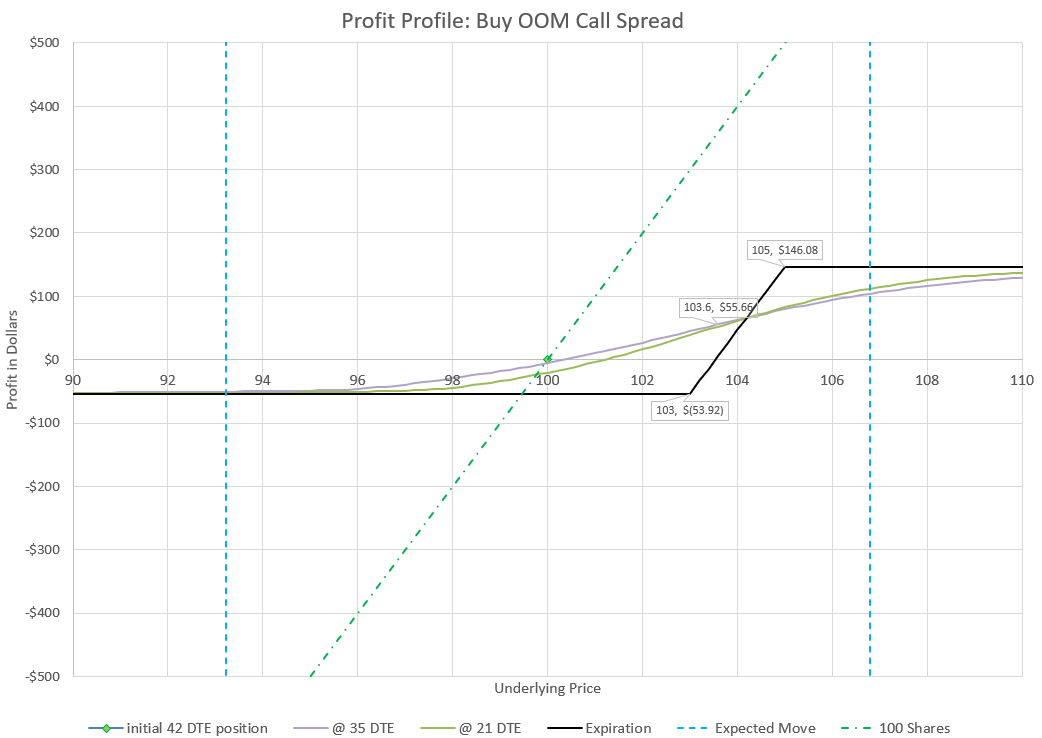

August 4, 2023: Added a post on Buying Out of the Money Call Spreads. This is a strategy that would appear to most option traders who mostly sell options to be a sure loser, but back-testing shows it to be quite profitable over time.

July 26, 2023: Added a post on the Poor Man’s Covered Call, a low cost variation of a Covered Call, based on selling a call against an in the money long call that acts as a replacement for stock. So, a bit of a cross combination of the two most recent previous write-ups.

July 25, 2023: Added a post on Covered Calls. Not sure why I never wrote one before, but given it is one of the most popular option trades around, I thought it was time to weigh in on it with a level of detail that isn’t available many places.

July 5, 2023: Added a post on Replacing Stock with a Call Option. When markets are going up and IV is low, buying calls can be a good way to get in at a low cost. This post goes into more detail.

June 19, 2023: Added a post on Underlying Security vs Risk Permission. There are a lot of factors to picking the type of security to buy or sell options for a specific type of trade. This post digs into what to consider and why some approaches may be better than others.

May 24, 2023: Added a post on Trading Options while working a Full Time Job. I went back to work this year and changed my trading routine. I know many readers can relate, even if they just want to make better use of their time.

May 20, 2023: Added a chart to the 1 DTE Straddle post to show profit and loss at various times of the day.

May 17, 2023: Added a post on Covered Strangles, a conservative options trade that reduces volatility with higher probability of profit than owning an equivalent amount of stock outright. It’s my first deep dive into Level 0 option trades, something I’ve had a number of requests to address.

February 27, 2023: Added a new Phone Stock Charts page with stock price charts formatted for a smart phone, and potentially screen-cast onto a monitor or TV. Not for everybody, but if this is something you are looking for, like I was, you’ve found it.

February 27, 2023: Updated the Current Prices page with more interactive charts, replacing those from a previous provider that had security flaws.

February 26, 2023: Added a post on the topic of 0 DTE trades.

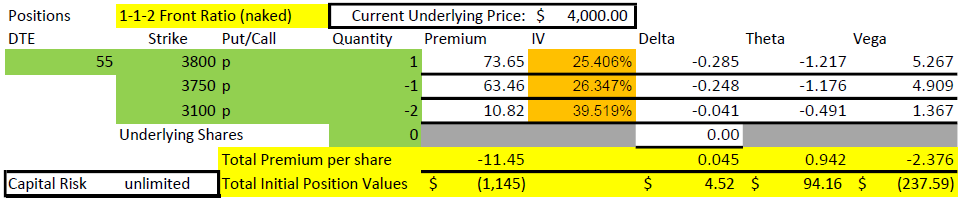

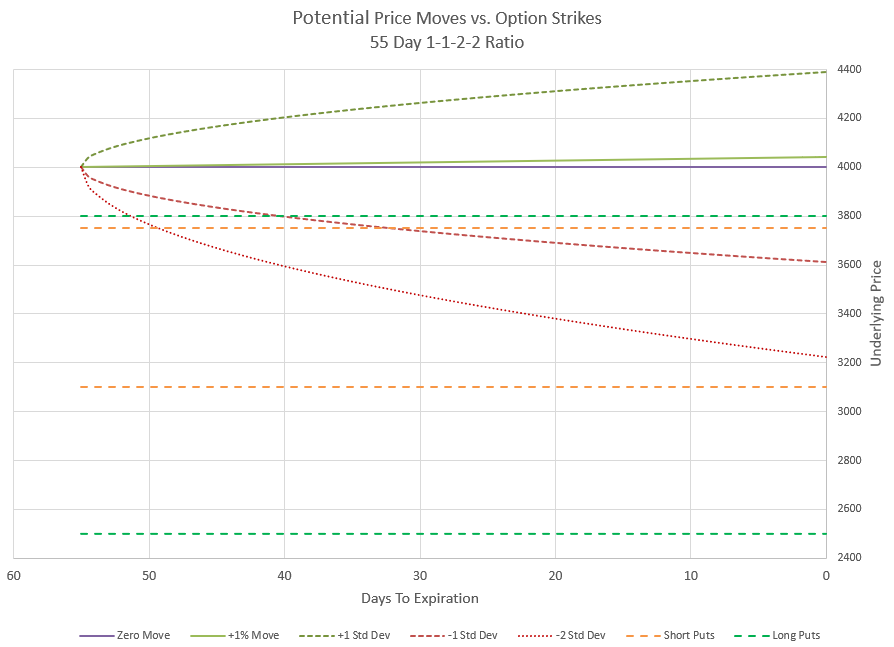

January 16, 2023: Provided responses to a couple of great reader comments and questions regarding the 1-1-2-2 trade.

January 13, 2023: Added a new post on my 2022 learnings.

December 23, 2022: Added a post regarding the best Delta for ROLLING put spreads. This is a new topic that I had curiosity about from years of observing that some rolls do better than others, and I couldn’t figure out why.

November 28, 2022: Accepted an extended comment to the page Rolling Iron Condors and added a response. Comments are always welcome and appreciated. Note that comments from first time commenters must be reviewed and accepted to keep those crazy spammers from ruining the site.

November 9, 2022: Response added to a comment about how to roll a back ratio call spread up or down to get back to Delta neutral.

November 3, 2022: Added a new page on Options Margin Usage. In this page, I compare different types of margin available for option traders and the benefits and risk of each.

October 15, 2022: Worked with the ad provider to reduce the number of ads on the site and make them less obnoxious. Should be no more pop up adds when changing pages, and less ads per page.

September 30, 2020: Added a new page explaining how brokers permit different levels of risk in option trading.

the S&P 500 index is very appealing but most traders don’t know there are at least 7 different great choices for options tied to the index

For many new options traders, trading the S&P 500 index is very appealing for a number of reasons. But most new traders are not aware that there are at least 7 different great choices for options tied to the index. Most have multiple expirations each week and are very liquid. Each choice has unique differences from the others that may make it appealing in certain circumstances. For a long time I was only aware of one way, and when I now tell others about these additional choices for options, it’s usually a pleasant surprise.

Background

The S&P 500 index is the most quoted benchmark of the stock market for good reason. It is made up of the 500 largest US publicly traded companies. The index is weighted by market capitalization of each firm, so the largest companies have more impact on the index than smaller ones. In fact, as of this writing, the seven largest firms are responsible for 30% of weight of the index. While the news media often leads market reports by sharing the Dow Jones Industrial Average, most traders and asset managers pay little to no attention to the Dow because it only includes 30 stocks and has a bizarre price weighted averaging system that gives the most weight to companies with the highest price per share.

If a trader can choose only one investment to own, some form of the S&P 500 index would be the most logical choice. When selling options, unexpected moves outside of expectations can lead to large losses. Many studies have shown that the S&P 500 index is much less likely to have an outsized move than individual stocks or even other indexes. TastyTrade has done numerous studies on this that are free to review. So options on the S&P 500 index can be a large part of a trader’s strategy. Understanding the variety of choices for trading options on the S&P 500 can be very helpful for traders of all experience levels.

Mutual Funds?

Almost every employee retirement account offers a mutual fund that mimics the S&P 500 index. While mutual funds are great for retirement accounts that rarely change holdings, they aren’t that useful for trading in general, and specifically not for options. There are literally dozens of mutual funds based on the S&P 500, but they share the same trading issues- they only trade at the closing price of the day which isn’t known until after a trade is submitted, and there aren’t options on any of them. Active traders want to be able to buy and sell at any point in the trading day and have options for hedging or amplifying returns, so mutual funds just won’t cut it.

Exchange Traded Funds

In recent years, exchange traded funds (ETFs) have grown in popularity. These funds are structured to match the holdings of underlying indexes or other trading strategies. The funds actually hold shares in the index that they are matching performance with. By far the largest ETF is the SPDR S&P 500 ETF Trust, which goes by ticker symbol SPY, and follows the S&P 500 index. It is priced at approximately 1/10 the price of the index per share. So, if the S&P 500 index is priced at 4500, the SPY ETF will be priced around 450. The SPY price isn’t exactly 1/10 of the S&P 500 index price, but slightly less by varying amounts. The variations are due to fees that come out of the ETF, and the impact of dividend payouts. SPY pays dividends once a quarter, and the price of SPY gets closer to 1/10 of the S&P 500 index as the dividend payment approaches and then drops after the dividend is allocated. Generally, the variation is less than one dollar in SPY, so if the S&P 500 index is trading 4500, SPY is likely to actually trade at somewhere between 449 and 449.50. For most traders, this difference isn’t a big deal, but just a minor factor to be aware of when comparing SPY to the S&P 500 index. Because of its name and ticker, SPY is often referred to as the “Spiders.”

SPY option contracts are based on 100 shares of SPY. If an option is exercised or assigned, the option seller will either be forced to buy or sell 100 shares of the SPY ETF. Because SPY pays a quarterly dividend, traders who sell calls on SPY need to be aware of the risk of having the call option exercised on dividend day. If a trader has a call near expiration that is at the money or in the money, it will likely be exercised because the dividend can be captured by the owner of the stock. If the call seller doesn’t have shares to be called away, and the option is executed, not only will the seller be short shares of SPY, but the seller will have to pay the dividend to the broker that they are borrowing the shares from. Only call sellers have to worry about this, but it is a real consideration four times a year.

Both SPY and options on SPY are extremely liquid with bid-ask spreads normally at one penny. I’ve found option trades that include four legs, can usually be filled immediately for two cents away from the mid price of the combined bid-ask spreads of all the legs. Options are priced in increments of one cent, so pricing can be fairly precise. SPY options have 3 expirations per week, with contracts for every Monday, Wednesday, and Friday. Adjustments are made for holidays when markets are closed. Every expiration has dozens of strikes, going several expected moves above and below the current price of SPY.

While SPY isn’t the only ETF to track the S&P 500 index, it is the predominant one, and really the only ETF to really consider for trying to match the performance of the actual index. There are a couple of other ETFs to consider that are designed to magnify or reverse the performance of the S&P 500 index. For some strategies, these might be helpful.

UPRO is an ETF from ProShares that is leveraged to deliver 3x the performance of the S&P 500 index. Officially, it is called the ProShares UltraPro S&P 500 ETF. So, if the S&P 500 index goes up 1% in a day, UPRO will go up 3%. However, the reverse is also true- if the S&P 500 index goes down 1% in a day, UPRO will go down 3%. To keep this relationship working, the holding in the ETF are adjusted each night, so over time the ETF won’t exactly keep pace at 3x the performance. The ETF relationship is more precise day by day than longer term, but will be relatively close to 3x. UPRO has options expiring every Friday and is somewhat liquid with wider bid-ask spreads than SPY. Because of large swings in price, the ETF has occasional splits to keep the share price reasonable, and the daily adjustment of holdings can alter the precision of the leverage factor, so the share price isn’t consistently convertible to a multiple of the S&P 500 index.

The opposite effect is achieved from the SDS, or Proshares Ultrashort S&P 500 ETF. SDS is set up to delivery -2x the performance of the S&P 500 index. So, if SPY goes up 1%, SDS goes down 2%. Over time the price of SDS tends to get lower and lower, and a reverse split is needed to get the price up to a reasonable level. Options on SDS also expire weekly. Both SDS and UPRO options are based on 100 shares of the corresponding ETF.

Options on leveraged ETFs are much more volatile than on non-leveraged ETFs. Because traders of these options know that there is multiple times price movement, options are priced accordingly. Because of this, strategies with options can perform very differently than with options based on the non-overaged SPY. The switch from SPY options to UPRO or SDS options is not as simple as it might appear, so research thoroughly before jumping in to these unique options.

There are other ETFs that follow the S&P 500 index as well as others that leverage the S&P 500, but they don’t trade with as much volume, and their options trade less frequently. Why trade a product that is less liquid, with fewer options, and much lower option volume when a better choice is available? I see no reason to use anything but SPY, UPRO, and SDS.

There are also ETFs that represent sectors or portions of the S&P 5oo, or weight the 500 stocks of the index equally. So, for value vs. growth, or Finance stocks or Utilities, there’s are ETFs with options of every flavor. But none of those represent trading the full S&P 500 index, so we won’t dig in any further into those products, because the point of this discussion is ways to trade the benchmark index.

For most traders, SPY options are the only options on the S&P 500 index they use, and many traders aren’t aware of any other choices for trading options on the index. But, we’ve only just begun.

Index Options

Why trade options on an ETF based on an index when you can simply trade options on the actual index? Index options remove the ETF from the mix and link options directly to the index. For the S&P 500, there are two index options available, SPX and XSP. SPX is literally the S&P 500 Index, and XSP is the Mini S&P 500 Index.

Traders are often not aware of these ticker symbols or the fact that options are available for these two indexes. There are a couple of reasons for this. There is no way to actually buy or sell the actual S&P 500 index directly, a trader can’t buy or sell shares of SPX. Additionally, since SPX is an index and not a stock or ETF, many brokerages don’t show it as SPX. For example, Schwab lists it as $SPX. Other sites may show it as ^SPX or .SPX. The point is that you have to know what you are looking for to even find it. Since SPX is literally the S&P 500 Index, it is priced at the full price of the index. So, if the S&P 500 Index is at 4500, SPX is at 4500. They are exactly the same.

Okay, SPX is the S&P 500 index. But, what is the Mini S&P 500 index, you may ask? XSP, or the Mini S&P 500 is simply an index that is 1/10 of the S&P 500. However, unlike SPY, which is approximately 1/10 of the S&P 500 index, XSP is exactly 1/10 of the S&P 500 index. Why do we need an index that is 1/10 of another index? It’s all because of options and sizing of positions.

Options on SPX don’t represent 100 shares in SPX because SPX doesn’t have shares. Instead, SPX options represent a value of 100 times the value of SPX. Think of it as if SPX had shares and the options represented 100 shares, even though there aren’t any shares. XSP options represent 100 times the value of the XSP. So, in both cases we still have a multiplier of 100 as we do with ETF options. This is where the similarity in options end.

One difference is that dividends are not part of the S&P 500 index. Many of the 500 stocks in the index pay dividends at various times throughout each quarter, and those payments have an impact on the individual stock price, which will then impact the price of the index. But the index has no mechanism to pay dividends because it is just an average of the prices of the 500 stocks it tracks and isn’t tradable itself. So, option buyers and sellers of SPX and XSP don’t have to consider dividends as an event, like traders in the SPY ETF.

Since index options can’t be settled in shares, they settle in cash when they expire. In many ways, this can be a lot easier. If an option expires $5 in the money, a call buyer will receive $500 from the account of the call seller at expiration because of the 100 multiplier. If an option expires out of the money, it is worthless and there is nothing to settle.

Cash settlement can be a bit confusing at first, so just realize that there is nothing to actually buy or sell from assignment- a put seller that is assigned doesn’t have to buy 100 shares, they just have to pay the difference in the current price at expiration from the strike price of the option. If the trader sold a put on a stock or ETF, they would be assigned shares that they would buy for more than the current price, which they could turn around and sell at a loss. Index options eliminate the step of buying and selling shares, and just settles the difference in price with cash.

Index options use European style option assignment, while stock and ETF options use American style options. American style options can be executed at any time by the option buyer, and this becomes a consideration for option sellers that have positions in the money before expiration. However, European style options can only be executed at expiration. So, sellers of index options don’t have to worry about having an early assignment before expiration, and buyers don’t have that option. And since index options are cash settled, there really isn’t an “option” at all. In the money index options are simply “settled” at expiration.

SPX options have lots of different expirations. Originally, these options only had expirations once a month on the third Friday of the month. Later, month end and quarter end expirations were added. Then weekly expirations every Friday were added. And now there are Monday and Wednesday expirations. Soon, maybe by the time you read this, there will be options expiring every trading weekday when Tuesday and Thursday are added.

One holdover from the original monthly expiration is that monthly index option expirations are different than all the other expirations in a couple of ways. First, and most importantly, monthly index options expire in the morning (AM) of expiration, while all other expirations expire at the close (PM) of trading. For SPX, there are actually two option expirations on the third Friday of the month, the monthly AM expiration, and the Friday PM weekly expiration. The settlement price for AM expirations of SPX is based on the opening trade price of each of the 500 stocks of the S&P 500 index. After each of the 500 stocks has traded on expiration morning, the prices are calculated to determine a settlement price for expiration. However, trading on the expiring option is stopped at the close of trading the day before. So, SPX option sellers and buyers are stuck with their positions from Thursday afternoon until Friday morning not knowing what the index price will be for settlement until the market actually opens and sets the price. For PM expirations, it is simpler, when the market closes, option trading stops and expiration settlement is based on the price of each of the 500 stocks in their last trade of the day. If you watch the price at the closing bell, you will see it change slightly by several cents after the close as all the different orders that execute at the market close get accounted for. The second way that AM and PM expirations vary with index options is that when the option contract is listed, monthly contracts use the ticker symbol SPX, while all other expirations use SPXW. The W is for weekly, even though the expirations may be quarterly, monthly, Monday, or Wednesday, and soon Tuesday or Thursday. So for S&P 500 Index options, just know that SPX listed options expire in the morning (AM) and SPXW listed options expire in the afternoon (PM). Either way, when you are searching for option listings, most brokers list SPX and SPXW options together under SPX.

XSP options are a more recent creation, and only have PM expirations. There aren’t different naming conventions either. Settlement works the same, with prices set by the final trade of each of the 500 stocks of the index when the market closes.

Another difference between SPX and SPY options is that SPX options are traded in increments of 5 cents. Since SPX is 10 times the price of SPY or XSP, trading increments or tick size is actually more precise on a percentage basis for SPX. XSP trades in increments of one cent like SPY. SPX options are also very liquid and orders can usually be filled 5 cents away from the mid price, even in multi-leg orders. There is a little difference based on trade volume of different expirations. Monthly expirations typically have the most volume, followed by Friday PM expirations and month-end expirations. Monday and Wednesday expirations have the least volume and can sometimes be slightly harder to fill, especially for strikes away from the money with more than a week until expiration.

XSP have a lot less volume than SPX or even SPY options, so they can be a little less liquid. Because of their pricing, they trade very similar to SPY, but with a little less liquidity. Since XSP is an index option, there is no worry of assignment, and dividends are not a consideration.

Some brokers don’t allow trading of index options in their accounts, and some strategies are not allowed with index options in certain types of accounts. Some brokers charge higher commissions and fees for index options than for stock and ETF options, so watch out!

Finally, index options get a different tax treatment and have a different accounting treatment at the end of the calendar year. Index options fall under Section 1256 of the tax code which allows a trader to classify 60% of the gains from trading index options as long term, while only 40% are short term. For taxable accounts of traders in mid to high tax brackets, this can be a significant advantage! It doesn’t matter if the option was held for a minute or six months, the 60/40 tax assignment applies. The other part of 1256 treatment is that index option positions are “marked to market” at the end of the year, meaning that a trader considers the option to be a profit or a loss at the end of the year even if the position is still open based on the price at the end of the year of open positions. In stocks and stock options, only positions that have been closed are evaluated for a profit or loss. Using mark to market can be a bit confusing the first time around, but most brokers do all the calculations and provide them in a year end tax statement.

The CBOE has announced another index option on the S&P 500 index to start trading very soon, call Nano options. This index will be 1/1000 of the SPX, or 1/100 of XSP, to allow very small option trades on the S&P 500. Supposedly the ticker symbol will be NANOS. Stay tuned for more details.

Futures Options

There are two futures contracts on the S&P 500 index that offer options. The primary one is called the E-Mini S&P 500 Futures, which uses the symbol /ES at most brokers. In listings of futures contracts and futures options the symbol will be followed by a letter to designate the month the future expires and a number for the year of expiration- for example /ESH2 represents the future contract expiring in April of 2022. The other futures contract is called Micro E-Mini S&P 500 Futures, and uses the symbol /MES. Some brokers may use other characters to designate futures instead of the forward slash, and some may require approval of futures to even see the ticker symbols. Consult with each broker for details.

Futures are tradable contracts based on the price of the underlying index at the expiration of the contract. Futures contracts in general expire at a variety of times in the month with /ES and /MES expiring on Wednesday mornings and settling to opening prices of the S&P 500 index. Since the futures contract is based on what the market expects the price to be at expiration, the price of the future is usually a little less or sometimes a little more than the current value of the S&P 500 index. However, it generally doesn’t vary that much because the current price is one of the best indicators of what the future price might be and futures buyers and sellers won’t let the prices to diverge that much because it presents an opportunity for arbitrage between the different values, knowing that at expiration they will converge. At any given time, there are many different contract expirations available to trade, going months out in time. The contract month closest to expiration is called the front month. Buying a front month futures contract is as close to directly owning the S&P 500 index as you can get. The value of the futures contract goes up and down with the index.

A single /ES contract is valued at 50 times the S&P 500 index. One might think of it as owning 50 shares of the S&P 500 index if the index price were the price of a share. A single /MES contract is valued at 5 times the S&P 500 index. These values are known as the notional value. However, futures contracts are priced at prices similar to the actual S&P 500 index, regardless of the notional multiplier.

Let’s take an example. Let’s say that the S&P 500 index is currently at 5010, and front month futures contracts for both /ES and /MES are trading at 5000 as they are slightly less. The /ES contract would have a notional value of $250,000, and the /MES would have a notional value of $25,000. If the market went up 100 points on the S&P 500, and both /ES and /MES went up to 5100, the owner of one contract of /ES would make $5000, and the owner of /MES would make $500. For most people $250,000 for one contract is too expensive, but futures contract owners aren’t required to have the full amount in their account, but just a fraction due to the assumption that the price will only move within a small percentage of the index price. If the price moves more than expected against a contract owner or seller, additional capital will be required. This practice is called span margining, and can be very helpful to allow traders to leverage a position, but also very dangerous if over-used and the market moves against a position. For example, if a trader buys an /ES contract priced at 5000 and has $50,000 in their account, a 20% decline in the market to 4000 would wipe out the account. While /MES is one tenth the size, the problem can be the same for a trader with a smaller account.

So far we’ve talked just about the futures contracts themselves. The topic of this post is trading options on the S&P 500 index, not trading futures on the S&P 500 index. So, let’s talk about how options on futures work. In particular let’s look at options on /ES and /MES. One key difference from other options we’ve looked at is that /ES and /MES options don’t use a 100 multiplier, like stocks or index options. Instead, futures options are an option to buy or sell one single futures contract. Which futures contract is the option associated with? Typically, it is the futures contract that is next to expire after the option expires. So, an option on /MES expiring on the first Friday in March is tied to the March futures contract, which will still have time remaining when the option expires.

So, buying an /ES call gives the buyer the option to buy one /ES futures contract at option expiration, and buying a /MES put gives the buyer the option to sell one /MES futures contract at option expiration. So, settlement of the option at expiration doesn’t settle in stock or in cash, but in a futures contract. The price paid for the futures contract is the strike price of the option. For example, if a trader buys a call option for /ES with a strike price of 5000, they would get to buy an /ES futures contract at options expiration for $5000, multiplied times the /ES futures multiplier of 50, or a total of $250,000, assuming that /ES is trading above 5000, making the option in the money. On the other hand if the price of /ES is below the strike price of the call option, the option would expire worthless. Similarly, if a /MES 5000 put expired in the money, the settlement would be to sell a /MES futures contract for $5000 multiplied times the futures multiplier of 5, for a total of $25,000.

There are futures options for /ES and /MES that expire every Monday, Wednesday, and Friday, so there are plenty of expirations to choose from. And futures and futures options trade virtually around the clock, from Sunday afternoon until Friday afternoon. In fact, the price of /ES in the overnight hours moves around quite a bit based on news and as the opening of the market approaches, it is a fairly accurate indicator of where the market will open. Meanwhile the S&P 500 index stays the same during the overnight, because it is based on a calculation from the trading of the 500 stocks in the index, which don’t broadly trade at night.

The span margining ability to trade using the buying power associated only with a calculated expected move applies to futures options as well as futures contracts. As a result, traders can put on highly leveraged trades without consuming a lot of buying power. With this capability comes significant risk. Traders have to be very aware at all times of the true total risk that comes with trades in futures options. With futures options, the buying power used is not a good indicator of the capital at risk in the case of a very large move of the market up or down. Some brokers allow selling of naked futures options for very little buying power, where selling the same notional value of SPX or SPY could easily require ten times more capital even though the true risk is the same. Many trading strategies with futures options may seem very safe because they are high probability trades- perhaps they win 90% of the time- the problem is when the losing 10% happens and the trader is not prepared for the damage that occurs to the account. Risk management is critical in all options trades, but particularly in futures options using span margin. Stops and hedges become the difference between staying solvent and going broke.

Like index options, futures and futures options also use section 1256 tax treatment with 60% long term gains and 40% short term gains, and are marked to market at the end of the year. There are no dividend risk issues.

One final unique advantage to futures options is that they are exempt from the Pattern Day Trade rule. For accounts under $25,000 where trades are opened and closed the same day, a trader can have severe limitations placed on an account. Generally, the limit is five day trades in a rolling seven day week. This can be stocks or options. Futures and futures options are governed by different regulations, so many day traders favor futures.

Many brokers have significant approval processes to be allowed to trade futures or futures options. Some limit them only to standard taxable margin accounts. Other brokers don’t allow them at all. Go to the office of your broker and see if anyone there has any experience trading futures or futures options- it is likely no one there has a clue and they will tell you not to do it. If you have friends that trade in the market, chances are that almost none have ever traded a future or futures option, so you are likely on your own. Your best source for help will be specialist from your broker’s headquarters, specialized training materials, or online resources from your trading community as I discussed in an earlier post.

If trading futures options is so complex, hard to understand, and risky, why do it? For many strategies, futures options can fill in gaps at a low capital requirement. Some hedging strategies can be too expensive with stock or index options, but more affordable with index options. Because of the unique multipliers, futures options for the S&P 500 index may be just the right size for a particular need. And finally, because the futures prices move and trade all night, futures and futures options allow trading on that information at some brokers.

Review of choices

After a lot of discussion and explanation, we have come up with seven choices for trading options on the S&P 500 index. Five of these are directly correlated to the index, and two are leveraged. Remember that the UPRO ETF moves up and down with the S&P 500 index, but three times as much each day. SDS, the UltraShort ETF not only moves the opposite direction of the S&P 500 index, but twice as much in the opposite direction on a percentage basis each day. Because of this leverage, the options on these two ETFs behave in unique ways which can be helpful for some strategies. However, most traders are more likely to want options that are based on underlying entities that move on a 1:1 basis with the S&P 500 index. So let’s review those choices.

Ticker

Type

Index vs Strikes

# of Shares or Multiplier

Notional Value @ SPX = 4000

Settle as

Tax Treatment

SPX

index

1 : 1

100

$400,000

cash

60/40

/ES

futures

1 : 1

50

$200,000

one contract

60/40

SPY

ETF

1/10

100

$40,000

100 shares

short term

XSP

index

1/10

100

$40,000

cash

60/40

/MES

futures

1 : 1

5

$20,000

one contract

60/40

This table lists key differences in the five main choices for options on the S&P 500 index, listed in order of notional size. In this table notional value refers to the amount of capital controlled by a single option with a strike tied to the S&P 500 index being at 4000 (SPY and XSP would have strikes at 400, while SPX, /ES, and /MES would have strikes at 4000).

While SPY is the simplest choice because it is most readily available, there are reasons to consider each of the other listed choices to best meet the needs of a specific account or strategy. From biggest to smallest, SPX controls 20 times as much capital as /MES, and the other choices provide increments in between. I was personally reluctant to trade futures options at first, but for no good reason other than I wasn’t familiar with their nuance. As I write this, I currently have at least one contract of each of these five choices open amongst the various accounts I manage.

For all of our choices, we currently have the ability to select expirations three days a week, and potentially five days a week in the near future. Each choice has an extensive selection of strikes available at each expiration, although one can expect Friday expirations and month end expirations to have more choices and more trading volume than Mondays and Wednesdays. We expect third Friday (monthly expirations) to have more choices and trading volume than any other expiration in the month.

My personal preference in most situations is SPX due to its large size. Even though commissions and fees are more on a per contract basis, the fact that SPX is 10 times bigger than SPY or XSP makes commissions and fees almost negligible in most trades of SPX, where they can be a substantial consideration with SPY and XSP in some strategies that deliver narrow profits. For futures, I like /ES over /MES for the same reasons. However, when I’m trying out a new strategy or working with a small account, I often have no choice but to use SPY, XSP, or /MES. For most new traders, SPY is the first and easiest choice, but eventually there may be a need to use another choice. For example, if you start trading 10 option contracts at a time, it might make sense to use SPX. If SPY is too big, you may want to get approval to trade futures and trade options on /MES. If you have a taxable account and are in a higher tax bracket, XSP may be a good alternative to SPY to reduce short term capital gains. So, learn the differences and make the choice that makes the most sense for the situation.

If you want to investigate strategies for trading options on the S&P 500 index, take a look at some of my favorite strategies. You may also want to read my page on how different option strategies have very different risk profiles.

Traders need access to other traders to share, learn, and teach each other. Online social media groups can provide that type of community.

Let’s face it. Trading options can be a lonely task. It’s just a trader and the computer screen. Whom can a trader turn to with questions, for encouragement, or to share success and failure? Virtually every person who I dare to tell that I trade options as a primary activity either have no idea what I’m talking about, think I’m crazy, or both. Most people who do a lot of their own investing don’t even know what a put or call is. Traders need a community of other traders to keep their sanity and keep moving forward.

When I stop and think about it, I personally know seven option traders that I have met in person. Only seven. Four of them I met through one of the others. And only a few of them regularly do the same kinds of trades as me. And I feel lucky to know that many. So, personal connections can only help so much.

There are lots of online services that traders can pay a small fortune to join to help learn to trade options. Some are follow the leader- buy or sell what the guru says and exit when the guru says. I tried a few of those and found it hard to time it right and even then I didn’t get the results that were promised. So, I’m not a big fan of spending a lot to watch others trade.

If you do a Google search about any topic concerning options, you’ll be bombarded with ads for paid services, but then below them will be lots of YouTube.com videos, and other sites, maybe even this one. There are lots of quality YouTube videos on options, but many that are dubious at best. I first discovered TastyTrade.com through watching some of their YouTube videos. Tastytrade has their own channel on YouTube, and I’d encourage subscribing. One TastyTrader that I enjoy watching is “Sweet Bobby” Gaines. He has a “Sweet Bobby” channel on YouTube. Look around and search YouTube for option trading, and find your own favorites to follow.

But even watching others still doesn’t give you community. There’s nothing like interacting with others. This is where social media actually can be a help. A feature on Facebook.com that you may not be aware of is “Groups.” Just click on the Groups icon and either use the “Discover” icon or the search magnifying glass to look for groups that specialize in option trading. Some are more active than others. Most are private and require you to apply for membership- this is generally to keep out spammers and robots who will ruin the experience. I’ve joined a number of groups- some I’m active in and others not so much. For groups that don’t have members doing strategies I have in interest in, I simply drop my membership. I now have a number of virtual friends from these groups. Some of them message with me on an almost daily basis. I’ve discovered numerous trading strategies to try from posts in these groups, and the banter from members gives the members a wide variety of opinions about different trading scenarios, positive, negative, pointing out risk, ways to manage, and success stories.

Another social site that gained a lot of traction in early 2021 was Reddit.com. Reddit became an overnight sensation for traders when a little-known group on the site called “Wall Street Bets” essentially cornered the market on the stock of GameStop, an almost bankrupt video game store chain. By realizing that there was a huge amount of short interest in the stock and a small float of tradable shares, the group started buying up cheap shares of stock, and bigger buyers followed, driving up the price. Many short sellers, including some large hedge funds were caught flat-footed and had to buy back their short positions at huge losses, further driving up stock prices, a classic short squeeze. Call option buyers joined in as well and market makers hedged by buying increasing numbers of shares also driving up prices. By the time the craziness ended the stock was up over 100 times the price when the buying started. This crazy action drew attention to Reddit and the “Wall Street Bets” group. Like many, I joined both for the first time to see what the fuss was all about. The group membership ballooned to an enormous number and the content turned to mush- just a lot of nonsense posts slamming each other and promoting hundreds of other crazy schemes. I dropped my Wall Street Bets membership after less than a week.

However, Reddit has a feature that suggests posts from other groups that it thinks a reader might like. I found some other groups that I started commenting on that were more serious and in line with my view of trading. Again, I met a number of new virtual friends and engaged in both public and private dialogs about trading strategies. Groups on Reddit are public to read and join, so there can be a lot of spamming behavior and many users delight in being very foul-mouthed in their responses. Rudeness is tolerated a bit much, in my opinion. However, I’ve found that if I stay on the high road in my posts and stay factual and data focused, people generally engage back with me in a respectful way. It’s kind of a what goes around, comes around. In fact, the site has a measure called karma that is based on how well your posts are received by others. People who are mean and overly negative end up with negative karma and many of their comments get deleted by moderators.

Another social site that I’ve found helpful is Discord.com. Discord was started as a way for gamers to chat with each other in private rooms, and have discussions in groups on a private “server.” Once you join Discord, you can set up your own server, or join public servers set up by others. As it applies to traders, individuals will set up and organize a server and invite others to join. Many people have private servers by invitation only. Some of my local friends set up a server like this and invited me- I like the familiarity of the small group and we get along well with each other. I’m also a member of a number of other groups. A nice feature is that anytime someone posts a response to a server, I can have a notification pop up on my phone, or I can choose not to- the choice can vary from server to server. So, I have notifications on for some servers and off for others. The idea is that like-minded people can have an ongoing private dialog about their trading. Some conversations are based on users posting each of their trades for comparison and comment. So, a group of 0 DTE traders might each post their opening and closing trades, and then discuss what went right and what went wrong, critiquing themselves and other members on strategy. A Discord server can be very busy, or not busy at all- it depends on the number of users and how active they all want to be.

Twitter.com can be another source for information on trading. There are lots of famous and not so famous traders and information sources that tweet out information on a regular basis. I personally don’t have the bandwidth for it at the moment and don’t use it much. However, I know lots of traders love it. TastyTrade has a daily show, the Liz and Jenny show, where much of their discussion is based whatever Twitter posts use the hashtag #LizJny, which has fostered a community feel. Other shows on trading networks and CNBC have similar features and hashtags. Many high profile traders will respond to personal tweets or tweets that use an @ reference for them. However, the format really doesn’t lend itself to in-depth discussions. Often, it just allows tweeters to refer followers to content that the tweeter thinks is interesting.

I used to be a big fan of LinkedIn.com and its groups. Now, I think other social media resources have taken the lead in being sources of interaction with like-minded traders. I joined a few trading groups, and I have to say that I’ve been disappointed so far. Maybe new groups will emerge that will be better for the trading community, but I’m still waiting.

I know TikTok.com is gaining ground in this space as well. Similar to YouTube, TikTok offers videos, generally short in duration, and based on your reaction, the site steers you to similar content that might be appealing. As I write this, it seems a bit of an immature community currently, but by the time you read this in the future, TikTok could be the greatest resource available. We’ll see.

This is just a start. Feel free to leave your favorite way to get involved in the trading community in the comments below. New forums and sites are emerging all the time and providing new opportunities to connect with other traders. I’ll refrain from naming any specific groups on any particular site, because if you are reading this years from now because I haven’t updated it, there will likely be many new groups and sites to join and find community.

From my website Analytics, I can see that over half the hits to my site come from people clicking on a link to this site from a post someone referenced on a social media site. It used to be just me that did that on occasion, but lately others are finding this site and sharing it with their groups and trading friends. I really appreciate it when readers of this site find it helpful enough to copy a link from this site and share it with others. People seem to like the pages I have on my favorite trading strategies. I hope that you find some community here as well and find content worth sharing. Your comments are always appreciated, even it is a pain to leave them. It’s a challenge to have a site like this that doesn’t get nailed by spammers and hackers, so I have to put up some hurdles to allow comments.

Remember, the whole point of this post is to give you ideas about connecting with other people who understand the kinds of struggles you face as a trader, and give you a chance to give back to newer traders. Discussing trades on social media is the only place where I can discuss the merits of 20 delta short strike on a wide put spread, and know that most of the people reading will not only understand, but have an opinion to share back with me. That won’t happen at the next neighborhood block party. You aren’t crazy. There are people out there that get what you are trying to do and will be happy to have a discussion about it. You just have to know where to look. That’s the power of community, even when your community is spread around the world.

Build an annual financial balance sheet to track net worth, assets, liabilities, income, and insurance. A simple year‑end snapshot for smarter personal finance planning

Most people think of balance sheets as something only businesses use. But the truth is simple: every household benefits from taking a yearly financial snapshot. Every January, I like to hit pause and take a clean snapshot of my financial life. Not in a stressful way — more like stepping on a scale once a year just to see where things stand. It’s amazing how grounding it feels to look at everything in one place: what you own, what you owe, what you earned, and how protected you are.

If you’ve never built a personal balance sheet before, don’t worry. It’s simpler than it sounds, and once you set it up, updating it each year becomes a quick ritual that pays off in clarity. I’ve found that creating this snapshot at the start of each year is one of the most powerful ways to track progress, spot risks early, and make better long‑term decisions.

What does this have to do trading options, the focus of this site? A trader’s use of options is part of their overall investment plan, as well as a wealth creation and preservation strategy. Once in a while it’s useful to step back and look at the bigger picture. If I’ve made particularly wise or foolish trades, they may have a substantial impact on my overall financial condition, so I use this tool to put my trading into perspective.

Why an Annual Balance Sheet Matters

Life moves fast. Bank accounts change, investments grow or shrink, loans get paid down, and new obligations appear. Without a structured review, it’s easy to lose track of the big picture.

A yearly balance sheet helps you:

Measure progress by comparing this year’s numbers to last year’s

Spot trends in savings, debt reduction, and investment growth

Prepare for conversations with your spouse, financial advisor, or accountant

Organize key information for emergencies or estate planning

Stay intentional about your financial direction instead of drifting

Think of it as your household’s annual financial report—simple, honest, and incredibly useful.

Start With Your Assets (What You Own)

Think of this as your “everything that has value” list. You don’t need to overthink it — just gather the numbers from your year‑end statements. I like to also track what I’ve contributed or withdrawn from each type of asset or account to separate what is growth or decline from my cash flow impacts.

Typical Categories and where to find the data

Home value: Zillow, Redfin, or your latest appraisal

Record the value of each item as of January 1 (or whatever date you choose). This becomes your baseline for the year.

I think it is also a good practice to regularly deep dive into the make-up of stock and options portfolios. I look at that as a separate exercise which I’ve discussed in some detail in my write up on portfolio management. For that reason, I won’t discuss that as part of this household balance sheet.

List Your Liabilities (What You Owe)

This part is just as important — and often more motivating — because you can literally watch your debts shrink year after year.

Since I’m paying interest on all the money I owe, I like to list the interest rate on each debt. Maybe you want to also track what each monthly payment is. Keeping that out front can help in prioritizing debts to attack first.

Typical Categories and where to find the data

Mortgage: Your lender’s year‑end statement

Auto loans: Loan servicer statement

Student loans: Loan portal

Credit cards: December statement

Personal loans: Lender portal or statement

Just like with assets, use the balance as of your snapshot date, or as close as you can get.

Calculate Your Net Worth

Once you’ve listed everything, the magic moment arrives:

This number is your financial “you are here” marker. It doesn’t define you — it just gives you a baseline to compare against next year. Your net worth is the single best high‑level indicator of your financial health. Tracking it year over year shows whether you’re moving in the right direction—and by how much.

Even if the number isn’t where you want it to be, having clarity is the first step toward improvement.

Add Your Income Snapshot

This isn’t part of a traditional balance sheet, but it adds helpful context. It shows how your earning power and investment income support your financial progress.

Where to find the data

Work income: W‑2, pay stubs, or payroll portal

Side income: 1099s or your own records

Investment income: Year‑end brokerage statements (look for dividends, interest, and realized gains)

Rental income: Your bookkeeping or tax prep records

You don’t need to break it down to the penny — just capture the big picture.

While income isn’t part of a traditional balance sheet, including it gives you a fuller picture of your financial ecosystem. This section helps you understand how your cash flow supports (or limits) your financial goals.

Another related addition I like to add later to this section is my income taxes for the year. Since I likely won’t know that until after I do taxes, it will probably have to wait.

Document Your Insurance Coverage

Insurance is one of the most overlooked parts of a financial plan. Listing your policies in one place makes it easy to review coverage, compare premiums, and ensure your family knows what exists if something unexpected happens.

This is one of those “future you will be grateful” sections. “Present you” may find that it is time to add or subtract coverage, or find a new carrier.

Where to find the data

Policy documents

Insurance provider portals

Renewal statements

Include:

Auto insurance

Homeowners or renters insurance

Health insurance

Life insurance

Disability insurance

Long‑term care insurance

Umbrella liability policies

You don’t need to list every detail—just the provider, policy type, and key coverage notes. Where it makes sense to list, add coverage amounts, premiums and/or policy numbers. I recommend keeping it simple to start with and add more details that you think are important over time.

Why a Spreadsheet Makes This So Much Easier

A simple spreadsheet turns this into a living document you can update each year. It also makes comparisons effortless:

Update values each year without rebuilding anything

Automatically calculate totals and percentage changes

Add charts if you want a visual snapshot

Print a clean copy for discussions with your spouse or advisor

Store a version in a safe place for emergencies

It becomes a living document — part financial checkup, part family preparedness tool. This becomes a clean, printable document you can review privately, discuss with your spouse, or bring to a financial advisor.

Add Year‑Over‑Year Percentage Changes

This is where your spreadsheet becomes really insightful. Instead of just seeing that your net worth went from $X to $Y, you can see the percentage change, which puts everything into perspective.

How to calculate it

Use this formula in your spreadsheet:

Then format it as a percentage.

Example

Last year’s net worth: $500,000

This year’s net worth: $550,000

Suddenly, you’re not just “up $50k” — you’re “up 10%,” which is a much more meaningful way to track progress.

You can apply this to:

Net worth

Individual asset categories

Debt balances

Investment accounts

Income changes

It turns your balance sheet into a year‑over‑year dashboard.

Example Document

Your sheet might look something like this. There is no set standard format for this, so make it work for you.

Store It Somewhere Safe

Your annual balance sheet is more than a planning tool—it’s also a critical reference document for emergencies.

Keep a copy:

In a secure digital folder

On an encrypted drive

In a safe or lockbox

With other estate‑planning documents

If something happens to you or your home, your family will have a clear roadmap of accounts, assets, debts, and insurance policies—saving everyone enormous stress and confusion.

Final Thoughts

Creating an annual financial balance sheet isn’t about being perfect with money. It’s about being aware. It’s about giving yourself a clear picture of where you stand so you can make better decisions going forward.

Once you build the first version, updating it each year becomes quick and almost effortless. And over time, you’ll have a powerful record of your financial journey—one that helps you stay grounded, confident, and prepared.

Once you do it the first time, you’ll wonder how you ever lived without it.

A big shout out to those of you who reached out to John Einar Sandvand to ask about this site. We had a week of no DataDrivenOptions.com.

Thank you for your patience! We had a week of no DataDrivenOptions.com. It didn’t help that I was on vacation and wasn’t doing any content for the site, so I didn’t know there was a problem.

A big shout out to those of you who reached out to John Einar Sandvand of ThetaProfits.com to ask about this site. He reached out to me through another communication channel to see what was going on, which is how I found out the site was down. John Einer and his videos are a great resource and I’m grateful that he has chosen to feature trades from this site a few times. He’s also a great guy. He said he had several questions from concerned traders.

If you’ve tried to reach this site in the past week, you probably got an error. It turns out that my domain registration expired, and somehow I didn’t get the message. My email for the site is also tied to the URL domain registration, so it went down as well. I thought I had registration set for auto renew, but something went wrong. It is fixed now and hopefully that won’t happen again.

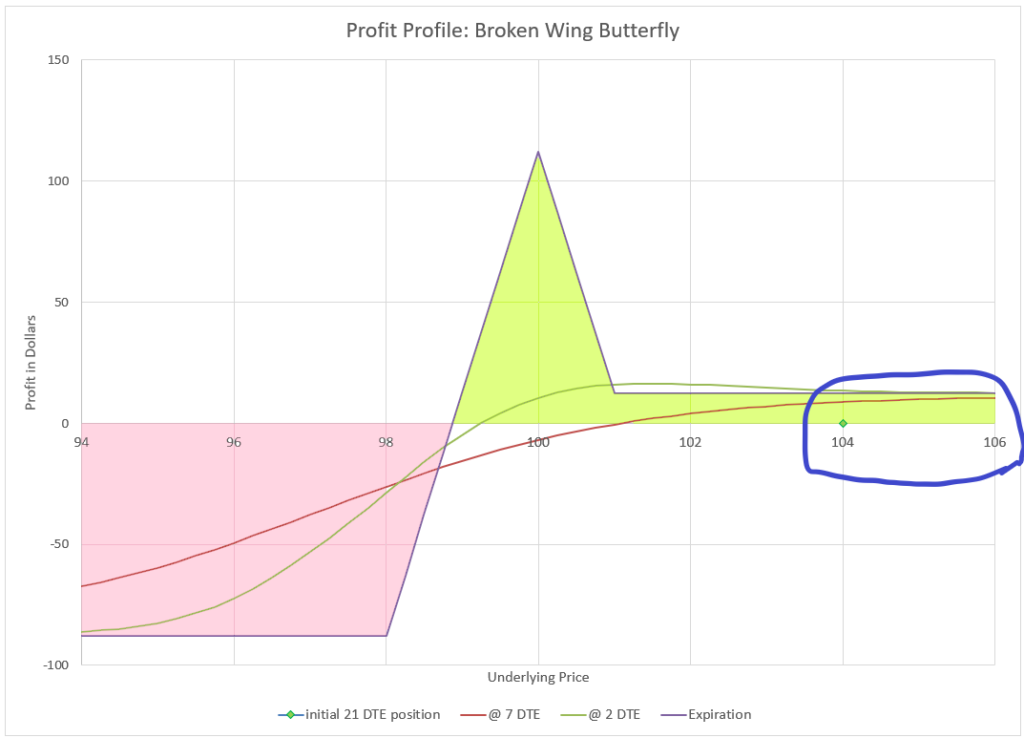

In March 2025, I was interviewed by John Einer Sandvand for his ThetaProfits.com YouTube channel. This 21 Day Broken Wing Butterfly video is the second video I’ve done with him. He’s done really well with his channel and has interviewed some amazing guests, and I am honored that he included me.

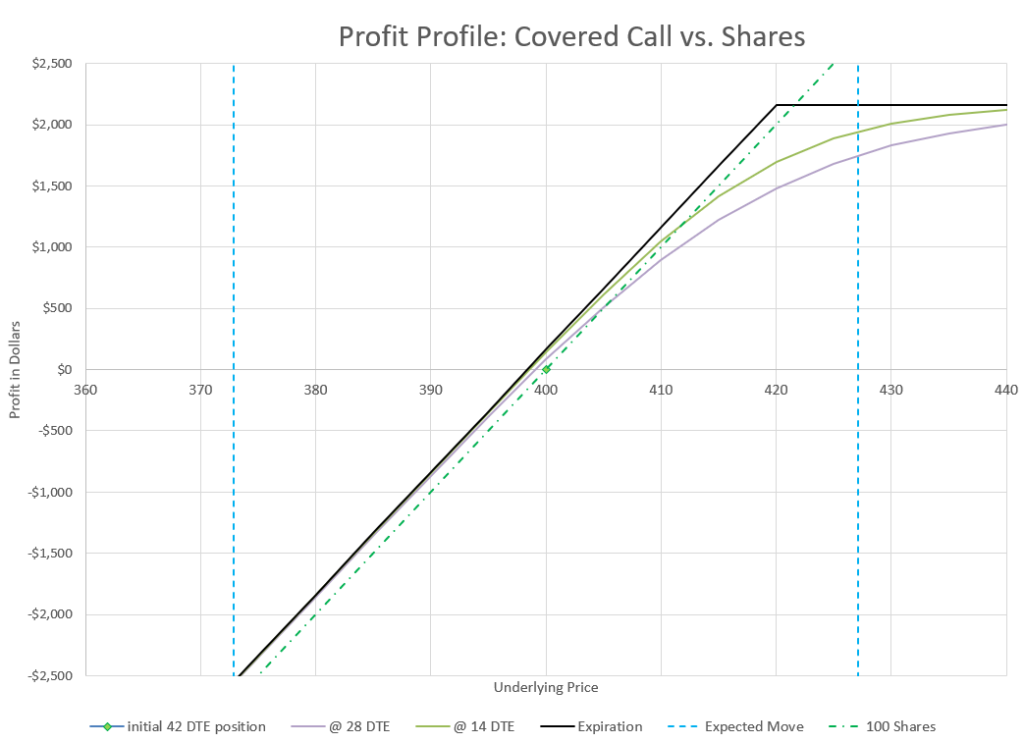

Those pages have the details of the trade, and I’ll let them speak for themselves. But as a brief refresher, here is the profit profile of the trade:

The profit curve of the 21 day Broken Wing Butterfly, highlighting the starting point of the trade.

Thanks to all who have watched the video and come to look around at this site as a result. As I mentioned in the video, the pages on the 21 Day Broken Wing Butterfly trade are consistently the most popular pages on this website- I’ve never understood why, considering that I have written content on so many more common option trading strategies.

I’ve received a few questions about the use of stop losses that I mentioned in the video along with probabilities. If you read the original write-up, you’ll see that I’m not generally a big fan of stop losses but they can be a useful tool. Over time, this trade actually wins greater than 80% of the time if allowed to continue. However, during extended bear markets like in 2022, the win rates were less, especially if stop losses were employed. For those trying to figure out how different management strategies compare, one thing that many analyzing traders forget is that this trade doesn’t always end at max profit or max loss. Sometimes it ends up in between, and that doesn’t make for easy calculations.

What I can say is that this trade does very well in bull markets, and does poorly in true bear markets. So, the majority of the time, this trade can get great returns. But always have a plan for how to manage when the market turns.

I like to roll covered calls almost no matter what, even when my rolls are deep in the money. There are advantages to this strategy, particularly in bear markets.

When I sell options, my favorite management strategy is to roll the option out and collect a credit. I like to do this win, lose, or draw. With a covered call, I like to roll almost no matter what, even when my rolls are deep in the money. Over time, I’ve found there are some advantages to this strategy, particularly in bear markets.

If you read a lot of my explanations on selling calls, you’ll see that I have not been a big fan of call selling in general. That goes for call credit spreads, the wheel, and selling covered calls. My general complaint is that because the market goes up much more often than it goes down, short calls tend to lose money. I’ve seen it in my trading and I’ve seen it in back tests. But covered calls are one of the most popular trades out there- so why are there so many fans?

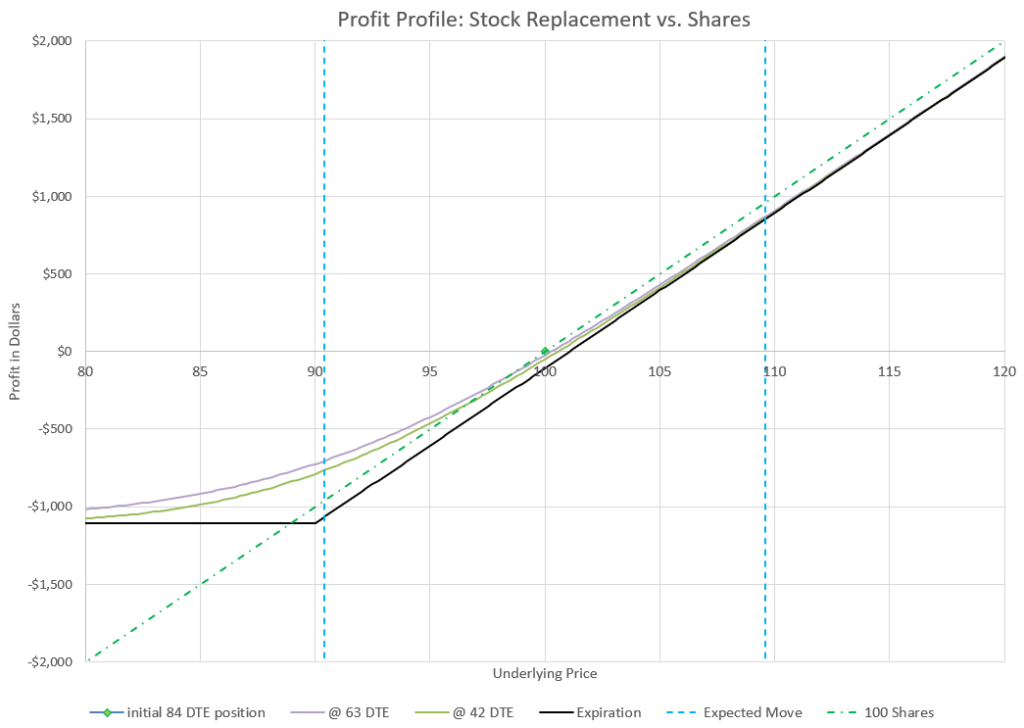

What is a covered call?

A covered call is a combination of buying or owning 100 shares of stock, and selling a call on that stock. Selling a call obligates the option seller to sell 100 shares of stock at the strike price of the option at any time the option buyer wants to exercise the option. Since the option seller owns 100 shares of stock, those shares cover the exercise risk of the call option- the call seller has 100 shares that can be sold if the the call buyer wants to exercise the option. But the option seller collects a premium when selling which decays in value over time. At option expiration, the option expires worthless if the stock is under the strike price, or it will likely be “called away” by the option buyer if the stock is greater than the strike price. Many traders sell calls against their stock positions to collect premium as extra income.

Let’s look at a typical set up of a covered call:

set up of a covered call with 42 days to expiration on a $200 stock

Here we are buying 100 shares of stock at $200 per share and selling a call with a strike price of $210 with 42 days to expiration (DTE). We collect a premium of $0.81, or a total of approximately $81 for the contract. So, our net cost per share to start is $199.19, instead of $200. This lowered “cost basis” is a benefit of selling a covered call- we’ll work to continually lower this further over time.

Throughout this article, we use this example position to demonstrate how rolling a covered call works. Each example transaction will be highlighted to differentiate it from the rest of the text.

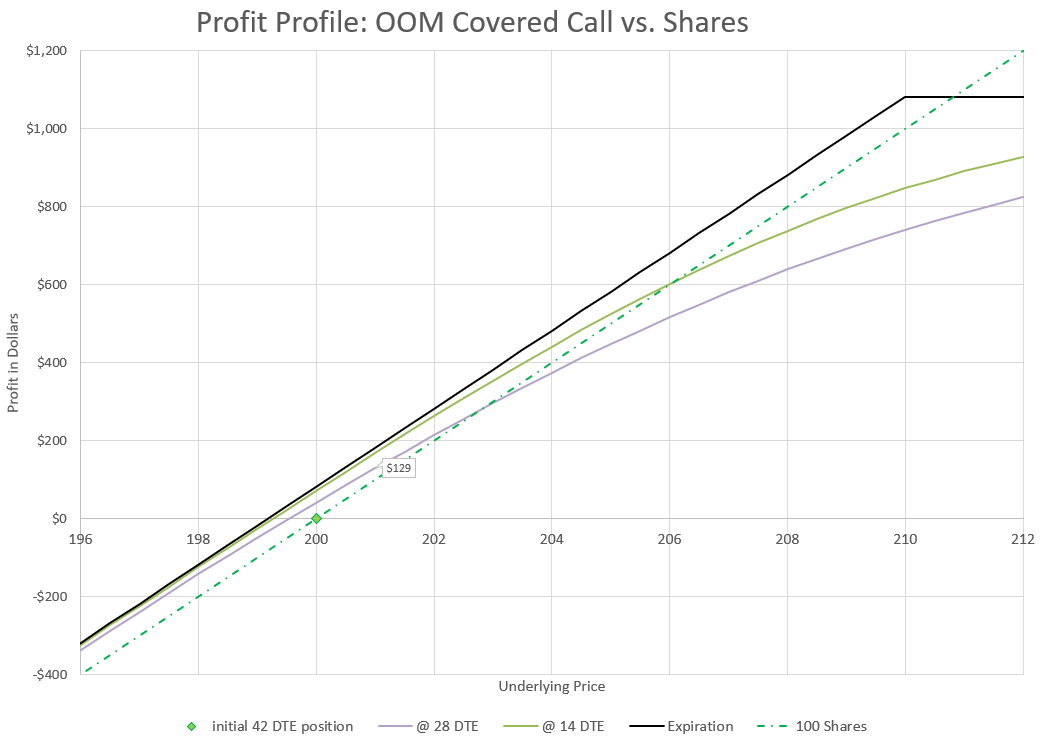

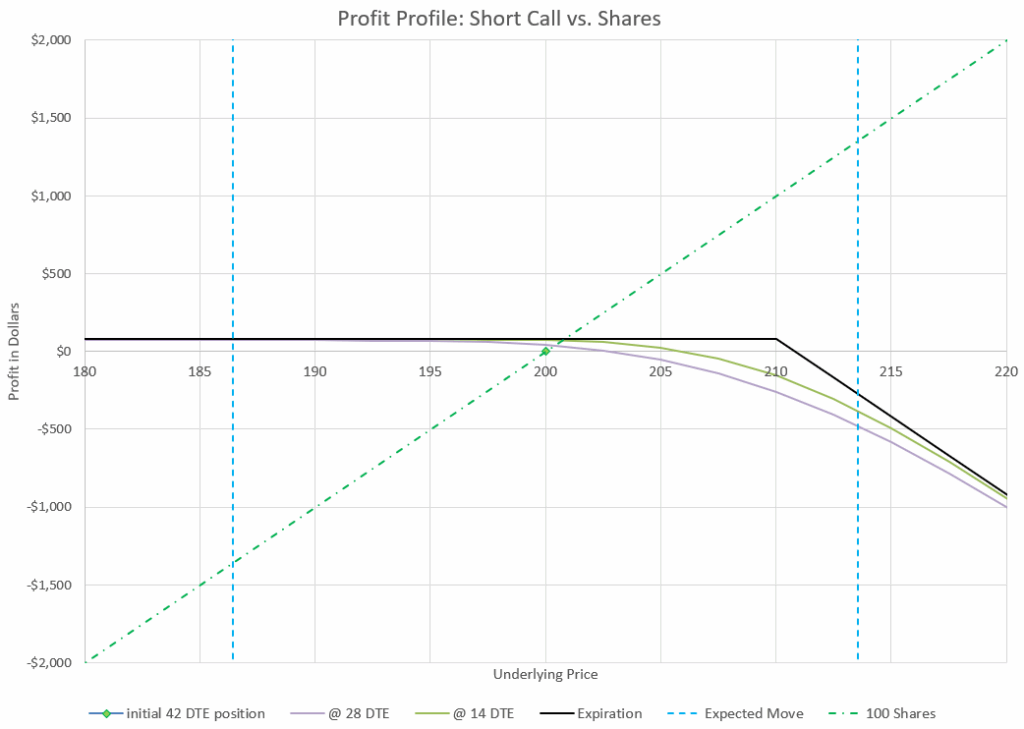

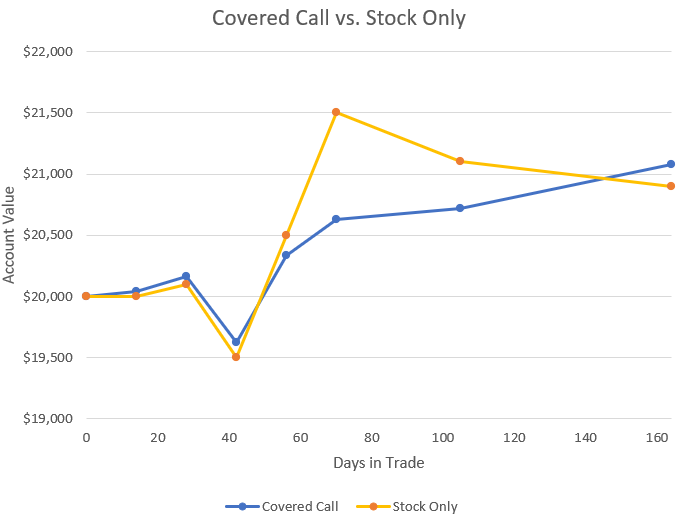

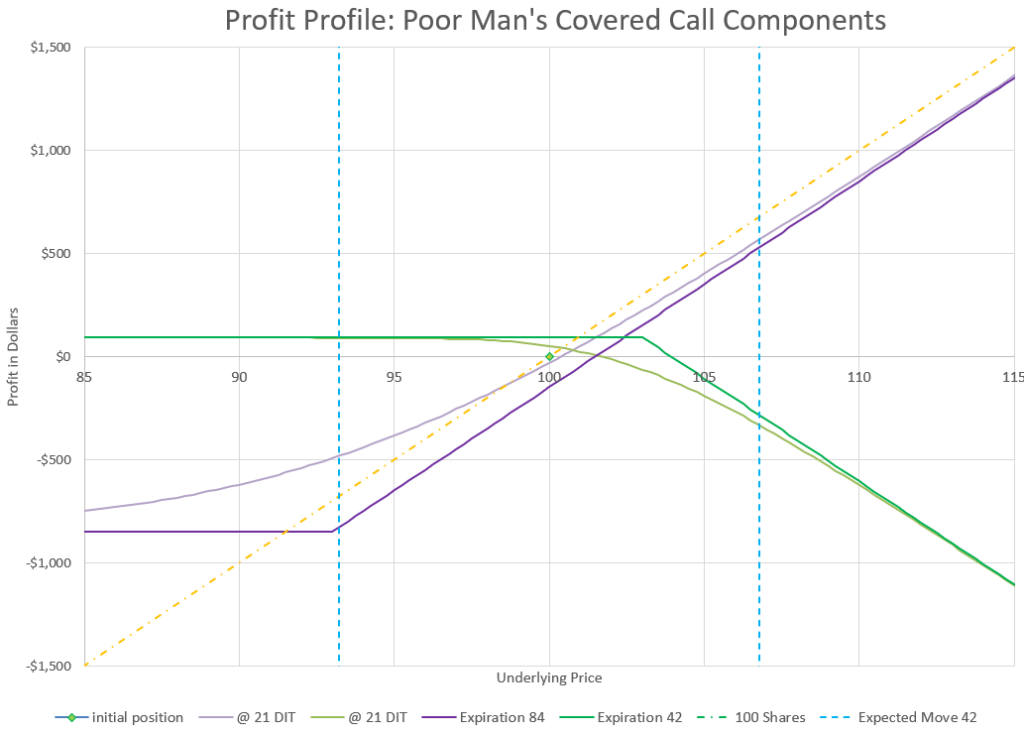

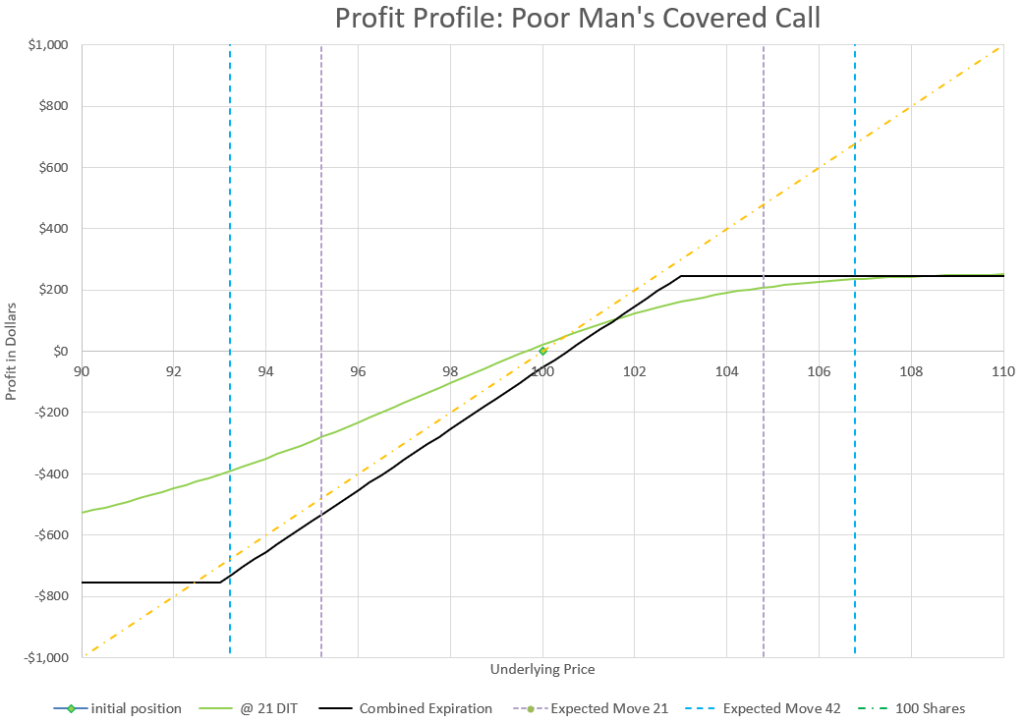

To see how this strategy works, let’s look at a chart of the profit profile of each component plotted separately:

profit of a short call vs shares- the two elements of a covered call strategy

The call makes a small profit at any outcome up to the 210 strike price, and the stock goes up and down. Above the 210 strike price, the two elements of the covered call go in opposite directions, cancelling each other out at expiration. Now, let’s combine the two profit lines into one and see what the outcome looks like:

covered call profit profile- at expiration and at selected times before expiration

Through most of the expected move, the covered call profit is a little better than just owning stock alone. Recall that the expected move is what is implied by one standard deviation of the implied volatility of the option chain-see the article on expected moves for a refresher. Only as the price movement gets close to the upper range of the expected move will the covered call profit be less than stock alone. But even in that situation, the profit of the covered call is substantial. The covered call limits maximum profit in exchange for better outcomes at every other point in the profit curve below the strike price.

Ultimately, covered calls are bullish strategy- the long stock always has more positive Delta than the short call has negative Delta, so covered call owners make money when the stock price goes up.

There are several outcomes possible from selling a covered call. The only sure thing is that time is always on the side of the call seller, eating away at the extrinsic or time value of the call option. However, price movements in the underlying stock will move the total position up or down the same direction as the price movement. When price goes up, the stock obviously goes up, while the call option gets more negative premium. The option premium change counters the stock price change, but the stock move is always more than the option premium move. The same is true on down moves, the stock will always move down more than the option premium will help. In the end, the short call option dampens the response of the stock price movement either way. A covered call makes a stock holding less volatile- another benefit.

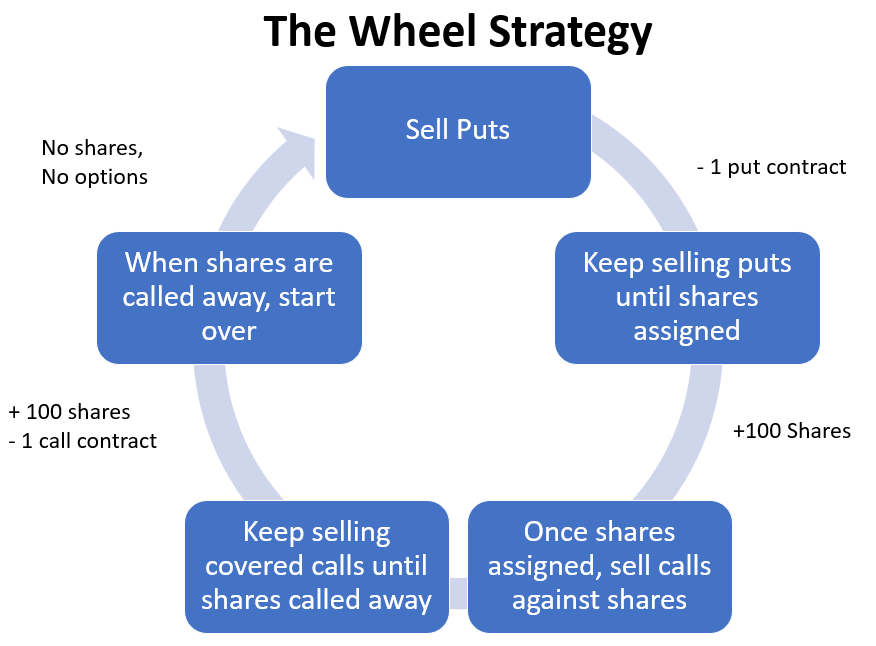

There are lots of ways to trade covered calls and to manage them. Some traders sell calls and then wait for them to expire or get exercised by the buyer. This is often true of “wheel” traders, who sell puts to get assigned shares, then sell calls against their shares until they the shares are called away, then they repeat the process, collecting option premium at each transaction.

The covered call is one element of the “wheel” strategy

Other covered call sellers aim to never let go of their shares and defend their positions so that the call buyer will never exercise the call option. This can be tricky, but the basic strategy is to make sure that the extrinsic value of the call is always more valuable than what the value of exercising the option is, so that exercising the option would be a money loser for the call owner. Generally, the three situations where a call buyer will exercise is when the option is in the money at or very near expiration, when a dividend is being paid, and when a stock option is too illiquid to sell and the only way to close the position is to exercise the call option. So, if a covered call seller can avoid being in those situations, they won’t lose their stock.

What does rolling an option mean?

Many new option traders are under the misunderstanding that they have to hold onto a position until expiration. If fact, generally a trader has three choices- hold, fold, or roll, which I’ve written about elsewhere. But let’s talk about rolling.

Rolling an option is when a trader closes one option and opens another option, usually in a single trade. A trader generally rolls up, down, out, or a combination. Rolling up means that the new option is a higher strike price than the old. Rolling down means that the new option is a lower strike price than the old. And rolling out means that the new option has a longer duration than the old.

As a continuation of our example, let’s say you have sold a $210 strike call on a stock and it is now set to expire in 28 days. You decide to roll out to 42 days. To do this you buy back the 28 DTE call and sell a 42 DTE call. If you sell a $210 strike call at 42 DTE, you have rolled out. If you sell a $211 strike call, you have rolled out and up.

With price remaining at $200, we can collect a credit to roll out to 42 days.

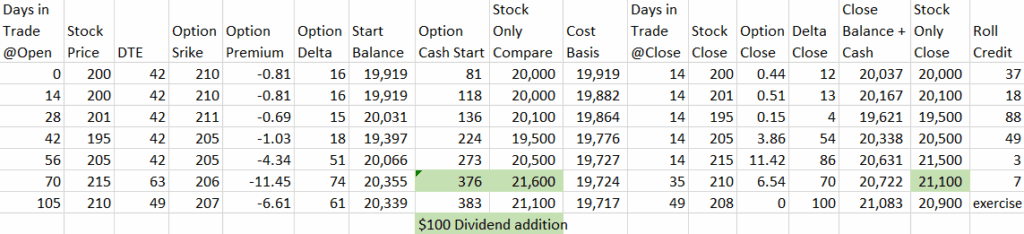

In this example, we are again collecting 0.81 premium on our new call, and since the old call has decayed to 0.44 premium, we have made a profit of $37 in the 14 days we held this covered call position, even though the stock price hasn’t changed. As it happens, we also have collected a net $37 credit for our roll.

With the price up, we may want to roll up and out, while still collecting a credit.

In this next example, the stock is up from $200 to $201, so we decide to roll up to a 211 strike, which still allows us to collect an $18 credit. Since the stock went up $1 a share, we’ve made $100 on the stock and our call made $30, by decaying from 0.81 to 0.51. In total, we made $130 on the move, compared to only $100 if we had only had the 100 shares.

Some brokers may label these trades differently, perhaps considering rolling up or down as a vertical spread trade, since you are buying and selling an option in the same expiration. If you roll out, some brokers may label this trade as a calendar trade, since you are buying and selling the same strike at different expirations. And if you roll both out and either up or down, your broker may label the trade as a diagonal spread, since you are buying and selling options at both different strikes and different expirations. The true difference between these labels and a roll is that with a roll, one side of the trade is closing a position, while the other is opening a position. When rolling a covered call, you are buying to close the old position, and selling to open the new position.

Notice that when we roll, we are only transacting our call position. The stock stays untouched. The stock’s roll in this trade is to “cover” the short call, so that risk is managed, by limiting it to the cost of the stock.

Why Roll a Covered Call?

There are three good reasons that I think most people use for rolling a covered call. First, they don’t want to have their call option exercised, so they roll out for more time and more premium to make exercising the option by the buyer less attactive. Second, a covered call seller may roll because the premium has decayed and they want to have more premium to decay and the seller doesn’t want to wait for expiration. Third, a covered call may be in the money and a covered call seller may want more attractive strikes. All of these are valid reasons to roll a covered call. Ultimately, all of these reasons boil down to an overarching reason- to keep collecting call option premium.

For most covered call sellers, the goal is to collect additional income from selling calls, and to keep the income coming, one has to keep selling over and over, so rolling is a common way to do it. The only alternatives are to hold to expiration, or let the shares be called away. I prefer rolling to avoid surprises as expiration approaches and to avoid options being exercised against me as much as possible.

Easy Rolls vs Hard Rolls

If the price of the stock that you sold covered calls against never really moved, you could just roll out to the same strike time after time. Sometimes, this is the case, and decisions are easy. If stock prices stay in a range, regular rolls can collect additional premium without adjust strikes up or down. For me, I’m generally happy just rolling my strikes out when the Delta of my call is anywhere from 10 to 40. There’s plenty of premium to collect and I’m not in danger of having the call exercised.

The earlier rolls shown are examples of easy rolls- the price either stayed the same or went up a small amount where we could roll and collect a credit to have a new position with similar Delta and similar premium to what we started with before time passed.

However, if my Delta value gets higher or lower, I have some decisions to make.

Let’s start with Delta values that are less than 10. When call Deltas are low, that means the stock is getting low compared to the call’s strike price, probably because the stock is going down in value. That probably isn’t good because the stock can lose a lot more than the call decay can make for a covered call seller. The worst scenario for a covered call seller is for the stock to go down significantly in price. All risk is to the downside, and even though the call sale premium makes up some of the loss, it can be a drop in the bucket. So, what can a covered call seller do when the underlying stock goes down in price. Let’s consider three choices.

Roll down and out. By rolling to a lower strike at a later expiration, a covered call seller gains premium both ways, more time and more Delta. Just pick the Delta you want from the later expiration and collect a nice payment for the roll. Sounds like a no-brainer. But what if the strike price is lower of the new option is lower than what you paid for stock? The concern is that if the price reverses, the position could get stuck in the money with a value less than what you paid. Do you want to potentially “lock in” a loss? For example, if you bought shares for $100 and the price drops to $80, is rolling calls down to $90 strikes a good plan? Many traders have a rule to never sell a covered call at a strike price less than their basis cost for their shares. If you sell covered calls over and over, all that premium effectively reduces your total cost for the position, so maybe $90 is still more than your basis, if you’ve collected a total of over $10 in premium. Maybe it’s a good idea or maybe not, depends on what got you to this point.

Roll out in time. Even if the price has dropped a lot, a covered call seller should be able to roll out at the same strike price for a credit, even if it isn’t much. As you roll out, the Delta value will also go up. In fact the further you roll out, the higher the premium and the higher the Delta value, but within limits- the position is out of the money. The question is whether the premium collected is enough to give up potential gains if the stock comes roaring back. If you roll out, how far out? I generally don’t like to roll out very far if I’m not collecting very much, but for some traders this is an ideal situation, collecting a little premium with very little risk of having the stock called away. It’s all a manner of perspective.

Stop selling calls on the stock for a while. I sometimes do this when the market is way down and it seems oversold. During big corrections or bear markets, I will let my calls either expire, or I may buy them back to close them when they have little value. In this case, I’m willing to wait a bit for the stock to make a comeback. If I’m not willing to wait, maybe I should close the out the stock position as well and put the money into something else. Sometimes, it is just time to cut losses and get out. But assuming that I want to keep the stock and I think it is just temporarily underpriced, I may choose to just hold the stock and not sell calls until the stock price is at a better value.

Which is the right choice? That’s up to each trader to decide. It also may depend on your view of the stock and the current market, as well as the stock’s cost basis. There are several factors to weigh, so there is no single answer for all situations.

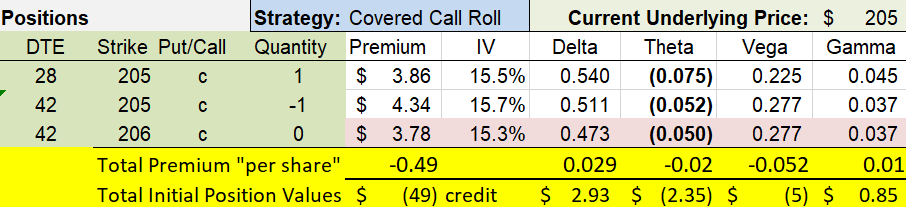

To keep going with our earlier example, let’s say our stock declined from 201 to 195, so we decide to roll down and out.

With the stock price down, we decide to roll down and out and collect more premium.

We collect more net credit for this roll than earlier ones, because our old call strike is farther out of the money and IV has increased a bit. Our new Delta is quite a bit higher than where our old Delta has dropped to. We also make more on the call’s decrease in value from 0.69 to 0.15, a profit of $54. But, since our stock went down $6 a share, the stock lost $600. Our net change for the covered call is a loss of $546, so we lost less than if we held stock alone. So far, every example we’ve seen shows the call making our results better than if we had stock alone.

On the opposite side of the value scale, what does a trader do when the Delta value of the call gets high, or even gets in the money? This situation used to really frustrate me, because the covered calls probably have lost money when looking at the call alone. But, if you look at the underlying stock and the call, the total position is making money, even if the call ends up in the money. So, this is a better situation than when stock prices are falling and the short call is gaining. In fact, let’s instead think of this as a good problem to have. This time, let’s consider four ways to deal with this situation.

Roll out and up for credit. If the stock has gone up, let’s try to move our strike price of our call up as well. The problem is that it can be hard to collect a net credit because higher strike options are not as expensive as a lower strike. So, to collect a credit, we may need to go further out in time to find an option at a higher strike price that also has more premium than the current option that is being replaced. As calls get into the money, the deeper in the money they are, the harder it becomes to roll up for a credit. And the further out a call is rolled in time, the harder the next roll is to roll up and out for a credit. That doesn’t mean that you shouldn’t do it, it just means that it is more difficult.